Structure moves while price falls—and the two are not telling the same story. The defining event of the week was structural rather than directional: on Friday May 29, 2026 at 4:00 PM Central Time, CME Group switched its regulated cryptocurrency futures and options to continuous around-the-clock trading on Globex, retiring the decades-old weekend "CME gap" that has shadowed Bitcoin futures since their December 2017 launch. Simultaneously, crypto prices drifted lower in a risk-off tape—Bitcoin fell approximately 4% on the week to roughly $73,400—driven by a nine-session US spot Bitcoin ETF outflow streak that included BlackRock IBIT's –$527.84 million single-day redemption on May 27, the second-largest on record. The trigger was macro and geopolitical—renewed US airstrikes near the Strait of Hormuz—rather than any crypto-specific failure. Against that entire backdrop, Hyperliquid's HYPE token printed a fresh all-time high in the $68.30–$69.97 range, the only major name in the complex to set a new high while Bitcoin, Ether, and XRP all fell. And in the structural background, the prediction-market sector—Kalshi and Polymarket combined monthly volume now near $24 billion, with the FIFA World Cup two weeks out—crossed the threshold to become a permanent Bitbase tracking line.

Week of May 25 to May 31, 2026

Bitbase Research · June 1, 2026

Market Insights is Bitbase Research's short-wave companion to our Deep Dive flagship series. Each edition reviews the most structurally meaningful developments of the preceding week in compliant crypto derivatives and on-chain native infrastructure, mapped against the long-wave framework set out in our flagship reports. The previous issue documented macro tightening reinforced from three sides—the four-dissent FOMC minutes, Waller's hawkish Frankfurt pivot, and Warsh's May 22 White House swearing-in—alongside the assembly of a complete institutional-flow stack around Hyperliquid. This issue records the first full week of the Warsh chairmanship (notably low-profile, consistent with Warsh's stated preference for a less communicative Fed rather than any blackout constraint—the week fell outside any FOMC communications blackout), a structural milestone in regulated-derivatives microstructure, a nine-session ETF outflow streak driven by exogenous geopolitical shock, and the formal adoption of a prediction-market tracking line. This week spans a data-scope split: crypto-native data covers the full seven days (May 25–31), while traditional-finance data—US spot Bitcoin ETF flows, money-market funds, MSTR equity—trades only on weekdays. US markets were closed Monday May 25 (Memorial Day), open Tuesday through Friday May 26–29, and closed for the weekend May 30–31. All TradFi data is anchored to end-of-day Friday May 29 (ET) unless otherwise stated; crypto data extends through Sunday May 31.

1. The one chart that matters

The chart captures the central paradox of the week: a permanent change to market structure landing in the same five days as a sharp risk-off drawdown, with the two operating on entirely different clocks. On Friday May 29 at 4:00 PM Central Time, CME Group switched its regulated cryptocurrency futures and options—covering Bitcoin, Ether, Solana, XRP, Cardano, Chainlink, Stellar, Avalanche, and Sui in both standard and micro sizes—to continuous trading on CME Globex, with a single weekly maintenance window [1][2]. For the first time since CME Bitcoin futures launched in December 2017, the Friday-close-to-Sunday-reopen blackout that produced the widely watched "CME gap" is structurally gone [2]. This is a genuine microstructure milestone: it removes the roughly two-day weekend window during which institutional traders could not adjust regulated positions while crypto spot markets kept moving, reducing weekend risk premia and improving hedging efficiency for asset managers, hedge funds, and corporate treasury desks.

Yet the near-term price impact was approximately nil—and that absence is itself the insight. The launch coincided with a risk-off tape, and liquidity did not migrate to CME. As of the report date, no Tier-1 source had published actual first-weekend (May 30–31) volume or open-interest figures—a timing artifact, since CME settles weekend trades on the next business day (Monday June 1)—so any figures circulating are pre-launch year-to-date baselines, not post-launch outcomes [1][2]. The pre-launch baselines for context only: 2026 year-to-date crypto average daily volume of approximately 407,200 contracts (up 46% year-over-year), average daily open interest of approximately 335,400 contracts, and 2025 full-year notional volume of approximately $3 trillion [1][3]. More tellingly, liquidity remains concentrated elsewhere: per Volmex Labs CEO Cole Kennelly, BlackRock's IBIT ETF options hold roughly $27–30 billion in open interest, dwarfing CME Bitcoin futures options at roughly $800–900 million [2]. The structural change is real; the flow change has not yet happened. That distinction—structure moving without flow following—is the through-line of this entire issue.

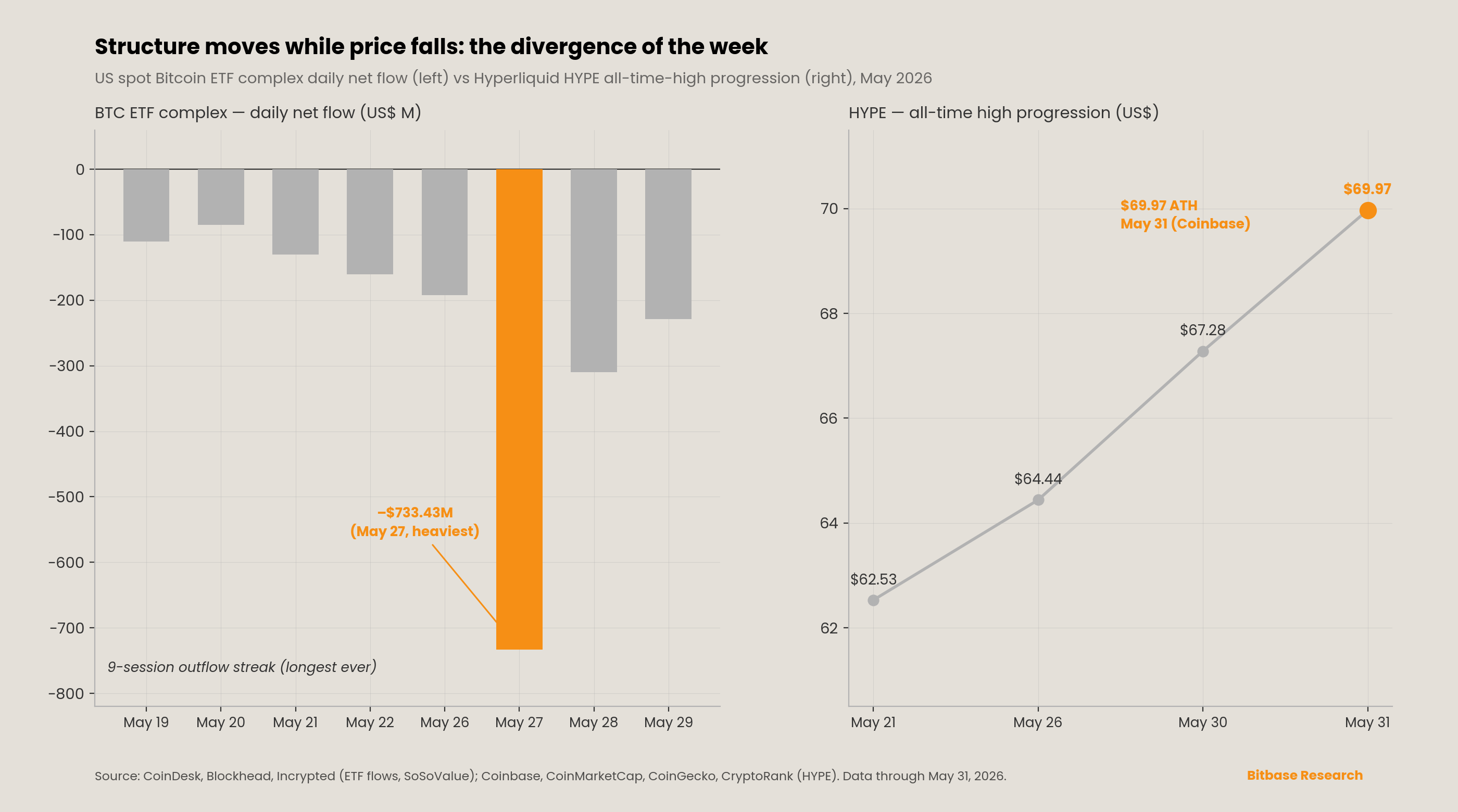

On the other side of the chart, the divergence between the regulated-ETF channel and the on-chain native token could not be starker. US spot Bitcoin ETFs extended a nine-session outflow streak through Thursday May 29, the longest since the products launched—breaking the prior record of eight consecutive sessions set in February 2025 [4]. Yet HYPE, Hyperliquid's native token, climbed to a fresh all-time high in the $68.30–$69.97 range across exchange feeds (Coinbase $69.97 on May 31; CoinMarketCap $69.45; CoinGecko $68.45; CryptoRank $68.30 on May 30), a weekly gain of approximately 8% from roughly $63.55 [5]. It was the only major digital asset by market capitalization to set a new high during a week in which Bitcoin, Ether, and XRP all declined. The contrast between the bleeding regulated-wrapper channel and the rallying on-chain native token is the structural signal: macro de-risking compressing the ETF channel and spot Bitcoin simultaneously, while the on-chain derivatives-infrastructure franchise decoupled entirely.

2. This week's structural signal

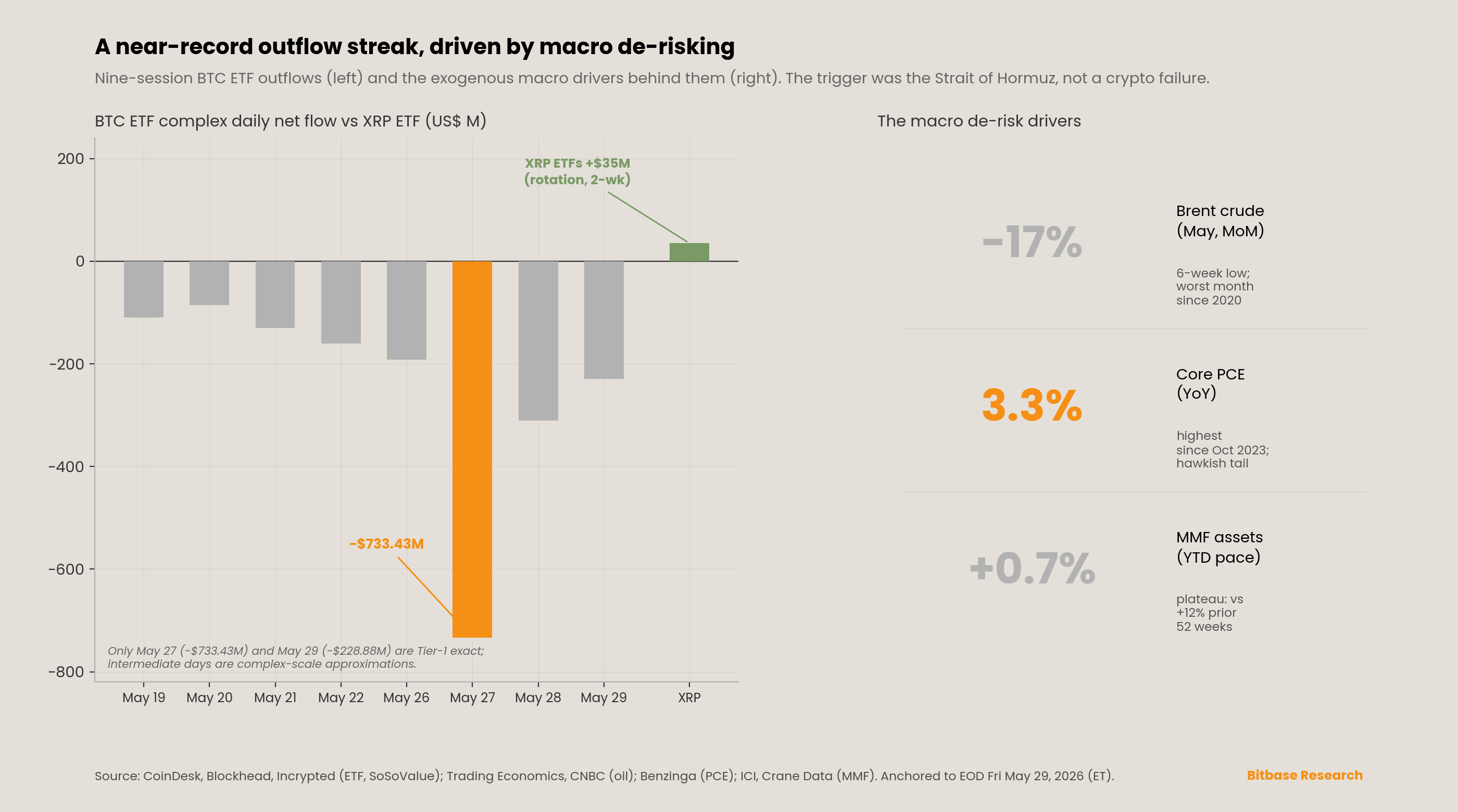

The structural signal of the week is that a near-record ETF outflow streak was driven by exogenous macro de-risking, not by any failure of the crypto-asset wrapper itself. The distinction matters for the long-wave read: a streak caused by a geopolitical shock resolves when the shock clears, whereas a streak caused by structural disillusionment with the ETF channel would not.

US spot Bitcoin ETFs posted their ninth consecutive session of net outflows on Thursday May 29, the longest such streak since the products launched in January 2024, surpassing the prior record of eight straight sessions set in February 2025 [4]. The heaviest single day was Wednesday May 27: BlackRock's IBIT shed –$527.84 million, its second-largest single-day net outflow on record, missing the all-time record of –$528.30 million (set January 30) by roughly $500,000 [6]. The same day, Fidelity's FBTC lost –$60.30 million and Grayscale's GBTC bled –$104.76 million, bringing the spot-ETF complex to –$733.43 million for the session (across the eleven U.S.-listed funds per CoinDesk's count; some trackers cite thirteen vehicles)—the heaviest single-day complex redemption since late January [6]. Thursday May 29 extended the streak with a further –$228.88 million, of which IBIT accounted for –$177.94 million [4]. (US markets were closed Monday May 25 for Memorial Day; the streak's trading days were Tuesday–Thursday May 26–29, with the weekend May 30–31 also closed.)

The cumulative figures require careful caliber. Over the two-week span, IBIT alone shed approximately $2.04 billion, while the broader eleven-fund complex shed approximately $2.6 billion—the two are distinct measures and should not be conflated [4][6]. GBTC's cumulative outflows since its conversion to a spot ETF have now surpassed $26 billion [6]. One clarifying detail from Tuesday May 26: a single investor sold $1.29 billion of IBIT shares in one dark-pool block trade, which is not the same as a net outflow—dark-pool trades are privately negotiated and do not directly translate to redemptions, and IBIT's actual net outflow that day was –$192.44 million [6]. The block trade is notable as signal, but the arithmetic distinction is the kind of thing that gets a flow figure wrong if read carelessly.

The trigger was unambiguously macro. Bitcoin broke below $73,000 on Thursday (trading at $72,978 in Asian hours, down 3.4% over 24 hours) after US airstrikes on an Iranian military site near the Strait of Hormuz reignited a conflict that markets had begun to price out [6]. ETF redemptions and the spot decline fed each other: redemptions forced issuers to sell the underlying asset to settle exits, accelerating the move. The crucial countervailing data point is intra-crypto rotation rather than wholesale exit: across the same window, XRP ETFs took in approximately $35 million in net inflows [4]. Capital was not abandoning the asset class; it was rotating within it and de-risking against a geopolitical tail. As CoinDesk noted, IBIT has weathered comparable streaks before during this cycle without a permanent reversal, with money returning each time the macro picture cleared [6]. The more reliable bottoming signal, accordingly, is not the end of the streak but the first net-inflow day.

The macro backdrop reinforced the risk-off read. April PCE, released Thursday May 28, showed headline inflation accelerating to +3.8% year-over-year (from 3.5%), the highest reading since May 2023, with core PCE at +3.3% (from 3.2%), the highest since October 2023; on a monthly basis headline rose +0.4% and core +0.2%, both slightly cooler than consensus, while first-quarter GDP was revised down to a 1.6% annualized pace [7]. The print kept the Federal Reserve firmly on hold for the June meeting—CME FedWatch placed the probability of no change on June 17 at roughly 99.9%—while futures continued to price a rising probability of a hike by year-end on sticky inflation, a hawkish tail rather than the cuts the White House has demanded. Money-market fund assets, the macro-liquidity counterweight, rose +$13.39 billion to $7.78 trillion for the week ended May 27 per ICI, but the longer trend is a plateau: assets are up just $51 billion year-to-date (+0.7%) versus +$836 billion (+12.0%) over the trailing 52 weeks, having peaked at $7.856 trillion roughly ten weeks earlier [8]. The upstream swing factor was oil: Brent crude collapsed to roughly $91–92.5 per barrel by May 29, a six-week low, down approximately 17–19% on the month—its worst month since 2020—on optimism over a tentatively agreed US–Iran 60-day ceasefire memorandum that would reopen the Strait of Hormuz [9][10]. That optimism remained explicitly unconfirmed: President Trump had not yet approved the proposed terms, Iranian state media said the agreement was not finalized, and Vice President Vance cautioned that it was uncertain whether or when a deal could be reached [9]. The oil round-trip—spiking intra-week on the Hormuz strike, then fading on ceasefire hopes—drove both the May 27–28 ETF outflow spike and the late-week relief in yields and the dollar.

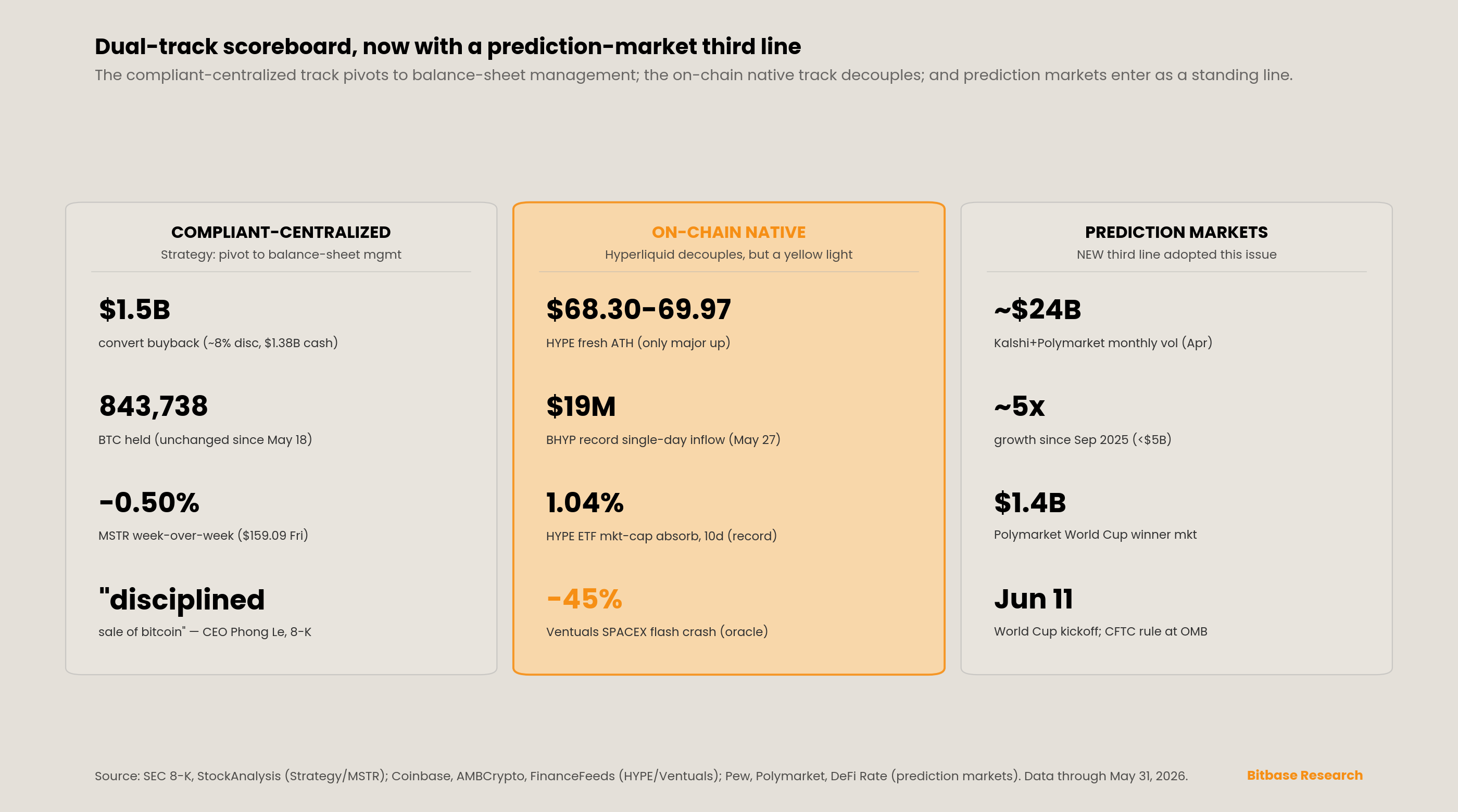

3. Dual-track scoreboard

Compliant-centralized track. The week's signal from Strategy was a pivot in kind, not degree: the company shifted from pure accumulation toward active balance-sheet management. An 8-K filed Tuesday May 26 disclosed that over the period May 11–25, Strategy repurchased $1.5 billion aggregate principal of its 0% Convertible Senior Notes due 2029 for approximately $1.38 billion in cash—an approximate 8% discount to par—lowering convertible notes outstanding from $8.2 billion to $6.7 billion [11]. Through the repurchase, the company generated a BTC Yield of 0.7%, a BTC Gain of 4,391 BTC, and a BTC Dollar Gain of $333 million [11]. As of May 25, Strategy holds 843,738 bitcoin (unchanged since the May 18 purchase—its longest accumulation gap in the recent run), with 220,900 sats per share, $15.5 billion notional of preferred stock outstanding, and a USD Reserve of $871 million it plans to replenish over time [11]. The same filing confirmed the funding of the prior week's purchase: an additional $2.0 billion notional of STRC preferred and $84 million of MSTR common stock were issued and used to buy 24,869 bitcoin; year-to-date the company reports a BTC Yield of 13.3%, BTC Gain of 89,378 bitcoin, and BTC Dollar Gain of $6.8 billion [11].

The strategic reframing is the signal. In the filing, President and CEO Phong Le stated that the company would "use the full range of capital management tools available to us, including the disciplined sale of bitcoin" [11]—language that, appearing in an official SEC filing rather than secondhand commentary, formally introduces two-directional balance-sheet management into a treasury that markets had modeled as a one-way accumulator. The weekly "Saylor bought X BTC" catalyst that had anchored the compliant-centralized track for much of the cycle is, for now, paused. MSTR equity reflected the recalibration without panic: the stock closed Tuesday May 26 around $159.93 and Friday May 29 at $159.09 (+4.91% on the day, +$7.45), as the buyback was read as balance-sheet-strengthening; against the prior Friday's $159.89 close (Issue 7), that is approximately –0.50% week-over-week—essentially flat, but flat in the precise sense, not the loose one [12]. Market capitalization sat near $56.5 billion [12]. (MSTR did not trade May 25 or the May 30–31 weekend.) The forward variables are the June 8 STRC holder vote on semi-monthly dividends, any 8-K resuming purchases after the May 18 gap, and—most consequential for the long-wave read—how the $871 million USD Reserve is replenished: via equity and credit, or, per Le's language, via the disciplined sale of bitcoin.

On-chain native track. Hyperliquid was the week's standout divergence—the only major name to rally while the rest of the complex fell. HYPE climbed to a fresh all-time high in the $68.30–$69.97 range across exchange feeds (Coinbase $69.97 on May 31), a weekly gain of approximately 8% from roughly $63.55, with market capitalization around $15–17.5 billion [5]. The drivers are increasingly those of a derivatives-infrastructure franchise rather than a speculative altcoin. Spot HYPE ETFs absorbed approximately 1.04% of the token's market capitalization in their first ten days per Kairos Research—the strongest crypto-ETF debut on record, ahead of Bitcoin (0.59%), Ether (0.41%), and Solana (0.31%). Bitwise's BHYP took a record single-day inflow of approximately $19 million on May 27—on roughly $22 million of volume, almost entirely buys—to become the world's largest HYPE ETF, per Bitwise CEO Hunter Horsley [13]. That the record ETF inflow landed on the same day Bitcoin ETFs posted their heaviest single-day redemption is the rotation thesis in microcosm. ICE CEO Jeff Sprecher publicly called Hyperliquid "bigger than Nasdaq," and a Grayscale report projected roughly $800 million in annualized protocol revenue, with a reported $115 million HYPE seed deal under negotiation [5].

But the same track flashed a yellow light. On Thursday May 28, the Ventuals SPACEX-USDH perpetual—a synthetic pre-IPO contract referencing SpaceX's implied share price, deployed on Hyperliquid's HIP-3 framework—crashed approximately 45% in 30 minutes, falling from $2,277 to $1,254 before rebounding near $2,169, and liquidating roughly $1.51 million in notional value across 405 traders and 1,393 positions [14][15]. The cause was not organic selling: an off-chain data provider (Notice) used in the oracle price calculation mishandled SpaceX's 5-for-1 stock split, feeding a corrupted price into Hyperliquid's mark-price-and-liquidation engine [14]. Thin liquidity amplified the cascade—the market had generated only $4.87 million of volume in the prior 24 hours against roughly $2.8 million of open interest [15]. Ventuals pledged to compensate affected users within 48 hours [15]. The episode was market-specific rather than systemic—HYPE set new highs the following day—but it is a clean illustration of the tail risk in the HIP-3 synthetic pre-IPO layer: single-oracle dependency, no public order book, and dangerously thin depth during corporate-action edge cases. (For the record, an attempt by some commentators to link the crash to the later Blue Origin rocket explosion does not survive scrutiny: the timelines do not align, and the connection has been debunked [14].) Context: SpaceX filed its S-1 with the SEC on May 20, disclosing an 18,712-bitcoin position worth roughly $1.45 billion and targeting a valuation above $1.75 trillion, with pricing expected around June 11 and a Nasdaq listing as early as June 12 under the ticker SPCX [14]. The synthetic SPACEX market exists precisely because speculative interest peaks in the final weeks before that listing—which is also why the oracle fragility matters now rather than later.

4. On the radar—week of June 1 to June 8

-

CME 24/7 first hard data (Monday June 1 settlement onward). The first Monday-settled weekend volume and open-interest prints are the first empirical read on whether continuous regulated trading drew real weekend activity. Threshold to change the structural-not-flow view: sustained weekend average daily volume above roughly 5–10% of weekday ADV would signal genuine liquidity migration; persistent near-zero weekend activity confirms that the launch is a structural milestone without near-term flow consequences. Watch also whether the weekly maintenance window becomes the new thin-liquidity volatility locus.

-

First Bitcoin ETF net-inflow day as the bottoming signal. Per Glassnode's framework, the rate of change in the 14-day flow moving average—not the streak length—is the turn signal. A single net-inflow day above roughly $200 million, or a clean Hormuz ceasefire signing, would flip the tactical bias. A tenth and eleventh consecutive outflow day would instead push year-to-date complex flows toward net-negative for 2026 for the first time since launch.

-

Strategy June 8 STRC holder vote and post-May-18 purchase cadence. The semi-monthly-dividend vote is a dated catalyst. More consequential: any 8-K resuming bitcoin purchases would frame the May 18 gap as a pause; continued silence would confirm the pivot to balance-sheet management. The escalation trigger is any disclosure of bitcoin sales—rather than equity or credit issuance—to replenish the $871 million USD Reserve, which would activate Le's "disciplined sale" language as realized policy.

-

SpaceX IPO pricing (~June 11) and Nasdaq debut (~June 12, ticker SPCX). The largest US IPO in recent memory carries direct crypto relevance: SpaceX's S-1 discloses an 18,712-bitcoin position. Watch how the Ventuals and trade.xyz synthetic SPCX perpetuals converge to (or dislocate from) the actual listing price—the cleanest live test yet of on-chain pre-IPO price discovery against a real public-market benchmark.

-

Hormuz ceasefire finalization—the dominant macro swing factor. The tentatively agreed 60-day US–Iran memorandum is not yet approved by Trump and not confirmed by Iran. Finalization would likely extend the Brent decline (and with it the risk-on relief in crypto); a collapse of the talks would re-spike the war premium and re-pressure ETF flows. This single variable sits upstream of oil, yields, the dollar, and crypto risk-off flows.

-

Warsh's first FOMC (June 16–17) and the December-hike tail. The June meeting is a near-certain hold (~99.9% priced), but the distribution for later 2026 has tilted toward a hike (futures implying meaningful odds of at least one increase by year-end). New Chair Kevin Warsh has indicated he believes the benchmark rate could be lowered, though he is likely to face opposition from the rest of the FOMC—a tension between the White House's stated rate-cut demand and an inflation print at a three-year high. Warsh made no in-week policy statement. The week fell outside any FOMC communications blackout (the blackout for the June 16–17 meeting runs June 6–18); other Fed officials did speak publicly. Warsh's quiet is more consistent with his stated intent to reduce Fed public communication than with any institutional constraint.

-

CFTC prediction-market rule in White House OMB review. On May 26, the proposed CFTC prediction-market rule was received by the White House Office of Information and Regulatory Affairs for review (reported May 28)—a step toward the first comprehensive federal event-contract framework, which President Trump has endorsed under the CFTC's exclusive authority [16]. Publication for public comment after OMB review is the next trigger. State-level friction (challenges in several states, Minnesota's felony ban) persists in parallel.

-

GENIUS Act rulemaking deadline (July 18) and CLARITY Act floor scheduling. Stablecoin implementing rules are due by July 18, 2026; central prohibitions take effect on the earlier of January 18, 2027 or 120 days after final rules. The CLARITY Act, which would classify Bitcoin as a commodity, awaits a full Senate floor vote with Trump urging passage. Absence of scheduling through June compresses the timeline materially.

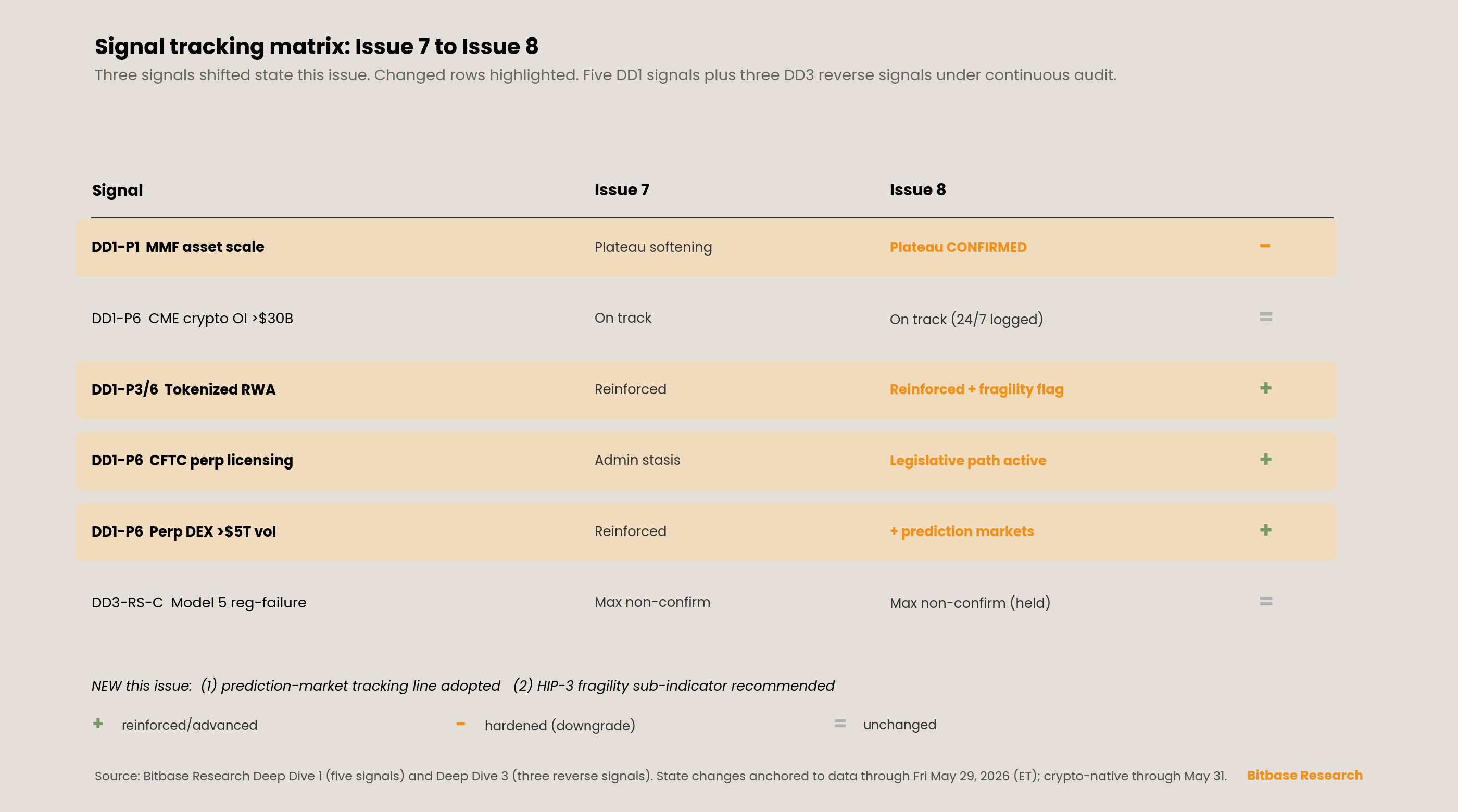

5. Signal tracking update

Five Deep Dive 1 signals plus three Deep Dive 3 reverse signals remain under continuous audit. This issue records three signals shifting state: the MMF plateau call hardening from "softening" to "confirmed plateau," the tokenized-RWA/HIP-3 read gaining a new fragility qualifier after the Ventuals episode, and the perpetual-DEX signal extending into a prediction-market connection. This issue also formally recommends a new HIP-3 fragility sub-indicator and adopts a prediction-market tracking line (detailed in Section 6).

SIGNAL—Deep Dive 1 Part 1: "MMF asset scale inflection point." STATUS: Plateau confirmed (hardened from "plateau softening" in Issue 7). ICI's May 28 release reported total MMF assets at $7.78 trillion for the week ended May 27, up +$13.39 billion week-over-week (government +$12.37 billion, prime +$2.83 billion, tax-exempt –$1.82 billion; retail +$4.03 billion to $3.09 trillion, institutional +$9.36 billion to $4.69 trillion) [8]. The single-week growth looks healthy in isolation, but the trend data confirms the plateau the Issue 7 "softening" call anticipated: per Crane Data, MMF assets are up only $51 billion year-to-date (+0.7%) against +$836 billion (+12.0%) over the trailing 52 weeks, having peaked at $7.856 trillion roughly ten weeks ago [8]. The deceleration from a 12% annual pace to a 0.7% year-to-date pace is the structural read: the post-2022 money-market accumulation wave has flattened, and the marginal dollar is no longer flowing into cash at the prior rate. The signal holds at "plateau confirmed" until either a sustained reacceleration above the prior trend or a decisive drawdown below $7.70 trillion.

SIGNAL—Deep Dive 1 Part 6: "Whether CME crypto derivatives OI persistently holds above $30B by 2027." STATUS: On track; structural milestone logged, no post-launch data yet. CME's switch to 24/7 trading on May 29 is the most significant microstructure change to regulated crypto derivatives since the products launched, but it is operationally distinct from the CFTC perpetual-futures framework tracked under the separate signal below, and—critically—no post-launch volume or open-interest data was available by the report date [1][2]. The pre-launch year-to-date baselines (407,200-contract ADV, 335,400-contract average OI) are not launch outcomes and must not be read as such [1]. The 24/7 expansion plausibly bears on aggregate CME OI in coming quarters by removing the weekend hedging gap, but the signal continues to be evaluated against full-year 2026 and 2027 data when published. The first observable evidence arrives with the June 1+ Monday-settled weekend prints.

SIGNAL—Deep Dive 1 Parts 3 and 6: "Tokenized RWA as common collateral infrastructure." STATUS: Reinforced, with a new fragility qualifier. The reinforcement and the warning arrived together. On the reinforcement side, the HIP-3 synthetic-equity layer continued to expand: SpaceX's May 20 S-1 filing intensified speculative interest in the synthetic SPCX perpetuals on both Ventuals and trade.xyz, and the broader tokenized pre-IPO category is maturing into a recognized on-chain price-discovery venue ahead of major listings. On the warning side, the Ventuals SPACEX 45% flash crash on May 28 exposed the tail risk of the architecture: an off-chain oracle mishandling a corporate action (the 5-for-1 stock split) cascaded into $1.51 million of liquidations across 405 traders, amplified by thin liquidity [14][15]. The structural significance is unchanged—tokenized and synthetic real-world assets are increasingly settled and margined alongside crypto pairs on the same venue—but the episode establishes that the synthetic pre-IPO sub-layer carries oracle and liquidity fragility that the tokenized-Treasury sub-layer does not. This issue recommends formalizing that distinction (see HIP-3 fragility sub-indicator below).

SIGNAL—Deep Dive 1 Part 6: "Whether the U.S. CFTC approves more licensed entities to offer perpetual swap-style products by 2027." STATUS: Legislative path active; administrative path still pending. The CFTC's own rulemaking on perpetual-style products remains unresolved, but the adjacent prediction-market rulemaking advanced materially this week: the proposed CFTC prediction-market rule was received by White House OMB (OIRA) for review on May 26 (reported May 28), the procedural step before publication for public comment [16]. President Trump has publicly backed the CFTC's exclusive federal authority over event contracts. While this rule concerns event contracts rather than perpetual swaps directly, it signals an active, advancing CFTC rulemaking posture after the administrative stasis documented across prior issues. The CLARITY Act, which would classify Bitcoin as a commodity, awaits a full Senate floor vote. The administrative-stasis read from Issue 7 is partially relieved on the prediction-market track; the perpetual-specific track remains unmoved.

SIGNAL—Deep Dive 1 Part 6: "Perpetual DEX 2026 above $5T volume." STATUS: Structurally reinforced, now extending into prediction markets. Hyperliquid's core franchise continued to compound—the protocol processes roughly $6 billion in daily derivatives volume and has demonstrated 24/7 real-world-asset trading throughout the first half of 2026. The new development is categorical: Hyperliquid's HIP-4 outcome-market primitive (binary/multi-outcome event contracts, distinct from the HIP-3 builder-perpetual framework) went live on mainnet on May 2, 2026, and per Hyperion DeFi CEO Hyunsu Jung, its first Bitcoin outcome market did roughly three times the volume of equivalent markets on Polymarket and Kalshi combined [17]. While the launch itself predates this reporting week, it is logged here as the structural link now being activated: full permissionless market creation (via a HYPE stake) is the next phase, and Bernstein has extended its digital-assets coverage to include prediction markets as a tracked trend [17]. This extends the perpetual-DEX signal into a new product category and directly connects the on-chain native track to the prediction-market third line adopted this issue.

SIGNAL—Deep Dive 3 Reverse Signal C: "Model 5 regulatory-failure scenario." STATUS: Maximally non-confirming (sustained from Issue 7). The reverse signal positing regulatory failure for the on-chain native model with US-regulated wrappers remains maximally non-confirming. BHYP became the world's largest HYPE ETF on a record inflow day; spot HYPE ETFs posted the strongest first-ten-day market-cap absorption of any crypto ETF on record; and the CFTC's prediction-market rulemaking advanced into OMB review rather than stalling. The regulated-wrapper channel for on-chain native assets is strengthening, not failing. The two Deep Dive 3 reverse signals not detailed here (Reverse Signal A, market-share above 70%; Reverse Signal B, cross-architecture unified framework) recorded no state change this week and remain at their Issue 7 readings.

6. New tracking line—prediction markets

This issue formally adopts a prediction-market / event-contract flow tracking line as a permanent fixture of the Market Insights framework. The decision rests on structural growth, not the World Cup alone—though the tournament is a near-term catalyst layered on top of an already-durable trend.

The sector growth is structural. Per a Pew Research Center analysis of data from The Block, combined monthly global trading volume on Kalshi and Polymarket rose from less than $5 billion in September 2025 to approximately $24 billion in April 2026—a roughly fivefold increase in eight months, now exceeding the total monthly handle of US legal sportsbooks (around $14 billion per month in 2025) [18]. The platform composition is distinct: in April 2026, Polymarket International recorded approximately $9 billion in volume against Polymarket US's $1.3 billion, and the topic mix diverges sharply—sports is 80% of Kalshi's volume versus 39% of Polymarket's, while politics is 4% of Kalshi versus 32% of Polymarket [18]. We deliberately avoid a "who dominates" claim: market-share figures vary dramatically by methodology (notional versus on-chain, inclusion of Polymarket US, measurement window), with credible estimates of Kalshi's share ranging from the high-20s to the low-60s percent. The durable, source-consistent fact is the absolute volume trajectory, and that is what we track.

The World Cup is the near-term catalyst. The 2026 FIFA World Cup (hosted by the USA, Mexico, and Canada) opens June 11—this issue falls roughly two weeks before kickoff. Polymarket's "World Cup Winner" single market has generated approximately $1.4 billion in total trading volume since it launched on July 2, 2025, with France and Spain effectively tied at around 17% implied probability each as of May 31 [19]. (A separately aggregated Kalshi-plus-Polymarket winner contract shows a smaller $452 million volume on a volume-weighted basis—a different measurement scope that should not be conflated with Polymarket's single-market $1.4 billion.) The final is July 19 at MetLife Stadium, with the market resolving July 20 [19].

The regulatory and crypto-native dimensions complete the case. On the regulatory side, the CFTC prediction-market rule entered White House OMB review on May 26 (reported May 28), advancing toward the first comprehensive federal event-contract framework [16]. On the crypto-native side, Polymarket settles on Polygon (direct on-chain volume), and Hyperliquid's HIP-4 outcome markets (live on mainnet since early May)—with a first Bitcoin market reportedly tripling the Polymarket-plus-Kalshi equivalent—bring the primitive directly into the HYPE ecosystem [17]. Taken together—roughly fivefold sector growth to $24 billion per month, institutional capital entering the space, a federal framework now in White House review, and a $1.4-billion-staked World Cup catalyst—the threshold for a standing tracking line is cleared. Recommended metrics: combined Kalshi-plus-Polymarket monthly volume; Polymarket on-chain (Polygon) volume; the sports-versus-non-sports mix; and CFTC rulemaking status. We expect a June–July World Cup volume spike layered on the durable ~$24-billion-per-month baseline.

We also recommend a HIP-3 fragility sub-indicator under the tokenized-RWA signal: per-market open interest, 24-hour volume, and oracle composition for the synthetic pre-IPO perpetuals (Ventuals, trade.xyz). The Ventuals 45% crash demonstrated that tail risk in this sub-layer is real, oracle-driven, and amplified by thin liquidity—distinct from the tokenized-Treasury layer, and worth tracking discretely as the SpaceX listing approaches.

Caveats

-

No CME post-launch data by report date. First-weekend (May 30–31) volume and open-interest figures were not yet published, as CME settles weekend trades on the next business day. Pre-launch year-to-date baselines (407,200-contract ADV, 335,400-contract OI) are not launch outcomes and are presented for context only.

-

Warsh made no in-week policy statement. This week fell outside any FOMC communications blackout (the blackout for the June 16–17 meeting runs June 6–18, per the St. Louis Fed), and other Fed officials did speak publicly. Warsh's relative silence is better read as his stated preference for a less communicative Fed than as an institutional constraint.

-

Stablecoin market-cap discrepancy flagged, not reconciled. Readings range from approximately $240 billion (a narrower dollar-stablecoin basket) to $315–320 billion or more (a broader measure); the two use different baskets. Issue 7's ~$322 billion baseline is consistent with the broader measure.

-

US market closures. Memorial Day (May 25) and the weekend (May 30–31) mean all ETF, MMF, and MSTR figures reflect only the May 26–29 trading window; crypto-native data extends through May 31.

-

Prediction-market share figures conflict by methodology. We use only Pew's absolute-volume figures and make no claim about which platform "dominates."

-

HYPE all-time high is a range. The $68.30–$69.97 span reflects different exchange aggregations; treat it as a range rather than a single print.

-

The Ventuals–Blue Origin link is debunked. A circulated attempt to connect the SPACEX perpetual crash to the later Blue Origin explosion does not survive timeline scrutiny and is not reflected here.

-

Analyst projections are not realized data. Forward targets (HYPE $100–150, MSTR analyst targets, year-end BTC ranges) and the SpaceX ~$1.75 trillion valuation target are projections and opinions, explicitly not realized figures.

-

Secondary data carries aggregator uncertainty. Precise weekly BTC OHLC and the two-week cumulative ETF totals (IBIT ~$2.04 billion / complex ~$2.6 billion) come from aggregators (SoSoValue, Farside); Tier-1 corroboration (CoinDesk, Blockhead, ICI, BEA, CME, SEC) was prioritized for headline figures.

References

[1] CME Group, "CME Group to Launch 24/7 Cryptocurrency Futures and Options Trading on May 29," official press release, February 19, 2026. Launch Friday May 29 at 4:00 PM Central Time on CME Globex; nine assets (BTC, ETH, SOL, XRP, ADA, LINK, XLM, AVAX, SUI), standard and micro; weekly maintenance window; 2025 notional volume ~$3T; 2026 YTD crypto ADV ~407,200 contracts (+46% YoY), average OI ~335,400 contracts. (Original source; robots-restricted to automated fetch—corroborated via CoinDesk [2].) https://www.cmegroup.com/media-room/press-releases/2026/2/19/cme\_group\_to\_launch247cryptocurrencyfuturesandoptionstradingonma.html

[2] CoinDesk, "Bitcoin's famous CME gaps are about to disappear, though three remain unresolved," May 28, 2026. 24/7 Globex launch from Friday; weekend "CME gap" effectively eliminated; weekend trades clear next business day; IBIT options OI ~$27–30B versus CME crypto options ~$800–900M (Volmex Labs CEO Cole Kennelly); three open gaps (~$80,000, ~$78,500, ~$70,000). https://www.coindesk.com/markets/2026/05/28/bitcoin-s-famous-cme-gaps-are-about-to-disappear-though-three-remain-unresolved

[3] Phemex, "CME 24/7 Crypto Futures Start May 29 | What Changes for BTC Traders," 2026. Pre-launch baseline detail: 407,200-contract YTD crypto ADV, 335,400-contract average daily OI, 403,900-contract futures ADV. https://phemex.com/blogs/cme-crypto-24-7-bitcoin-futures

[4] Blockhead, "Bitcoin ETFs Post Ninth Straight Day of Outflows as IBIT Notches Near-Record Redemption," May 29, 2026. Ninth consecutive session through May 29; breaks prior eight-session record (February 2025); May 29 complex –$228.88M, IBIT –$177.94M; IBIT two-week cumulative ~$2.04B; XRP ETF net inflows ~$35M. https://www.blockhead.co/2026/05/29/bitcoin-etfs-post-ninth-straight-day-of-outflows-as-ibit-notches-near-record-redemption/

[5] Coinbase, "Hyperliquid (HYPE) Price," accessed May 31, 2026. ATH $69.97 reached May 31, 2026; one-week price +8% from ~$63.55; market cap ~$17.46B. Cross-referenced: CoinMarketCap (ATH $69.45, May 31), CoinGecko (ATH $68.45, 65-exchange aggregate), CryptoRank (ATH $68.30, May 30). Grayscale ~$800M annualized revenue projection and ~$115M HYPE seed deal; ICE CEO "bigger than Nasdaq." https://www.coinbase.com/price/hyperliquid

[6] CoinDesk, "BlackRock's bitcoin ETF sheds $528 million, the second-largest daily outflow on record," May 28, 2026. IBIT –$527.84M on May 27 (second-largest on record, missing the January 30 record of –$528.30M by ~$500K); complex –$733.43M (FBTC –$60.30M, GBTC –$104.76M); GBTC cumulative post-conversion outflows >$26B; May 26 dark-pool block $1.29B ≠ net outflow (IBIT actual net –$192.44M); BTC $72,978 (–3.4% 24h); YTD accumulation thinned to ~4,500 BTC; IBIT ~$59B AUM. https://www.coindesk.com/markets/2026/05/28/blackrock-s-bitcoin-etf-sheds-usd528-million-the-second-largest-daily-outflow-on-record

[7] Benzinga, "Fed's Favorite Inflation Gauge Hits 3.8%, Highest Since May 2023," May 28, 2026. April PCE headline +3.8% YoY (from 3.5%, highest since May 2023), +0.4% MoM; core PCE +3.3% YoY (from 3.2%, highest since October 2023), +0.2% MoM; Q1 GDP revised to 1.6% annualized (from 2.0% initial). (Primary PCE source; CNBC bot-restricted to automated fetch.) https://www.benzinga.com/markets/macro-economic-events/26/05/52835775/us-pce-inflation-report-april-2026

[8] Investment Company Institute, "Money Market Fund Assets," May 28, 2026 release covering week ended May 27. Total MMF assets $7.78T, +$13.39B WoW (government +$12.37B, prime +$2.83B, tax-exempt –$1.82B); retail +$4.03B to $3.09T; institutional +$9.36B to $4.69T. Trend context via Crane Data: YTD +$51B (+0.7%) versus trailing-52-week +$836B (+12.0%); record $7.856T ~10 weeks prior. https://www.ici.org/research/stats/mmf

[9] Trading Economics, "Brent crude oil," accessed May 29, 2026. Brent ~$91.2/bbl Friday (six-week low), on track for ~17% May decline (most since 2020); tentative US–Iran 60-day ceasefire MOU to reopen Strait of Hormuz, Iran to clear mines within 30 days; Trump had not yet approved the terms, Iranian state media said not finalized, VP Vance cautioned uncertain. https://tradingeconomics.com/commodity/brent-crude-oil

[10] CNBC, "Oil drops 20% from 2026 peak on optimism over U.S.-Iran ceasefire talks," May 29, 2026. Brent $92.56 (–1.2% on the final trading day of May), down ~19% in May (worst month since the pandemic), ~20% off 2026 peaks; US and Iran "mostly agreed" to a 60-day memorandum of understanding. https://www.cnbc.com/2026/05/29/oil-prices-iran-ceasefire-us-trump-strait-hormuz-energy-costs.html

[11] U.S. Securities and Exchange Commission, "Strategy Inc Form 8-K (Exhibit 99.1)," May 26, 2026. Repurchase of $1.5B aggregate principal 0% Convertible Senior Notes due 2029 for ~$1.38B cash (~8% discount to par); convertible notes lowered $8.2B→(6.7B;\text{BTCYield}0.7) Gain $333M; holdings 843,738 BTC (as of May 25), 220,900 sats/share, preferred $15.5B notional, USD Reserve $871M; prior-week 24,869 BTC purchase funded by $2.0B STRC + (84\text{MMSTR};\text{YTDBTCYield}13.3) Gain $6.8B. CEO Phong Le: "the disciplined sale of bitcoin." https://www.sec.gov/Archives/edgar/data/0001050446/000119312526237907/mstr-ex99\_1.htm

[12] StockAnalysis / Google Finance, "Strategy Inc (MSTR) stock price history," accessed May 31, 2026. MSTR close May 29 $159.09 (+4.91%, +$7.45); open $149.92, high $162.06, low $148.20, market cap ~$56.5B; May 26 close ~$159.93. Versus Issue 7's verified May 22 close of $159.89 = approximately –0.50% WoW. https://stockanalysis.com/stocks/mstr/history/

[13] AMBCrypto, "Bitwise's $19M HYPE buy strengthens bull case, but ONE risk remains," May 27, 2026. BHYP $19M single-day net inflow on May 27 (93.15% of the day's $20.45M total HYPE-ETF buys; ~$22M volume, nearly all buys), becoming the world's largest HYPE ETF per Bitwise CEO Hunter Horsley; HYPE AUM $30.5M that day; spot HYPE ETFs = 1.04% of Hyperliquid's $15.63B market cap. https://ambcrypto.com/bitwises-19m-hype-buy-strengthens-bull-case-but-one-risk-remains/

[14] Unchained, "SpaceX Pre-IPO Contract on Hyperliquid Ventuals Crashes 45% on Faulty Oracle Data, Liquidating Hundreds," May 29, 2026. SPACEX-USDH perpetual –45% ($2,277→$1,254, rebound ~$2,169); cause: Notice off-chain oracle mishandled SpaceX's 5-for-1 stock split; 405 users / 1,393 trades liquidated; SpaceX S-1 filed May 20 (18,712 BTC ~$1.45B; target >$1.75T; pricing ~June 11, Nasdaq ~June 12, ticker SPCX); trade.xyz first SpaceX perp May 18 ($150 reference). Blue Origin link debunked (timeline misalignment, per Protos). https://unchainedcrypto.com/spacex-pre-ipo-contract-on-hyperliquid-ventuals-crashes-45-on-faulty-oracle-data-liquidating-hundreds/

[15] CoinDesk, "Hyperliquid's pre-IPO SpaceX contracts suffer 45% flash crash, liquidating $1.5 million," May 28, 2026. ~$1.51M notional liquidated in under 30 minutes; thin liquidity (24h volume ~$4.87M, OI ~$2.8M); Ventuals pledged 48-hour compensation. https://www.coindesk.com/markets/2026/05/28/hyperliquid-s-pre-ipo-spacex-contracts-suffers-45-flash-crash-liquidating-usd1-5-million

[16] CoinDesk, "White House reviews CFTC prediction-market rule as Trump backs federal control," May 28, 2026. Proposed CFTC prediction-market rule entered White House OMB (OIRA) review May 28; Trump endorsed CFTC exclusive federal authority over event contracts. https://www.coindesk.com/policy/2026/05/28/white-house-reviews-cftc-prediction-market-rule-as-trump-backs-federal-control

[17] DL News, "Hyperliquid takes aim at Kalshi, Polymarket targeting $24bn prediction markets," 2026. Hyperliquid's HIP-4 outcome-market primitive went live on mainnet May 2, 2026 (distinct from the HIP-3 builder-perpetual framework); first Bitcoin outcome market ~3x Polymarket-plus-Kalshi combined volume (Hyperion DeFi CEO Hyunsu Jung); protocol ~$6B daily derivatives volume; Bernstein added prediction markets to its digital-assets coverage. https://www.dlnews.com/articles/markets/hyperliquid-launches-prediction-markets-for-bitcoin/

[18] Pew Research Center, "Trading volume on prediction markets has soared in recent months," May 27, 2026 (analysis of data from The Block). Combined Kalshi+Polymarket monthly volume <$5B (September 2025) → ~$24B (April 2026); US legal sportsbooks ~$14B/month average in 2025; Polymarket International ~$9B versus Polymarket US $1.3B (April 2026); sports 80% of Kalshi versus 39% of Polymarket; politics 4% of Kalshi versus 32% of Polymarket. https://www.pewresearch.org/short-reads/2026/05/27/trading-volume-on-prediction-markets-has-soared-in-recent-months/

[19] Polymarket, "World Cup Winner," accessed May 31, 2026 (updated 8:15 PM UTC). Single market ~$1.4B total trading volume since launch July 2, 2025; France and Spain ~17% each; final July 19 (MetLife Stadium), resolves July 20. Separately, DeFi Rate aggregated Kalshi+Polymarket winner-contract VWAP volume ~$452.2M (distinct measurement scope). https://polymarket.com/event/world-cup-winner

[20] TronWeekly, "Bitcoin ETF Sees Longest Outflow Streak," May 30, 2026. IBIT ~$2.04B cumulative outflows over the period; IBIT holds ~792,000 BTC, ~62% of all spot Bitcoin ETF assets (Wallet Pilot); Farside net outflow –$223M on ninth day. https://www.tronweekly.com/bitcoin-etf-sees-longest-outflow-streak/

[21] Incrypted, "Bitcoin ETFs Shed $733M in a Single Day — Biggest Outflow Since January 2026," May 28, 2026. Complex –$733.43M on May 27 (largest since January 29 ~$818M); nine-session streak; ~$2.6B withdrawn over the period; ETH ETFs –$67.15M on May 27. https://incrypted.com/en/bitcoin-etfs-shed-733m-single-day-biggest-outflow-january-2026/

[22] Crane Data, "ICI Shows MMF Assets Up to $7.78T; Trends Confirms Big Drop in T-Bills," May 2026. ICI weekly +$13.39B to $7.785T (week ended May 27); YTD +$51B (+0.7%), trailing-52-week +$836B (+12.0%); record $7.856T ten weeks prior. https://cranedata.com/archives/all-articles/11359/

[23] CNBC, "Core inflation hit an annual rate of 3.3% in April, as expected, Fed's preferred gauge shows," May 28, 2026. Headline PCE +0.4% MoM / +3.8% YoY; core +0.2% MoM / +3.3% YoY; Q1 GDP revised to 1.6%; new Chair Warsh has indicated the benchmark rate could be lowered but is likely to face FOMC opposition. (Cited for the Warsh-vs-FOMC framing; PCE numerics corroborated by Benzinga [7].) https://www.cnbc.com/2026/05/28/core-inflation-hit-an-annual-rate-of-3point3percent-in-april-as-expected-feds-preferred-gauge-shows-.html

[24] Bybit / TradingView, "Hyperliquid (HYPE) price," accessed May 30, 2026. Cross-reference for HYPE ATH range and weekly performance; Bybit 24h high $67.13 (May 30), market cap ~$14.38B; TradingView one-week +21%. https://www.bybit.com/en/price/hyperliquid/

[25] Federal Reserve, "FOMC meeting calendars," accessed June 1, 2026; St. Louis Fed, "Federal Reserve Blackout Periods." Warsh's first FOMC as Chair June 16–17, 2026; the communications blackout for that meeting runs Saturday June 6–Thursday June 18 (the May 25–31 week falls outside any blackout). https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm

[26] Protos, "Hyperliquid SpaceX perp plummeted before Blue Origin explosion," May 30, 2026. Confirms the Ventuals SPACEX crash preceded—and is not causally linked to—the Blue Origin New Glenn explosion; timeline misalignment debunks the circulated connection; Ventuals identified Notice as the off-chain data provider. https://protos.com/hyperliquid-spacex-perp-plummeted-before-blue-origin-explosion/

[27] Unchained, "HYPE Spot ETFs Absorb 1.04% of Market Cap in First 10 Days, the Best Crypto ETF Debut on Record," May 27, 2026 (citing Kairos Research). Spot HYPE ETFs absorbed 1.04% of market cap in first ten days, versus BTC 0.59%, ETH 0.41%, SOL 0.31%; BHYP ~$19M single-day inflow (Hunter Horsley); combined two-fund cumulative inflows >$75M with 8-day inflow streak while BTC+ETH ETFs shed $112M that Tuesday. https://unchainedcrypto.com/hype-spot-etfs-absorb-1-04-of-market-cap-in-first-10-days-the-best-crypto-etf-debut-on-record/

[28] CME Group, "FAQ: Cryptocurrency Futures," accessed June 1, 2026. Weekend/holiday trades carry the next business day's trade date for clearing and settlement; weekly maintenance window detail. (Source descriptions of the maintenance-window timing vary across outlets; specific timing not locked here.) https://www.cmegroup.com/articles/faqs/frequently-asked-questions-cryptocurrency-futures.html

[29] Bitget (citing Cointelegraph), "Bitcoin ETFs bleed $2.8B in record nine-day outflow streak," May 2026. IBIT $527.8M May 27 second-largest on record; IBIT ~$2.04B cumulative May 15–29; HYPE ETFs ~$100M inflows May 12–28; XRP funds +~$120M. https://www.bitget.com/news/detail/12560605435074

[30] FXStreet, "Core PCE inflation rises to 3.3% in April as forecast," May 28, 2026. Personal income unchanged, personal spending +0.5%; DXY ~99.20 at print; markets see ~50% chance of at least one Fed hike by end-2026. https://www.fxstreet.com/news/us-core-pce-inflation-expected-to-tick-up-in-april-reinforcing-fed-hawkish-shift-202605280600

[31] CoinDesk, "Crypto slides on Hormuz airstrikes as $897 million in long liquidations pile up," May 28, 2026. ~$958M total crypto liquidations in 24h (longs $897M); ETH below $2,000; ETH futures OI record. https://www.coindesk.com/markets/2026/05/28/crypto-slides-on-hormuz-airstrikes-as-usd897-million-in-long-liquidations-pile-up

[32] CryptoTimes, "Ventuals Pledges Compensation After SPACEX Oracle Triggers $1.5M Crash," May 29, 2026. Settlement mark price $2,132 versus oracle $1,908 (>$220 premium at settlement); HIP-3 permissionless market-creation framework detail; SpaceX S-1 May 20. https://www.cryptotimes.io/2026/05/29/ventuals-pledges-compensation-after-spacex-oracle-triggers-1-5m-crash/

[33] DeFi Rate, "World Cup 2026 odds," accessed May 31, 2026. Aggregated Kalshi+Polymarket winner-contract VWAP volume $452.2M; France +485 (17.1%), Spain +490 (17.0%), England +796 (11.2%); settlement July 20, 2026. https://defirate.com/prediction-markets/world-cup-odds/

[34] Marketplace, "Fed leaders give a lot of speeches. The central bank's new chair may change that," May 19, 2026. Warsh expected to cut back Fed communications, possibly ending post-meeting press conferences. https://www.marketplace.org/story/2026/05/19/incoming-fed-chair-warsh-may-cut-back-communications

[35] CNBC, "Trump swears Kevin Warsh in as Fed chair, seeking interest rate cuts," May 22, 2026. Warsh sworn in May 22 (White House, oath by Justice Thomas); first White House Fed swearing-in since Greenspan 1987; Senate confirmation 54–45 (May 13). https://www.cnbc.com/2026/05/22/trump-kevin-warsh-fed-chair-interest-rates.html

[36] CoinMarketCap, "Hyperliquid (HYPE) price," accessed May 31, 2026. ATH $69.45 (May 31); 24h range $64.02–$69.45. https://coinmarketcap.com/currencies/hyperliquid/

[37] CoinGecko, "Hyperliquid (HYPE) price," accessed May 30, 2026. ATH $68.45 (65-exchange volume-weighted aggregate); market cap ~$15.22B; FDV ~$65.38B. https://www.coingecko.com/en/coins/hyperliquid

[38] TheStreet, "Wall Street giant's ETF suffers second-worst outflow ever," May 28, 2026. IBIT –$527.84M May 27 (second-worst), record –$528.30M January 30; IBIT cumulative net inflow since launch ~$64B, net assets ~$59.48B; IBIT closed $42.45 on May 27. https://www.thestreet.com/crypto/markets/iconic-blackrock-etf-posts-second-worst-outflow-ever

[39] Bitbase Research, "Market Insights — Issue 7," May 25, 2026. Prior-issue baselines: MSTR May 22 close $159.89; HYPE prior ATH $62.14 (May 21); stablecoin ~$322B; six-day ETF outflow streak –$1.55B; Strategy 24,869 BTC purchase, 843,738 BTC total.

[40] Bitbase Research, "Deep Dive 1" (five signals) and "Deep Dive 3" (three reverse signals). Signal-tracking framework underlying Section 5; state changes anchored to data through Friday May 29, 2026 (ET), with crypto-native data through Sunday May 31.