The drawdown found its sellers. Where Issue 8 documented a price decline with no clearly identifiable seller—a risk-off drift attributed to macro and geopolitics—this week the selling pressure acquired specific, nameable sources. Bitcoin fell from roughly $73,400 to a cycle low near $59,100 on June 6, propelled by three attributable catalysts landing on top of the same Strait-of-Hormuz oil backdrop: a record 13-session US spot Bitcoin ETF outflow streak that drained $4.37 billion before snapping on June 4 with a token $3.05 million inflow; Strategy's disclosure on June 1 of its first bitcoin sale in four years; and a hot May payrolls print (+172,000 versus an 80,000 consensus) that pushed Federal Reserve rate-cut expectations further out. On the on-chain native track, HYPE round-tripped—setting a fresh all-time high near $75.5 on June 1–2 before a scheduled token unlock and Arthur Hayes's full exit drove a roughly 12% pullback—even as Hyperliquid's derivatives franchise kept setting records. And the prediction-market third line restructured rather than simply grew: Robinhood began routing World Cup contracts to its own Rothera exchange instead of Kalshi, ahead of the June 11 tournament. CME, meanwhile, cleared roughly $50 million over its first-ever 24/7 weekend—but the second-weekend read, the figure that actually settles Issue 8's suspense, was still unpublished.

Week of June 1 to June 7, 2026

Bitbase Research · June 8, 2026

Market Insights is Bitbase Research's short-wave companion to our Deep Dive flagship series. Each edition reviews the most structurally meaningful developments of the preceding week in compliant crypto derivatives and on-chain native infrastructure, mapped against the long-wave framework set out in our flagship reports. The previous issue documented a structural milestone—CME's switch to 24/7 regulated crypto trading on May 29—landing in the same week as a nine-session ETF outflow streak driven by exogenous geopolitical shock, with HYPE decoupling to a fresh high and prediction markets formally adopted as a standing tracking line. This issue records the week that decline broadened and found attributable sellers: the ETF streak extended to a record thirteen sessions before breaking, Strategy executed the bitcoin sale its Q1 guidance had foreshadowed, and a strong jobs report removed the near-term rate-cut tailwind. This week spans a data-scope split: crypto-native data covers the full seven days (June 1–7), while traditional-finance data—US spot Bitcoin and Ether ETF flows, MSTR equity, the jobs report—trades or releases only on weekdays. US markets were open Monday through Friday June 1–5 and closed for the weekend June 6–7. All TradFi data is anchored to end-of-day Friday June 5 (ET) unless otherwise stated; crypto data extends through Sunday June 7. The Federal Reserve entered its communications blackout on June 6 ahead of the June 16–17 FOMC, Warsh's first meeting as Chair.

1. The one chart that matters

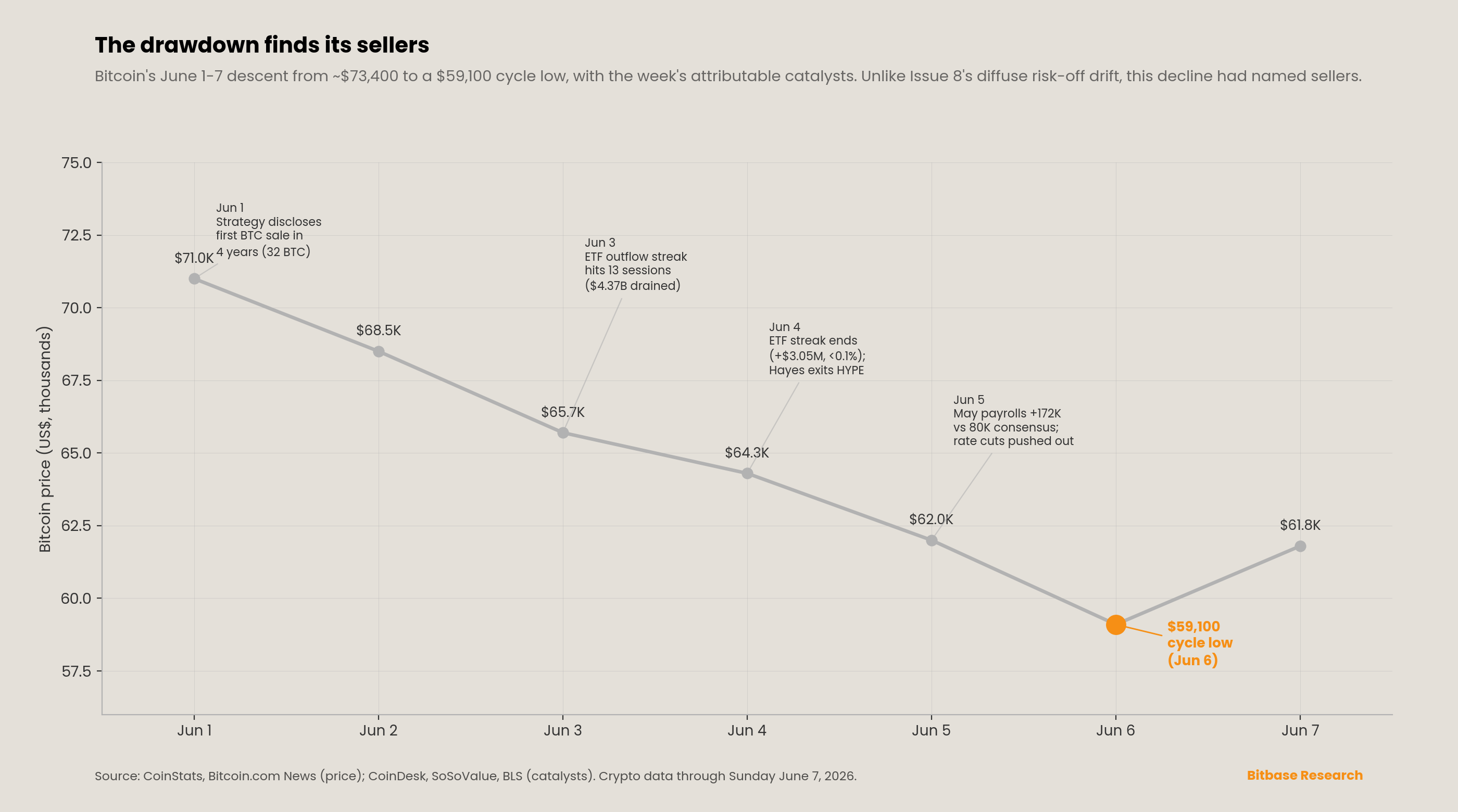

The chart traces Bitcoin's descent across the week and labels the catalysts that distinguish this drawdown from the prior one. Bitcoin entered June around $73,400—the level at which Issue 8 closed—and fell in steps: it was already near $71,000 when Strategy's sale disclosure hit on Monday June 1; broke below $66,000 mid-week; breached $62,000 on Friday June 5 as the jobs report landed; and touched a cycle low near $59,100 on June 6 before a modest bounce to roughly $61,800 by June 7 [1][2]. The Crypto Fear & Greed Index sat at 12 (Extreme Fear) for most of the week [2]. The structural point is not the magnitude of the move—roughly 19% peak-to-trough from the late-May high—but its character: where Issue 8's decline was a risk-off drift with no single identifiable seller, this week the selling had specific, sourced origins.

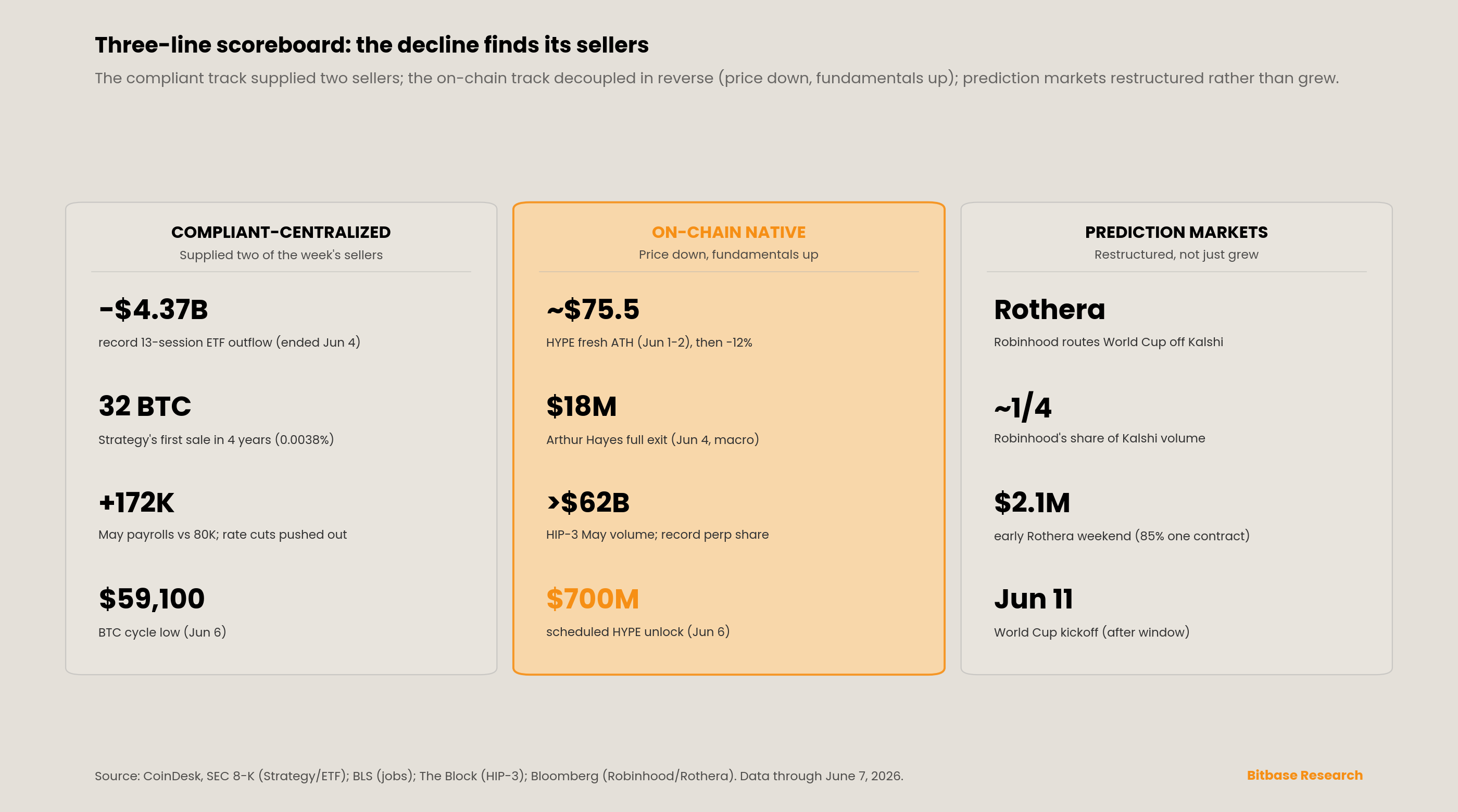

That is the through-line of this issue. Three catalysts, each independently documented, stacked on top of the same geopolitical oil backdrop that drove the prior week. First, the regulated-ETF channel: US spot Bitcoin ETFs extended what became a record thirteen-session outflow streak, draining $4.37 billion before it broke on June 4 [3][4]. Second, the corporate-treasury channel: Strategy disclosed on June 1 that it had sold bitcoin for the first time in four years, a symbolically large move despite its trivial size [5]. Third, the macro channel: a May payrolls print of +172,000—more than double the consensus—killed the case for a near-term Federal Reserve rate cut [6][7]. None of these alone would define a week; landing together, they converted a sentiment-driven retreat into a decline with attributable sellers. The remainder of this issue traces each catalyst and then turns to the on-chain native track, where price and fundamentals diverged sharply, and to the prediction-market line, which restructured ahead of the World Cup.

2. This week's structural signal

The structural signal of the week is that the spot Bitcoin ETF complex completed its longest outflow streak on record—thirteen consecutive sessions—then broke it with an inflow so small it underscored, rather than reversed, the trend. The streak's end is the bottoming signal Issue 8 flagged as the one to watch; its weakness is the reason that signal does not yet qualify as a bottom.

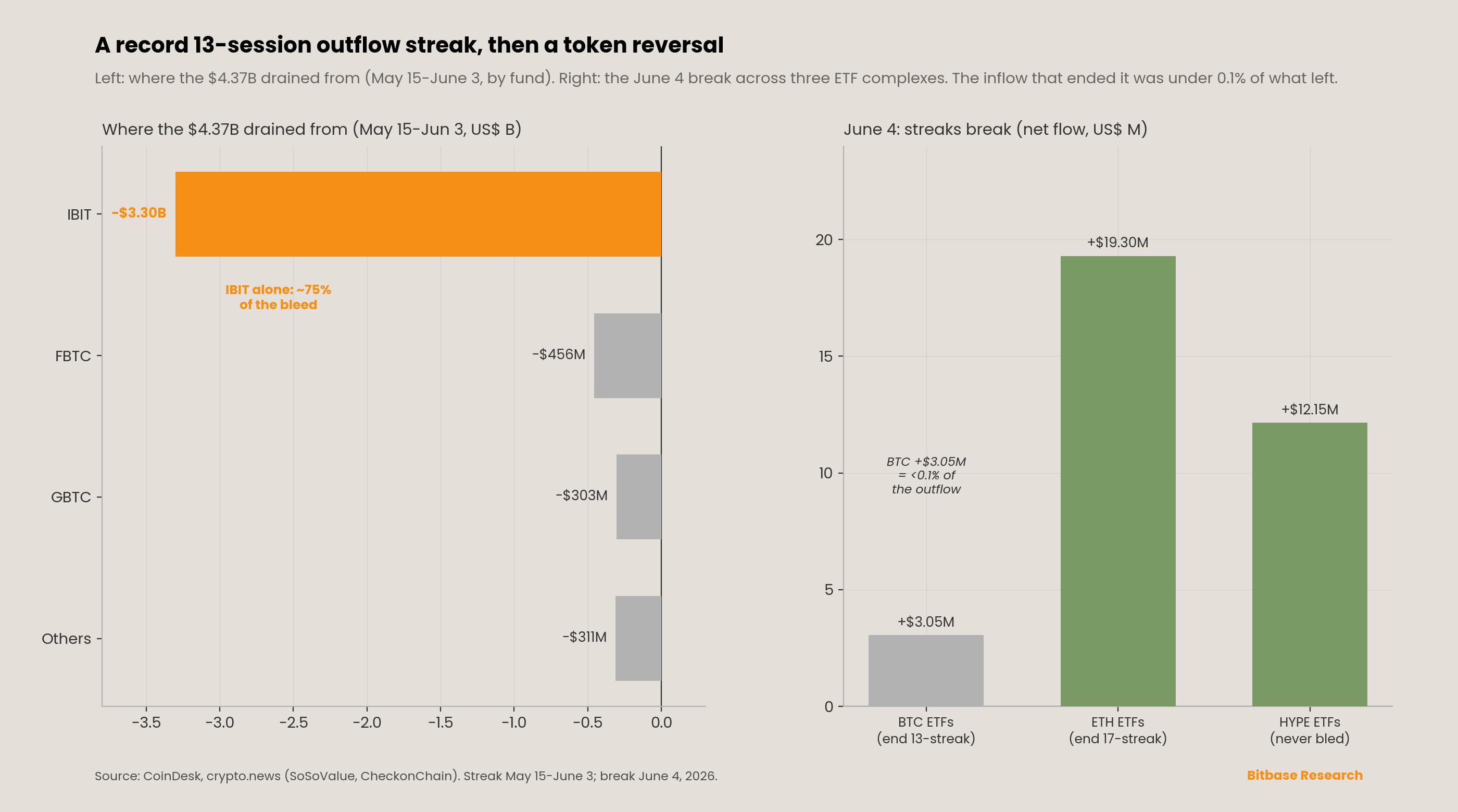

US spot Bitcoin ETFs recorded thirteen consecutive sessions of net outflows from May 15 through June 3, the longest such streak since the products launched in January 2024, draining approximately $4.37 billion from the complex [3][4]. The concentration is the tell: BlackRock's IBIT alone accounted for roughly $3.3 billion—about 75% of the total—identifying the bleed as large institutional redemptions through the dominant vehicle rather than a broad retail panic; Fidelity's FBTC contributed roughly $456 million and Grayscale's GBTC roughly $303 million [4]. The seven sessions from June 2 onward accounted for approximately $3.4 billion of the total, the largest single calendar-week outflow on record—a distinct rolling-window measure that should not be conflated with the 13-session figure [4]. Total assets across the US spot Bitcoin ETFs fell from $104.29 billion on May 15 to $82.83 billion on June 3, with holdings down to approximately 1.277 million BTC, about 7.2% below the October 2025 peak (CheckonChain) [4]. Of the thirteen sessions, only the tail—June 1 through June 3—and the break fall inside this reporting week; the streak itself began in the prior window, and we flag that boundary explicitly rather than present the full $4.37 billion as a single-week event.

The streak broke on Thursday June 4 with a net inflow of approximately $3.05 million—a figure less than 0.1% of what had left, and smaller than any single day of outflows during the run, most of which exceeded $100 million [3][4]. The inflow came almost entirely from BlackRock's IBIT, which took in $47.66 million, while Fidelity's FBTC, Bitwise's BITB, and Ark's ARKB continued to bleed on the same session [4]. (One aggregator, citing the Trader T dataset, put the net figure at +$2.69 million rather than +$3.05 million; we use the SoSoValue figure CoinDesk reports, and flag the minor caliber difference.) The same day, US spot Ether ETFs ended an even longer 17-session outflow streak with a +$19.30 million inflow driven entirely by BlackRock's ETHA—every other Ether ETF logged zero net flow [4]. And the Hyperliquid HYPE ETFs, launched in mid-May, were the only crypto ETF complex to avoid outflows throughout the sell-off, taking in +$12.15 million on June 4 to reach $185.68 million in assets [4]. The lesson Issue 8 anticipated holds: the end of a streak is not the same as a bottom. The more reliable confirmation would be two or more consecutive sessions of net inflows above roughly $100 million—a threshold this week's $3 million print falls far short of.

3. Dual-track scoreboard

Compliant-centralized track. The week's most-discussed corporate event was Strategy's first bitcoin sale in four years—a move whose symbolic weight vastly exceeded its size. In an 8-K filed Monday June 1, the company disclosed that it sold 32 BTC at an average net price of roughly $77,135 (about $2.5 million in proceeds) during May 26–31, with the proceeds earmarked to fund dividend payments on STRC, its perpetual preferred stock [5]. The disclosure date falls in this week; the sale itself occurred in the prior reporting window, and we flag that distinction rather than present it as a June 1–7 transaction. As of May 31, Strategy still held 843,706 BTC at an average cost of $75,699, meaning the sale represented about 0.0038% of its holdings—a rounding error on the balance sheet [5]. The last time the company sold was a small tax-loss harvest in December 2022; this was its first disclosed net disposal in four years [5].

The sale was not a surprise so much as a confirmation. On the Q1 2026 earnings call, Executive Chairman Michael Saylor had already signaled it, saying the company would "probably sell some bitcoin to pay a dividend just to inoculate the market and send the message that we did it" [5]. This is the on-the-ground execution of the pivot Issue 8 identified—from pure accumulation toward active balance-sheet management—rather than a reversal of conviction. Wall Street read it the same way, with caveats: two analysts called the roughly $2.5 million sale economically immaterial and tactical, with TD Cowen's Lance Vitanza saying reports that Strategy had become a meaningful seller were overblown, while at least one other suggested something larger might be afoot [5]. We present both readings rather than adjudicate. The market's immediate reaction was a "sell the headline" move: MSTR shares fell roughly 5% on June 1 [5]. (Separately, Form 4 filings around June 5 disclosed routine planned insider equity sales by CEO Phong Le and CFO Andrew Kang—personal-equity transactions, not company bitcoin sales, and not to be confused with the treasury disposal.)

On-chain native track. Detailed in Section 5; in brief, HYPE round-tripped from a fresh all-time high while Hyperliquid's underlying derivatives franchise kept setting records—a sharp divergence between token price and protocol fundamentals.

Prediction-market third line. The line restructured rather than simply grew. On June 4, Bloomberg reported that Robinhood had begun routing select 2026 World Cup event contracts—individual match outcomes, the tournament winner, and total goals—to Rothera, the CFTC-regulated exchange it co-owns with Susquehanna International Group (the rebranded former LedgerX, acquired November 2025), while keeping player-specific and combination markets on Kalshi [8]. The structural significance: a Bernstein analysis cited by Bloomberg estimated Robinhood generated close to a quarter of Kalshi's total trading volume in early 2026, so the routing shift could redistribute rather than grow the sector's reported volume [8]. Robinhood's own share of Kalshi flow had already fallen from roughly 60% in September 2025 to about 20% by April 2026 [8]. Early Rothera volumes remained modest—roughly $2.1 million over one recent weekend, about 85% of it tied to a single baseball contract—underscoring that this is a structural realignment, not yet a volume event [8]. Robinhood, which holds a 7% stake in Kalshi, reported more than 16 billion event contracts traded year-to-date in 2026, up from 12 billion in all of 2025 [8].

4. On the radar—week of June 8 to June 14

Several scheduled events in the week ahead are structurally larger than anything that settled this week, and we flag them as forward markers rather than reported facts.

-

FIFA World Cup kickoff (June 11). The tournament—104 matches across the US, Mexico, and Canada through July 19—is the first major stress test of the prediction-market infrastructure described above. DeFi Rate estimated Americans will trade more than $2.5 billion on World Cup prediction markets, including roughly $1.47 billion on Kalshi alone; these are projections, not realized volume, and the Robinhood-Rothera routing shift adds uncertainty to how that volume distributes [8]. Spain and France entered as co-favorites near 16–18% apiece across venues.

-

SpaceX IPO (expected pricing ~June 11, Nasdaq debut ~June 12). SpaceX set a fixed $135-per-share IPO price and launched its roadshow June 4, targeting a raise near $75 billion at a valuation around $1.75 trillion—which would be the largest IPO in history. As of June 7 the offering had not priced or begun trading; we note it as pending, not as an in-week event, and flag that on-chain pre-IPO venues such as Ventuals offer synthetic exposure but reported no specific in-window SpaceX-market volume.

-

CME second-weekend 24/7 data. The single most important unreported datapoint: whether CME's June 6–7 weekend volume materially exceeds the roughly $50 million inaugural figure. See Section 5.

-

Fed in blackout into the June 16–17 FOMC. With the communications blackout running June 6–18, no Fed speech will move markets in the week ahead; the hot jobs print has already made a June hold near-certain. The next macro triggers are the June CPI (released mid-July) and any de-escalation in the Hormuz oil situation.

5. Signal tracking update

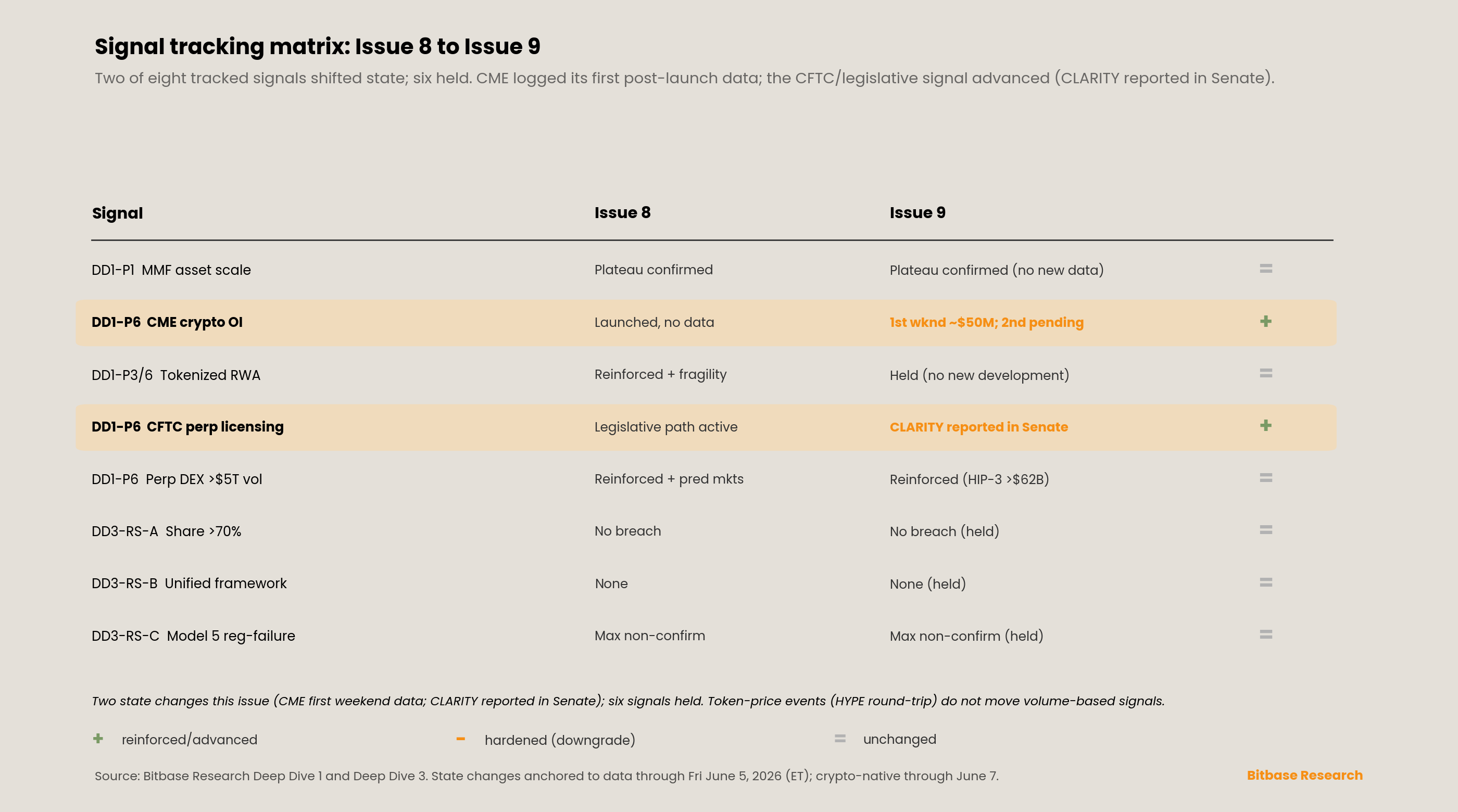

Five Deep Dive 1 signals plus three Deep Dive 3 reverse signals remain under continuous audit. This issue records two signals shifting state—the CME microstructure signal logging its first post-launch data, and the CFTC/legislative signal advancing as the CLARITY Act was reported in the Senate—while the remaining six hold their Issue 8 readings. The HYPE round-trip and the jobs report covered in Sections 2, 3, and 5's narrative bear on these signals but, as detailed below, do not by themselves move them.

SIGNAL—Deep Dive 1 Part 1: "MMF asset scale inflection point." STATUS: Plateau confirmed (held from Issue 8); no new reading. No fresh ICI weekly money-market-fund release fell within this reporting window, so the signal carries its Issue 8 reading—a confirmed plateau, with assets having decelerated from a +12.0% trailing-52-week pace to a near-flat year-to-date pace—unchanged. We flag the absence of new data rather than infer a move; the signal holds at "plateau confirmed" pending the next ICI print.

SIGNAL—Deep Dive 1 Part 6: "Whether CME crypto derivatives OI persistently holds above $30B by 2027." STATUS: On track; first post-launch data logged. This is the week the signal gained its first observable evidence since the 24/7 launch. Per CME's June 1 release, more than 7,200 cryptocurrency futures and options contracts traded over the inaugural 24/7 weekend (May 30–31), totaling approximately $50 million in notional, with Bitcoin Volatility futures (ticker BVI) joining the schedule on day one [9][10]. The figure is real but small: as The Defiant observed, $50 million is a sliver of weekday flow—CME's 2026 year-to-date crypto average daily volume is roughly 407,200 contracts—but it is the first weekend in the venue's history that it was open at all [10]. A single weekend cannot distinguish "launch curiosity" from "steady-state floor," and the second-weekend (June 6–7) figure—the read that would begin to settle that question—had not been published by any Tier-1 source as of June 8. The signal stays "on track," evaluated against full-year data; the second-weekend print is the next observable evidence and the top infrastructure watch into Issue 10.

SIGNAL—Deep Dive 1 Parts 3 and 6: "Tokenized RWA as common collateral infrastructure." STATUS: Reinforced with fragility qualifier (held from Issue 8); no new development. No material new tokenized-RWA or synthetic-equity development settled within this window. The SpaceX IPO roadshow launched June 4 with a fixed $135 price, which intensifies interest in the synthetic pre-IPO category (Ventuals, trade.xyz) ahead of the expected ~June 11 pricing, but the listing had not occurred and produced no in-window on-chain settlement data. The signal holds its Issue 8 reading, including the Ventuals-derived fragility qualifier on the synthetic pre-IPO sub-layer.

SIGNAL—Deep Dive 1 Part 6: "Whether the U.S. CFTC approves more licensed entities to offer perpetual swap-style products by 2027." STATUS: Legislative path advanced; administrative path still pending. The signal moved on the legislative side this week: the CLARITY Act (H.R.3633), which would classify Bitcoin as a commodity, was reported in the Senate on June 1, a procedural step toward a floor vote, though CoinDesk cautioned the bill faces a tight calendar and unresolved conflict-of-interest provisions [17]. The CFTC's own perpetual-style-product rulemaking remained unmoved, and the adjacent prediction-market rule received by White House OIRA on May 26 showed no further movement in-window. The legislative track advances; the perpetual-specific administrative track holds at pending.

SIGNAL—Deep Dive 1 Part 6: "Whether perpetual DEX annual trading volume holds above $5 trillion in 2026." STATUS: Structurally reinforced (held and extended from Issue 8). Hyperliquid's franchise kept setting records: HIP-3 builder-deployed perpetuals topped $62 billion in May volume, the protocol's share of global perpetual-futures volume reached a record, and trade.xyz held more than 90% of HIP-3 open interest [13]. The HYPE token's roughly 12% round-trip this week—from a fresh all-time high near $75.5 on June 1–2 down to the $59–62 range after a scheduled ~$700 million June 6 unlock and Arthur Hayes's full $18 million exit—is a token-price event, not a signal-state change: Hayes attributed his exit explicitly to macro factors and stated it did not reflect a changed view of fundamentals, and 10xResearch's Markus Thielen, even while calling the rally short-term overheated at ~25x projected fee revenue, described Hyperliquid as "one of the most impressive businesses in crypto" at ~77% gross margins [11][12]. The signal—which tracks volume, not price—reads structurally reinforced. The Ventuals "yellow light" from Issue 8 now has a companion risk dimension worth noting in passing: scheduled token unlocks as a recurring, mechanical source of HYPE-specific sell pressure, distinct from protocol performance.

SIGNAL (Deep Dive 3 Reverse Signal A)—Market-share concentration above 70%. STATUS: No concentration breach (held). Hyperliquid's record share of global perpetual-futures volume this week is notable, but no single venue breached the 70% model-concentration threshold, and no new independent third-party attribution was published in-window. The five-model coexistence thesis from Deep Dive 3 holds.

SIGNAL (Deep Dive 3 Reverse Signal B)—Cross-architecture unified regulatory framework. STATUS: No unified framework (held). The CLARITY Act's advance in the Senate is a single-jurisdiction (US) legislative step, not a cross-jurisdiction harmonization event; no new ESMA, FCA, MAS, JFSA, BIS, or Basel coordination statement was issued in-window. The five-model regulatory divergence documented in Deep Dive 3 remains the state of record.

SIGNAL (Deep Dive 3 Reverse Signal C)—Model 5 regulatory failure. STATUS: Maximally non-confirming (sustained from Issue 8). The reverse signal positing regulatory failure for the on-chain-native model wrapped by US-regulated access remains maximally non-confirming. During a week when the broad spot Bitcoin ETF complex bled for a record thirteen sessions, the Hyperliquid HYPE ETFs were the only crypto ETF complex to avoid outflows entirely, taking +$12.15 million on June 4 to reach $185.68 million in assets [4]; and the CFTC/legislative track advanced rather than stalled. The regulated-wrapper channel for on-chain-native assets is strengthening, not failing.

6. New dimension—the attributability of the decline

If Issue 8's methodological contribution was distinguishing structure from flow, Issue 9's is distinguishing a decline with attributable sellers from one without. The distinction is not academic. Issue 8's drawdown was a risk-off drift: prices fell, but the proximate seller was diffuse—macro de-risking against a geopolitical tail, with capital rotating within the asset class (XRP ETFs took inflows even as Bitcoin ETFs bled). That kind of decline tends to resolve when the external shock clears, because nothing structural had broken.

This week is different. The selling had three named, independently sourced origins: a record institutional ETF redemption streak concentrated in a single vehicle (IBIT, ~75% of the bleed); a corporate-treasury seller breaking a four-year pattern, however trivially; and a macro data point that repriced the rate path. When a decline has identifiable sellers, the bottoming logic changes: the question is no longer "when does the shock clear" but "are the sellers exhausted." That reframing is why the recommendation below ties the upgrade threshold to flow persistence (two-plus days of >$100 million ETF inflows) and a price reclaim, rather than to any single headline. The $3 million June 4 inflow ended a streak; it did not signal seller exhaustion.

A second-order observation: the on-chain native track decoupled in the opposite direction this week from last. In Issue 8, HYPE rose while the regulated channel bled. In Issue 9, HYPE fell on idiosyncratic supply (an unlock and a high-profile exit) while its protocol fundamentals strengthened—the inverse pattern. The consistent reading across both weeks is that the on-chain native track moves on its own logic, and conflating HYPE's token price with Hyperliquid's franchise health—in either direction—misreads the signal.

Caveats

-

Date integrity. The 13-session ETF outflow streak began May 15, outside this window; only June 1–3 (the tail) and June 4 (the break) fall inside it, and the full $4.37 billion is not a single-week figure. Strategy's bitcoin sale occurred May 26–31 and was disclosed June 1; the disclosure is in-window, the transaction is not. The CME 24/7 launch was May 29; only the first-weekend result (reported June

-

is confirmed, and the second-weekend figure is unpublished. Arthur Hayes's HYPE exit (June 4) and the scheduled token unlock (June 6) are two distinct events on different dates, not a single one. The FIFA World Cup (June 11) and the SpaceX IPO (expected ~June 11–12) both fall after this window and had not occurred as of June 7.

-

Data caliber conflicts flagged. BTC ETF streak total: $4.37 billion (SoSoValue, 13 sessions) is distinct from the "$3.4 billion single-week record" (the seven sessions from June 2). June 4 net inflow: $3.05 million (SoSoValue/CoinDesk) versus $2.69 million (Trader T dataset). HYPE ATH: $75.51 (June 1) versus $75.48 (June 2). Jobs consensus: 80,000 (CNBC/Dow Jones) versus 85,000 (some desks).

-

Source attribution. Total-holdings figure (1.277 million BTC, –7.2% from the October peak) is CheckonChain's, not Galaxy's; IBIT concentration (~75%) and fund-level splits are per SoSoValue via CoinDesk and crypto.news.

-

Unconfirmed/pending items. No new MSTR weekly 8-K covering June 1–7 was confirmed as of June 8, though Michael Saylor's June 7 social post revived purchase speculation. CME second-weekend volume was unreported. The CFTC event-contract rule, received by White House OIRA on May 26, showed no further movement in-window. No specific stablecoin supply-change datapoint surfaced for the week.

-

Causation discipline. All causal attributions—Strategy's sale weighing on sentiment, the jobs report removing the rate-cut tailwind, the unlock and Hayes's exit driving HYPE lower—reflect the cited outlets' framing and the principals' own stated reasoning, not independent Bitbase inference.

-

This is not investment advice. Bitbase Research does not make price predictions or recommend positions. Figures are anchored to end-of-day Friday June 5 (ET) for TradFi and Sunday June 7 for crypto-native data unless otherwise stated.

References

[1] Bitcoin.com News, "Bitcoin Holds Above $59.1K Low as Short-Term Charts Signal Oversold Bounce Setup," June 7, 2026. Cycle low ~$59,100 June 6; bounce to ~$61,800 June 7; RSI-14 oversold. https://news.bitcoin.com/bitcoin-holds-above-59-1k-low-as-short-term-charts-signal-oversold-bounce-setup/

[2] CoinStats, "Bitcoin Daily Market Analysis," June 4–7, 2026. Price timeline June 1–7; Fear & Greed Index 12 (Extreme Fear). https://coinstats.app/ai/a/latest-news-for-bitcoin

[3] crypto.news, "Spot Bitcoin ETFs attract $3M as historic outflow streak comes to an end," June 5, 2026. June 4 +$3.05M ends 13-session streak; IBIT +$47.66M; AUM $80.40B; 1.277M BTC (CheckonChain). https://crypto.news/spot-bitcoin-etfs-attract-3m-as-historic-outflow-streak-comes-to-an-end/

[4] CoinDesk, "Bitcoin and ether spot ETFs end record multibillion outflow streak," June 5, 2026. 13-session streak ~$4.4B; ETH 17-session streak ends +$19.30M; HYPE ETFs $185.68M; IBIT $47.66M. https://www.coindesk.com/markets/2026/06/05/bitcoin-and-ether-etfs-end-record-multi-billion-outflow-streak

[5] CoinDesk, "Strategy sold 32 BTC for $2.5 million in late May, filing shows," June 1, 2026, and SEC EDGAR Form 8-K (filed June 1, 2026). 32 BTC @ $77,135; 843,706 BTC held @ $75,699; STRC dividend; Saylor Q1-call quote; analyst reactions. https://www.coindesk.com/markets/2026/06/01/strategy-sold-32-btc-for-usd2-5-million-in-late-may-filing-shows

[6] CNBC, "Jobs report May 2026," June 5, 2026. +172,000 payrolls; consensus 80,000; unemployment 4.3%; earnings +0.3% m/m, +3.4% y/y. https://www.cnbc.com/2026/06/05/jobs-report-may-2026.html

[7] US Bureau of Labor Statistics, "The Employment Situation—May 2026" (USDL-26-0786), June 5, 2026. +172,000; March/April revised +93,000 combined; sector detail; long-term unemployed 27.5%. https://www.bls.gov/news.release/empsit.nr0.htm

[8] Crypto Briefing / Bloomberg, "Robinhood shifts World Cup bets to Rothera," June 4, 2026; Next Event Horizon, "Robinhood Is Using Rothera For World Cup Markets." Routing shift; Rothera (ex-LedgerX); Bernstein ~quarter-of-Kalshi-volume; Kalshi ~$68B YTD; Robinhood 7% Kalshi stake; 16B event contracts YTD. https://cryptobriefing.com/robinhood-world-cup-rothera-exchange/

[9] CME Group, "CME Group Announces Launch of 24/7 Cryptocurrency Futures and Options Trading," June 1, 2026. Inaugural weekend 7,200+ contracts, ~$50M notional; BVI futures 24/7; McCourt quote. https://www.cmegroup.com/media-room/press-releases/2026/6/01/cme\_group\_announceslaunchof247cryptocurrencyfuturesandoptionstra.html

[10] The Defiant, "CME Group Processes 7,200 Crypto Contracts in First Weekend of 24/7 Trading," June 2, 2026. $50M = sliver of weekday flow; YTD crypto ADV 407,200 contracts; second-weekend the next data point. https://thedefiant.io/converge/tradfi-and-fintech/cme-group-7200-crypto-contracts-first-weekend-247-trading

[11] CoinDesk, "Hyperliquid pulls back from record highs as Arthur Hayes exits position," June 4, 2026. ATH ~$75.5; Hayes sells 247,334 HYPE (~$18M) June 4; macro rationale; Thielen 77% margins, 25x fee revenue. https://www.coindesk.com/markets/2026/06/04/hyperliquid-pulls-back-from-record-highs-as-arthur-hayes-exits-position-shy-of-usd150-price-target

[12] CoinMarketCap CMC-AI, "Latest Hyperliquid News," June 2026. $700M scheduled monthly unlock June 6; ATH $75.51 June 1; HYPE ~$59.35 post-unlock (–12%). https://coinmarketcap.com/cmc-ai/hyperliquid/latest-updates/

[13] The Block, "Hyperliquid hits record share of global perps market as HIP-3 tops $62 billion," June 3, 2026. HIP-3 >$62B May volume; record global perp share; trade.xyz >90% HIP-3 OI. https://www.theblock.co/post/403384/hyperliquid-record-share-global-perps-market-hip-3-tops-62-billion-monthly-volume

[14] Bloomberg (paywalled; the +172K figure's primary citations are [6] CNBC and [7] BLS official, both freely accessible), "US Adds 172,000 Jobs in May, Beating All Economists' Estimates," June 5, 2026. Payrolls beat; rate-path repricing. https://www.bloomberg.com/news/articles/2026-06-05/us-adds-172-000-jobs-in-may-beating-all-economists-estimates

[15] CNBC, "SpaceX targets fixed $135 IPO price for roadshow," June 3, 2026. $135/share; roadshow June 4; pricing ~June 11; Nasdaq debut ~June 12 (SPCX); ~$75B raise, ~$1.75T valuation. https://www.cnbc.com/2026/06/03/spacex-ipo-stock-price-roadshow-musk.html

[16] DeFi Rate, "Robinhood Launches World Cup Prediction Markets Through Rothera," June 5, 2026. >$2.5B projected US WC volume; ~$1.47B Kalshi projection; World Cup June 11–July 19. https://defirate.com/news/robinhood-launches-world-cup-prediction-markets-through-rothera/

[17] CoinDesk, "Clarity Act survival depends on the U.S. Senate," June 2, 2026. H.R.3633 reported in Senate June 1; tight calendar. https://www.coindesk.com/news-analysis/2026/06/02/clarity-act-survival-depends-on-the-u-s-senate

[18] Bitbase Research, "Market Insights — Issue 8," June 1, 2026. Prior-week framework; CME 24/7 launch; nine-session ETF streak; HYPE ATH; prediction-market line adoption.

[19] Bitbase Research, "Deep Dive 1" (five signals) and "Deep Dive 3" (three reverse signals). Signal framework referenced in Section 5.

[20] CheckonChain, spot Bitcoin ETF holdings data. 1.277M BTC; –7.2% from October 2025 peak. https://checkonchain.com