Macro tightening reinforced from three sides while crypto-internal catalysts remain in stasis. The April FOMC minutes released Wednesday May 20 (ET) recorded four dissents—the largest single-meeting dissent count since October 1992; Governor Christopher Waller's Friday Frankfurt address completed a public hawkish pivot from one of the prior cycle's most consistently dovish voices; and Kevin Warsh was sworn in as the 17th Chair of the Federal Reserve at a White House ceremony Friday May 22, with Supreme Court Justice Clarence Thomas administering the oath—the first Chair to take the oath at the White House since Alan Greenspan in 1987. US spot Bitcoin ETFs printed approximately –$1.26 billion in net outflows for the week, the heaviest weekly drain since late January and a continuation of the six-day outflow streak that began May 15. Simultaneously, the on-chain native track recorded its largest institutional-integration week since first U.S. Hyperliquid ETF listings: HYPE printed an intra-week all-time high of $62.14 on Thursday May 21 (approximately +42% on the week); BHYP and THYP attracted approximately $54 million in net inflows across five trading days with no net-outflow day; Bitwise committed 10% of BHYP management fees to balance-sheet HYPE accumulation; Goldman Sachs's Q1 13F disclosed full exit from XRP and SOL ETF positions with a new $3.3 million Hyperliquid Strategies allocation; and Ventuals launched the first synthetic SpaceX private-equity perpetual on HIP-3.

Week of May 18 to May 24, 2026

Bitbase Research · May 25, 2026

Market Insights is Bitbase Research's short-wave companion to our Deep Dive flagship series. Each edition reviews the most structurally meaningful developments of the preceding week in compliant crypto derivatives and on-chain native infrastructure, mapped against the long-wave framework set out in our flagship reports. The previous issue documented the collapse of the Issue 4–5 two-sided regime under macro shock and noted that the chair-pro-tempore designation of Powell pending Warsh's swearing-in was Federal Reserve Board official action; this issue records the seven-day chair-pro-tempore interval closing with Friday's White House oath, the largest single-meeting FOMC dissent count in 33 years, a public hawkish pivot from Governor Waller, and—concurrently—the assembly of a complete institutional-flow stack around Hyperliquid that constitutes the strongest non-confirmation of the Deep Dive 3 Model 5 regulatory-failure reverse signal since Deep Dive 3 publication. Deep Dive 4, published Friday May 22, is referenced in Section 4 as a forward-observation slate. All data is anchored to end-of-day Friday May 22 (ET) unless otherwise stated.

1. The one chart that matters

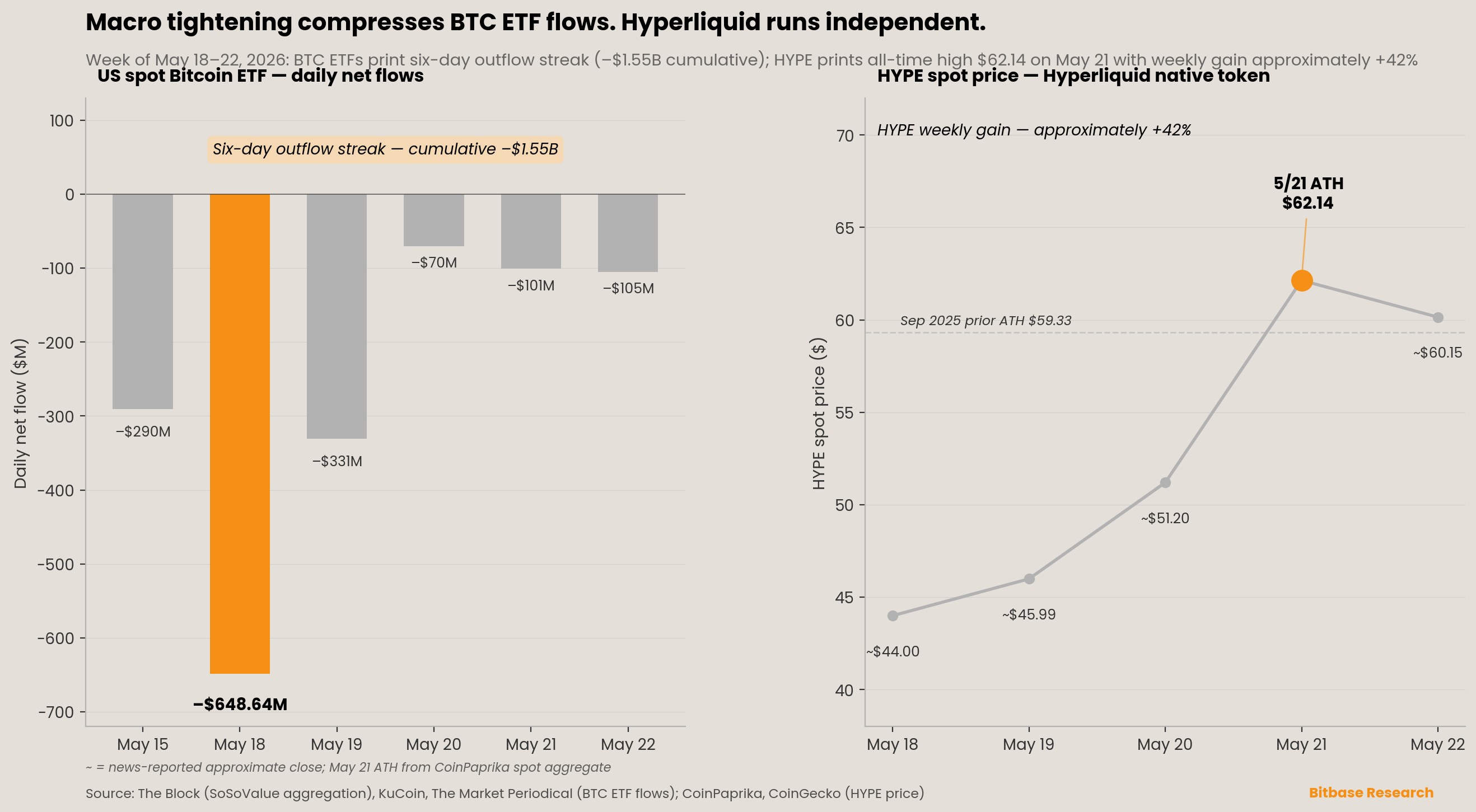

The two panels capture the bifurcation this week produced. On the left, eight trading days of US spot Bitcoin ETF flows track the transition from Issue 6's –$1.0 billion weekly print into Issue 7's six-day consecutive outflow streak. The streak began May 15 with –$290.42 million, extended through Monday May 18 at –$648.64 million (the largest single-day outflow of the entire current sequence), Tuesday May 19 at –$331.05 million, Wednesday May 20 at –$70.47 million, Thursday May 21 at –$100.82 million, and Friday May 22 at –$105.19 million [1][2][3]. The cumulative six-day total is approximately –$1.55 billion, and the full Issue 7 week (Monday May 18 through Friday May 22) printed approximately –$1.26 billion in net outflows—the heaviest weekly drain since late January and the second consecutive week of net outflows for the asset class. Cumulative net inflows since January 2024 retreated to approximately $57.1 billion (from $58.34 billion at Issue 6 close), with category aggregate net assets at approximately $98.9 billion [1]. The intra-week composition further reinforced the Issue 6 finding that the Monday-Wednesday accumulation, Thursday-Friday reversal pattern characteristic of Issues 4 and 5 has fully dissolved: this week skewed uniformly negative across all five trading days, with no single positive print on the BlackRock IBIT flagship. Friday's IBIT-specific reading was –$103.65 million; the only U.S. spot BTC ETF with a positive Friday print was Ark/21Shares' ARKB at +$2.83 million [3]. The Spot Ethereum ETF complex extended a parallel nine-day consecutive outflow streak through May 21 [4].

On the right, the Hyperliquid breakout. While BTC compressed inside a $132 weekly open-price range and ETH inside an under-$2 range, HYPE closed Thursday May 21 at $62.14 spot per CoinPaprika aggregation [5]—a fresh all-time high breaking the prior September 2025 high of approximately $59.33, with intra-week peaks of $62.16–$62.53 observed across CoinGecko, CoinMarketCap, and exchange-level feeds. The weekly gain of approximately +42% is the strongest weekly return for any top-50 digital asset by market capitalization this year. The price action coincided with the cumulative arrival of all four institutional-flow constituents during the week itself: BHYP and THYP combined net inflows of approximately $54 million over the five trading days with no net-outflow day, peaking at $25.5 million on May 20 [6][7]; Bitwise's Monday May 18 commitment to allocate 10% of BHYP management fees to balance-sheet HYPE accumulation under a 12-month lock [8][9]; Goldman Sachs's May 15 Q1 13F disclosure of full XRP ETF and SOL ETF exits with a new $3.3 million PURR (Hyperliquid Strategies) position opened [10]; and Ventuals's launch of SPCX-USDC synthetic perpetual on HIP-3 on Monday May 18 with approximately $33 million first-day volume [11]. The conjunction is not coincidental: each constituent reinforces the others, and the price tape responded to the cumulative arrival rather than any single component. The DD3 Model 5 reverse signal—originally posited as the regulatory-failure scenario for the on-chain native model with U.S.-regulated wrapper—is now maximally non-confirming, the strongest read since Deep Dive 3 publication in April. The contrast between the left and right panels is the structural signal of the week: macro tightening compressing BTC ETF flows and spot price simultaneously while the on-chain native track executes its largest institutional integration week since the Bitwise/21Shares/Grayscale Hyperliquid ETF cohort filed in early 2026.

2. This week's structural signal

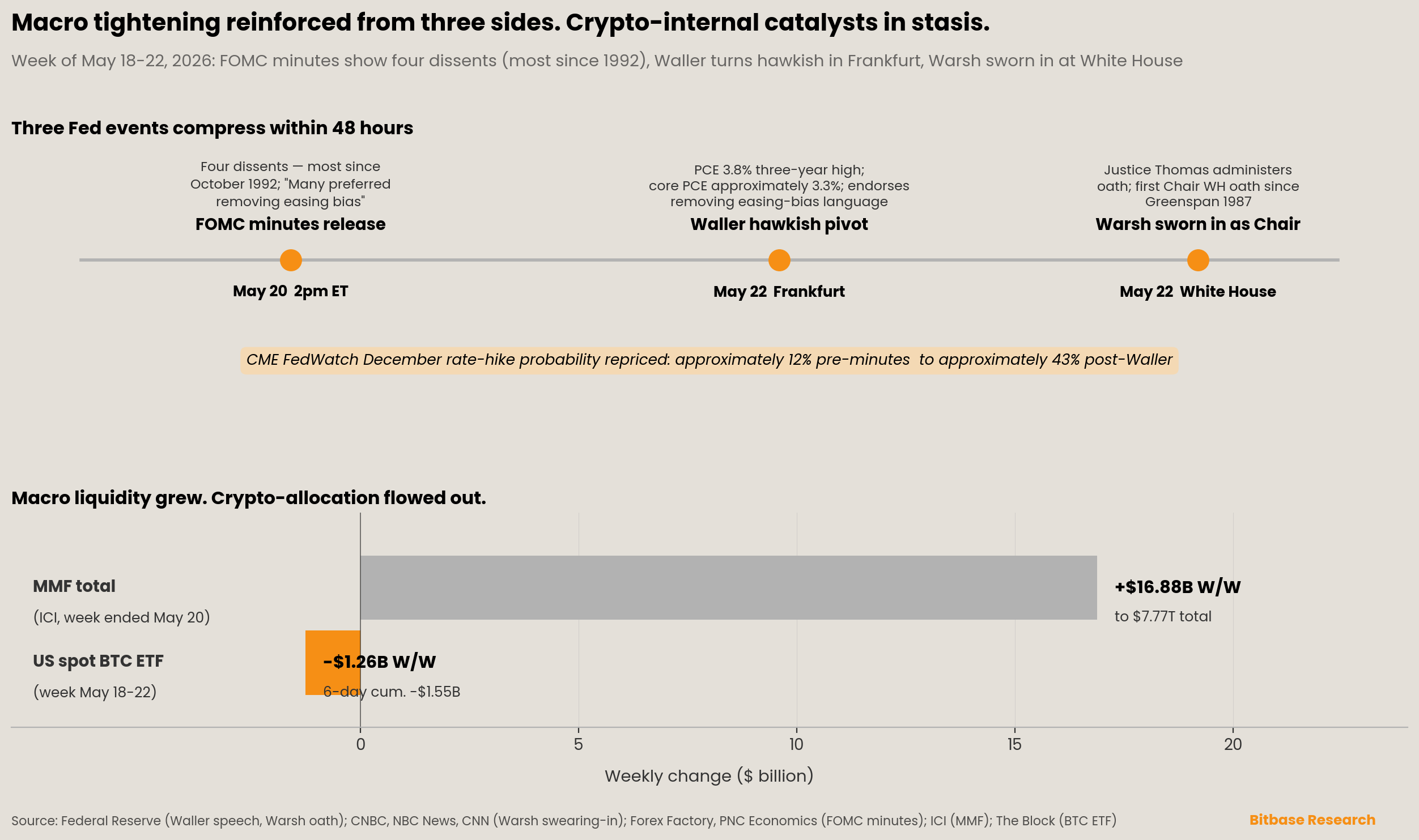

The structural signal of the week is macro tightening reinforced from three sides simultaneously while crypto-internal catalysts remain in stasis. The Issue 6 thesis that macro variables had overrun crypto catalysts within a single 24-hour window held through this entire five-day window without exception. Three developments compound: the Federal Reserve transition completed in form via Friday's White House swearing-in; the April 28–29 FOMC minutes released Wednesday revealed a four-dissent hawkish pivot inside the institution; and Governor Christopher Waller's Friday Frankfurt address marked a public hawkish reversal from one of the prior cycle's most consistent dovish voices.

First, the Federal Reserve transition completed in ceremony on Friday May 22, seven days after Powell's term as Chair ended. Issue 6 reported that Kevin Warsh had been confirmed by the Senate 54-45 on May 13 and that Powell was named "chair pro tempore" pending Warsh's swearing-in; the swearing-in itself occurred at the White House East Room on Friday May 22, with Supreme Court Justice Clarence Thomas administering the oath and Warsh's wife Jane Lauder holding the Bible [12]. The ceremony was attended by Justice Brett Kavanaugh, Treasury Secretary Scott Bessent, Transportation Secretary Sean Duffy, Agriculture Secretary Brooke Rollins, Speaker Mike Johnson, House Majority Leader Steve Scalise, Council of Economic Advisers Chair Kevin Hassett, former Secretary of State Condoleezza Rice, and Virginia Governor Glenn Youngkin [12]. The White House venue is itself a departure: the most recent comparable Federal Reserve Chair oath at the White House was Alan Greenspan's in 1987 [13]. President Trump's remarks at the ceremony directly addressed the institutional independence question: "I want Kevin to be totally independent... Don't look at me, don't look at anybody, just do your own thing, and do a great job." [14]. Warsh's first Chair-capacity remarks framed the institutional posture: "Our mandate at the Fed is to promote price stability and maximum employment... To fulfill this mission, I will lead a reform-oriented Federal Reserve, learning from past successes and mistakes, both escaping static frameworks and models, and upholding clear standards of integrity and performance." [14]. Powell remains on the Board of Governors with a term running through January 2028. Warsh's first FOMC meeting as Chair is scheduled June 16–17, 2026 [15]. The seven-day chair-pro-tempore interval between Powell's term-end (May 15) and Warsh's swearing-in (May 22) is the longest such interval since the 1948 Eccles–McCabe transition.

Second, the April 28–29 FOMC minutes released Wednesday May 20 at 2:00 PM ET revealed an institutional hawkish pivot that materially exceeded the visible voting record from the April meeting. The minutes' standout phrases: "Many preferred removing easing bias from statement"; "Majority saw hike likely warranted if inflation persists"; "Some were concerned inflation expectations could de-anchor"; "Officials generally judged rate pause will extend longer than previously thought" [16][17]. The April meeting vote was 8–4 with four dissents [18]: Stephen Miran dissenting in favor of cutting; and Beth Hammack (Cleveland), Neel Kashkari (Minneapolis), and Lorie Logan (Dallas) dissenting against the retention of easing-bias language in the statement. As multiple commentators noted, "the last time four FOMC members dissented was in October 1992" [18]. The minutes were released into a market that had been positioning around a base case of one rate cut by year-end; the publication did not produce a sharp same-day reaction (PNC Economics: "There was little reaction in stock and bond markets to the release of the minutes." [17]) but it reset the medium-term distribution of FOMC outcomes.

Third, Governor Christopher Waller's address Friday May 22 in Frankfurt completed the hawkish shift in public communication. In "Policy Risks Have Changed" delivered at the European Central Bank, Waller stated that personal consumption expenditures inflation "rose around 3.8 percent over the previous 12 months, the highest in three years" with core PCE running at approximately 3.3% year-over-year on the most recent twelve-month basis—the highest core reading in approximately two and a half years [19]. Waller endorsed removing the easing-bias language and used a coin-toss analogy to argue that successive supply shocks compounding into base inflation expectations could de-anchor in ways that conventional models do not capture. Waller's position is consequential because he was, through the prior cycle, among the most consistently dovish-leaning Governors; the rotation of his public stance is therefore a regime indicator, not noise within an established distribution. By Friday evening, CME FedWatch had repriced December rate-hike probabilities to approximately 43% on a 25-basis-point increment—from approximately 12% pre-minutes [20]. This is the most consequential change in market-implied Fed path since the November 2025 cycle inflection.

The macro pricing through the week stayed within a tight band that reflected the absorption rather than rejection of the tightening signal. The 10-year Treasury yield closed Friday at 4.56% [21]—three basis points below Issue 6's 4.59% close, but with intraday testing of 4.62% on Wednesday following the minutes. The dollar index closed at 99.319 [22], one basis point above Issue 6's 99.27 close. Bitcoin spot opened the week at approximately $77,447 (Fortune snapshot, Monday May 18, 9:15 AM ET [23]) and closed Friday May 22 morning at approximately $77,289 (Yahoo Finance, Friday 7:55 AM ET intraday low [24]). The full five-day open-price range across May 18–22 was approximately $132—a remarkably tight band, with similar compression in ETH spot (under $2 of opening-price range). The macro signal tightened; the price signal compressed; the resolution variable becomes ETF flow.

3. Dual-track scoreboard

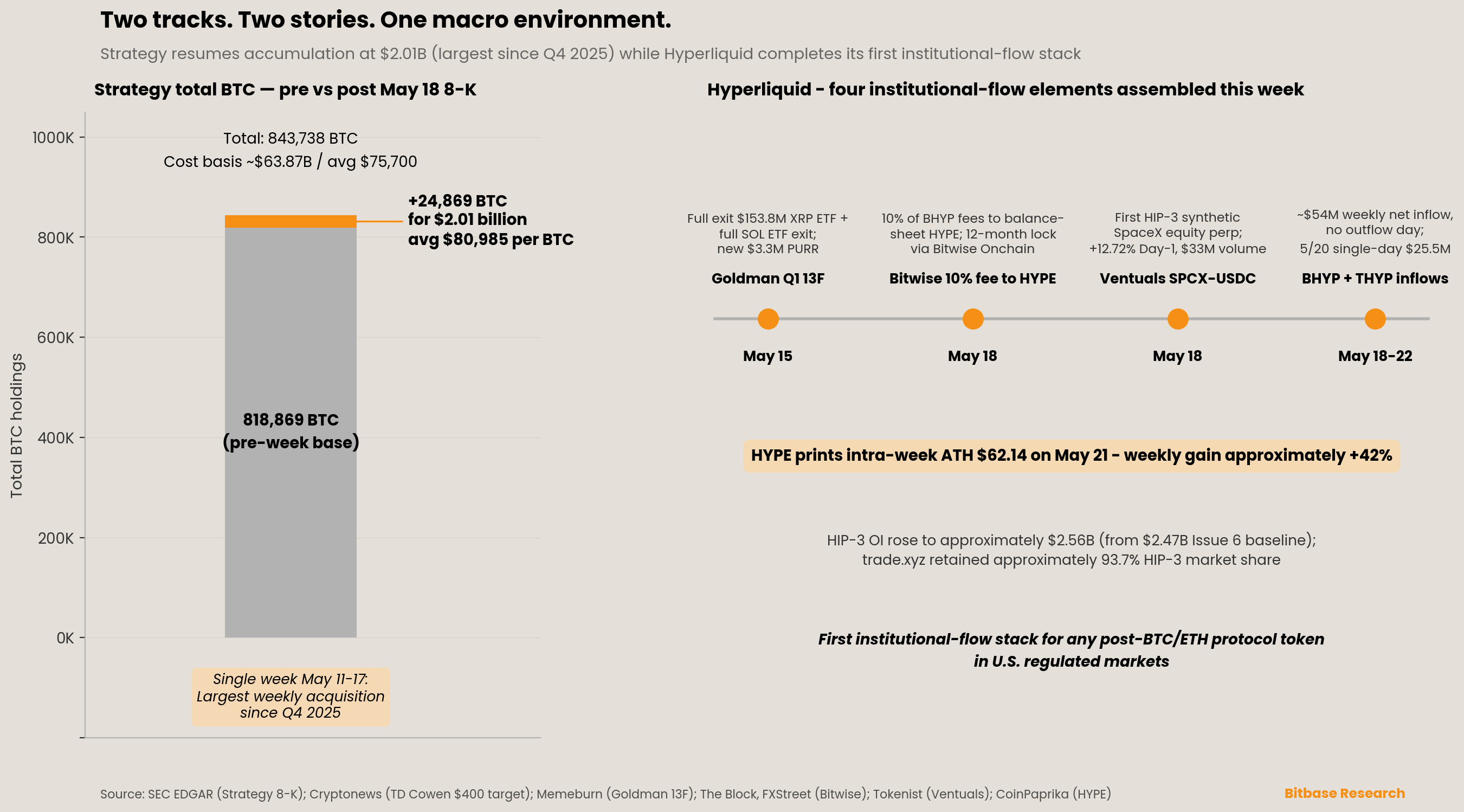

Compliant-centralized track. Strategy resumed institutional-scale accumulation at unusual magnitude. An 8-K filed Monday May 18 disclosed the purchase of 24,869 BTC for approximately $2.01 billion at an average price of $80,985 during the week of May 11–17 [25]. Total holdings now stand at 843,738 BTC (up from a pre-week base of 818,869 BTC) at aggregate cost basis of approximately $63.87 billion, average $75,700 per BTC [25]. This single-week purchase exceeds the cumulative purchases of the four preceding weeks combined and is the largest weekly acquisition since the fourth quarter of 2025; the company has now ended its two-week zero-purchase pause (weeks of April 27 and May 4) with a single print that materially increases position size. TD Cowen analyst Lance Vitanza raised MSTR's 12-month price target Tuesday May 19 from $395 to $400, maintaining a Buy rating, with the $5 increase driven by upward revisions to TD Cowen's 2026 BTC Yield and BTC Dollar Gain estimates after Q2 treasury activity surpassed the firm's prior model; the valuation framework applies a 3x multiple to projected 2026 BTC Dollar Gain of approximately $15.16 billion, adds projected year-end bitcoin holdings of $132.9 billion, and subtracts $3.5 billion in debt and $15.5 billion in preferred equity obligations [26]. The market reaction was inconsistent with the disclosure direction: MSTR closed Friday May 22 at $159.89, down 3.01% on the day and approximately 9.88% lower than the May 15 close of $177.42 [27]; for the year-to-date the stock is down approximately 60% per multiple coverage aggregations. Yahoo Finance summary commentary noted that "MicroStrategy is shifting its Bitcoin strategy, now considering limited sales to manage obligations" [28]—a position framing that has not appeared in Strategy's own filings or executive commentary, but that is reflected in the equity tape. The accumulation-action versus equity-reaction divergence is the cleanest single observation this quarter on the long-wave question of whether the corporate-treasury BTC adoption channel is operationally durable through bear-tape pricing. The Jane Street IBIT 71% reduction disclosed in Q1 13F filings (noted in Issue 6) remains the prior quarter's marker; the next 13F reporting cycle (Q2, due mid-August) will be the comparable data point.

On-chain native track. The week's signature event for the on-chain native track was Hyperliquid completing what amounts to the first institutional-flow stack for any post-Bitcoin/Ethereum protocol native token in U.S. regulated markets. The constituent elements assembled during the week, and the cumulative effect is larger than any single component. HYPE closed Thursday May 21 at an intra-day all-time high of $62.14 spot [5]—a roughly 42% weekly gain that broke the prior September 2025 high of approximately $59.33. Bitwise's BHYP and 21Shares' THYP attracted approximately $54 million in net inflows across the five trading days, with no net-outflow day; the May 20 single-day reading of $25.5 million (BHYP $8.8 million plus THYP $16.6 million) was the strongest of the week [6][7]. THYP's first-week assets under management reached approximately $37.2 million per 21Shares' own week-one disclosure, with cumulative net inflows of $24.4 million [29]. Bitwise's Monday May 18 announcement that 10% of BHYP management fees will be directed to balance-sheet HYPE accumulation, staked through Bitwise Onchain Solutions and locked for at least 12 months, has no precedent among U.S. spot crypto ETFs and creates a structural revenue-recycling loop between the regulated wrapper and the native token [8][9]. Goldman Sachs's Q1 13F filing made public May 15 disclosed full exit from approximately $153.8 million in XRP ETF holdings, full exit from its SOL ETF position, and a new $3.3 million PURR (Hyperliquid Strategies) position [10]—the first disclosed major prime-broker Hyperliquid-related allocation. HIP-3 deployed-market open interest rose to approximately $2.56 billion mid-week per Loris.tools [30], from the $2.47 billion Issue 6 baseline; trade.xyz retained approximately 93.7% of HIP-3 share [31]. The HIP-3 / core perpetual OI inversion documented in Issue 6 sustained into a second observed week. Ventuals's May 18 launch of SPCX-USDC—a synthetic perpetual referencing SpaceX private-market equity—opened at $208 against a $150 reference, closed at $202.89 (+12.72%), and traded approximately $33 million in volume on the first day [11], extending the HIP-3 builder ecosystem into tokenized private-equity exposure on the same venue housing the crypto-derivatives liquidity.

TradFi-perpetual & tokenized-RWA layer. No new BitMEX or third-party quarterly TradFi-perpetual data published this week; the Q1 2026 baseline ($30.7 billion weekly TradFi-perpetual volume) remains the reference. CME Group's confirmed May 29 launch of 24/7 (around-the-clock) cryptocurrency futures and options trading, announced February 19, 2026, is operationally inside the existing CME framework and does not constitute new CFTC-perpetual evidence [32]; the relevant signal D1-Part 6 status continues at twelve weeks overdue without further movement. Hyperliquid's network-aggregate RWA open interest reached approximately $2.6 billion mid-month, roughly doubled in two months, with cumulative tokenized-stock turnover peaking at approximately $3.57 billion [33]. The Ventuals SPCX launch is most consequential at this layer: a U.S.-domiciled private-equity exposure made tradeable as a perpetual contract via a HIP-3 builder, settled and margined alongside crypto pairs, with the synthetic price discovery sustaining a 12.7% first-day premium against the reference. Brent crude closed near $105 per barrel with WTI near $97, weekly moves in the –4 to –6% range [34]; the Strategic Petroleum Reserve drew down approximately 10 million barrels in the week ended May 16, the largest weekly drain on record, with total reserves now below 375 million barrels [35]. Stablecoin total market capitalization remained near the Issue 6 reading of approximately $322 billion; the GENIUS Act compliance trigger date of July 18, 2026 is approximately 8 weeks out [36].

4. On the radar—week of May 25 to May 31

-

Warsh's first public statement as Chair, ahead of the June 16–17 FOMC meeting. The seven-day chair-pro-tempore transition window has closed; Warsh's communication path now sets the FOMC reaction function. Any forward guidance from Warsh in the first week post-swearing-in—through public speech, congressional appearance, or background-attributed press—will be Tier-1 market-moving and the most consequential single observable for the remainder of the quarter. A continuation of the Waller hawkish framing would push December rate-hike probability well above 50%; any dovish surprise would unwind the bond-yield premium accumulated since early May.

-

Strategy 8-K filing window opens Monday May 25 (week of May 18–24 purchases). This week's $2.01 billion single-week acquisition resolved the two-week pause but at exceptional scale. A follow-up filing showing continued large-magnitude accumulation would confirm a structural reset in the funding cadence; a return to small-scale or zero purchase would frame the May 11–17 print as a one-off catch-up rather than a regime restart. The funding-mix detail (common-stock ATM versus preferred-share issuance proportions) is the key inner variable.

-

HYPE post-ATH holding pattern: $50 support and BHYP/THYP second-week flow durability. The first-week institutional-flow stack is now publicly visible. The second-week behavior is the durability test. If BHYP and THYP combined inflows hold above approximately $30 million on the week with no single-day net outflow, the institutional-flow channel is empirically confirmed; if inflows collapse to single-digit millions or print net outflows, the May 18–22 institutional-arrival burst may not extend into a sustained flow regime.

-

HIP-3 builder diversification beyond trade.xyz. trade.xyz's 93.7% share is the central concentration risk for the on-chain native track's structural read. Ventuals's SPCX debut is the second material HIP-3 builder this quarter to attract meaningful first-day volume; any third builder reaching a $20 million+ daily volume floor would begin to dilute the concentration. Watch for new HIP-3 deployments specifically in tokenized U.S. equities (single-stock perpetuals), commodity perpetuals (oil, gold), or rates exposure (Treasury yield perpetuals).

-

BTC ETF six-day outflow streak: extension or break. Any single net-positive day breaks the streak; a seventh consecutive negative day extends it to the longest outflow run since late January. Either resolution is informative. A break with a magnitude greater than the prior outflows (a single day above +$300 million) would suggest tactical reallocation rather than directional buying; a single day in the +$50–150 million range would suggest market-maker rebalancing rather than fresh institutional commitment.

-

MMF plateau softening: directional confirmation or reversal. The +$16.88 billion week-over-week ICI print to $7.77 trillion is one data point. A second consecutive week of growth above $20 billion would reposition the DD1-P1 signal toward "renewed accumulation"; a sharp reversal below $7.745 trillion would restore the "plateau-fixed" Issue 6 framing. The Strait of Hormuz flow status and Brent crude path are the upstream variables; Brent breaking below $100 would likely catalyze MMF reflux.

-

CFTC perpetual framework week 13 and Senate Clarity Act floor scheduling. Twelve weeks of administrative silence with one week of legislative silence is the current configuration. The Witt White House target of a July 4 presidential signature implies a Senate floor vote in early to mid-June; absence of scheduling through this week would compress that timeline materially. Any Selig CFTC framework release this week would be a complete inflection in the long-standing administrative-stasis read.

-

DD4 reverse-signal observation slate—first formal inclusion. Bitbase Research's Deep Dive 4 ("When Momentum Breaks: A Structural Framework for Reading Meme Markets") published May 22 enumerates four falsification conditions in Chapter 7 [37]: peer-reviewed evidence of canonical RSI/MACD directional accuracy on memecoins within five percentage points of major-cap crypto accuracy at 1% statistical significance; published memecoin-specific parameter recalibration producing stable risk-adjusted excess returns with White (2000) reality-check applied; empirical work explaining memecoin returns through Fama–French extensions at 30%+ R-squared; Granger causality tests demonstrating that abnormal search and social-mention metrics do not lead memecoin prices at 10% significance. None have triggered in the first week post-publication; all four are entered into the Market Insights observation slate. Activation criteria: any peer-reviewed publication, regulatory-document-level analysis, or Bitbase internal backtest meeting the threshold conditions will be elevated to a formal Section 5 SIGNAL block in a subsequent issue.

5. Signal tracking update

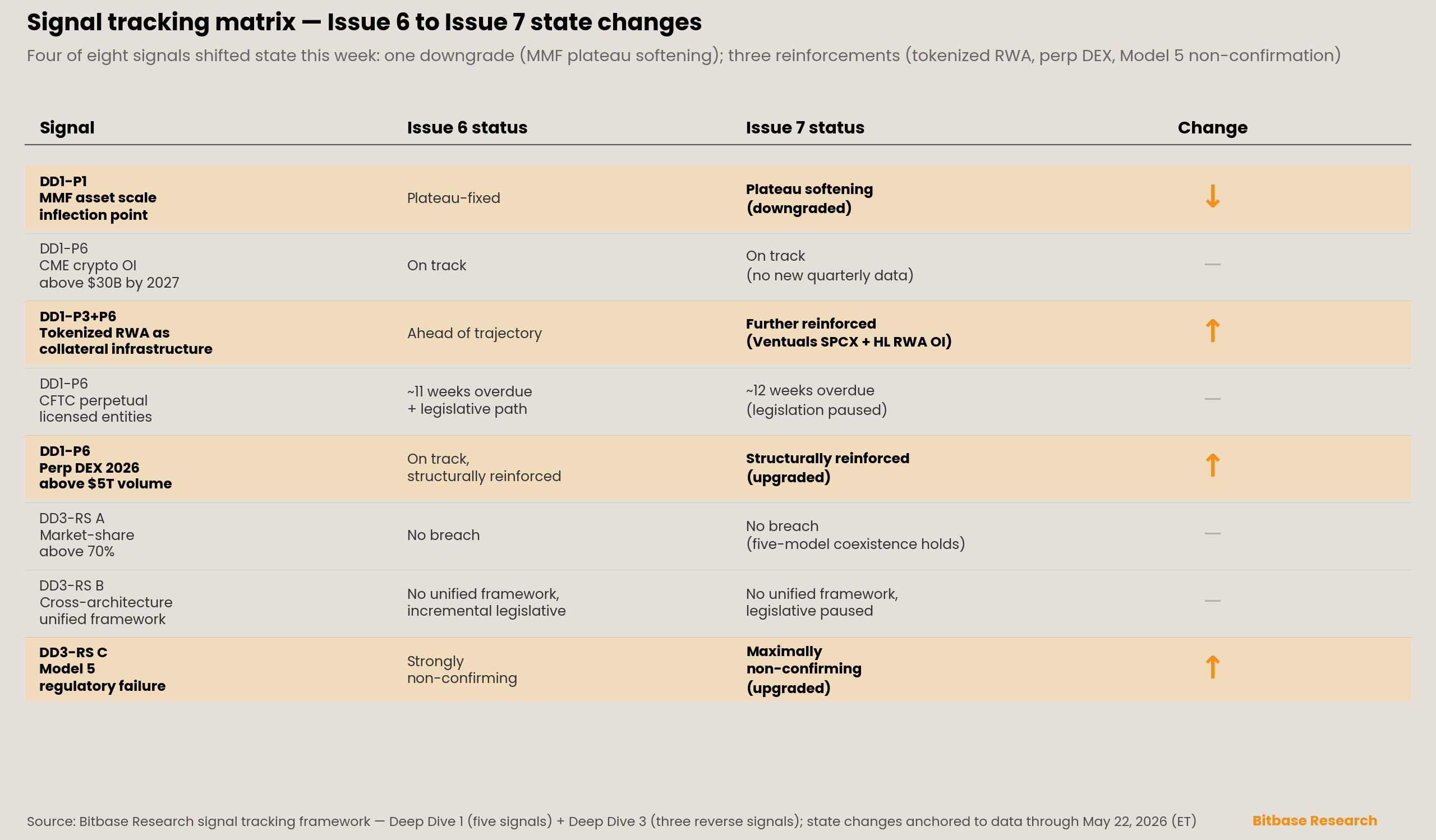

Five Deep Dive 1 signals plus three Deep Dive 3 reverse signals remain under continuous audit. This issue records four signals shifting state—matching Issue 5 and Issue 6 as the largest single-issue change since tracking began. Three of the four moves are reinforcing on-chain-native and tokenized-RWA infrastructure; one is a mild softening of the MMF plateau call from Issue 6.

SIGNAL—Deep Dive 1 Part 1: "MMF asset scale inflection point." STATUS: Plateau softening (downgraded from "plateau-fixed" in Issue 6). ICI's May 21 release (ET) reported total MMF assets at $7.77 trillion for the week ended May 20, a +$16.88 billion week-over-week increase composed of +$16.34 billion in government MMF, +$946 million in prime, and –$409 million in tax-exempt; retail funds rose +$4.04 billion to $3.09 trillion [38]. The single-week reading is the strongest since the geopolitically-driven +$122.35 billion print of early May. The Issue 6 "plateau-fixed" characterization was premised on near-flat readings; one week of mid-double-digit-billion growth is not by itself a regime change, but it is sufficient to retire the "fixed" descriptor and replace it with "softening." Strait of Hormuz flow remained depressed through the week; Brent traded near $105 per barrel with WTI near $97, both down 4–6% week-over-week [34]. The Strategic Petroleum Reserve drew down approximately 10 million barrels in the week ended May 16—the largest weekly drain on record, total reserves now below 375 million barrels [35]. The signal cannot return to confirmation status until the geopolitical premium drains and assets revert below $7.70 trillion; the current $7.77 trillion reading is moving in the opposite direction.

SIGNAL—Deep Dive 1 Part 6: "Whether CME crypto derivatives OI persistently holds above $30B by 2027." STATUS: On track, no new quarterly data. CME's previously announced 24/7 (around-the-clock) cryptocurrency futures and options trading launches Friday May 29, 2026 at 4:00 PM Central Time [32]—a microstructure expansion that is operationally distinct from the CFTC perpetual-futures framework pending under Signal D1-Part 6 below. The 24/7 expansion may bear on aggregate CME OI in subsequent quarters but does not yet constitute observable evidence for or against the $30 billion 2027 threshold. Signal evaluation continues against full-year 2026 and 2027 data when published.

SIGNAL—Deep Dive 1 Parts 3 and 6: "Tokenized RWA as common collateral infrastructure." STATUS: Further reinforced. Two material developments converged this week. First, Ventuals went live on Hyperliquid's HIP-3 framework on Monday May 18 with SPCX-USDC, a synthetic perpetual referencing SpaceX private-market equity; reference price was $150, open print $208, close $202.89 (+12.72% on debut), with first-day volume of approximately $33 million [11]. Second, Hyperliquid network-aggregate RWA open interest reached approximately $2.6 billion mid-month—roughly doubled in two months—with cumulative tokenized-stock turnover peaking at approximately $3.57 billion [33]. The structural significance is not the dollar amount but the asset-class boundary: tokenized U.S. Treasuries now joined by synthetic exposure to one of the most-watched private equities, on the same on-chain venue, with the same margin and settlement infrastructure. No major new cross-border atomic settlement followed the May 6 Ondo-JPMorgan-Mastercard-Ripple event noted in Issue 5; institutional integration of the tokenized Treasury layer remains in the evaluation period observed last issue, while the synthetic-equity layer expanded.

SIGNAL—Deep Dive 1 Part 6: "Whether the U.S. CFTC approves more licensed entities to offer perpetual swap-style products by 2027." STATUS: Commitment now approximately 12 weeks overdue. Acting Chair Caroline Pham's deputy successor framework remains unfilled; Selig's March 3 commitment of "next month or so" reached the twelve-week mark Friday May 22 with no staff letter, no-action position, or rulemaking published. The CFTC continues to operate with limited Senate-confirmed leadership. The Clarity Act parallel legislative track established by Senate Banking Committee's May 14 vote saw no further movement this week—no full-Senate scheduling, no manager's amendment, no Witt White House statement on the previously-stated July 4 signing target. Both tracks are now in observable stasis; the administrative-stasis read from Issue 6 is unchanged, and the legislative-momentum read from Issue 6 has paused for one full week.

SIGNAL—Deep Dive 1 Part 6: "Whether perpetual DEX annual trading volume holds above $5 trillion in 2026." STATUS: Structurally reinforced—upgraded. Three independent developments tracked this week strengthen the signal beyond the Issue 6 reading. First, HYPE printed an intra-week all-time high of $62.14 on Thursday May 21 (CoinPaprika spot-aggregated; CoinGecko and CoinMarketCap show $62.16–$62.53 across exchange feeds), with weekly gain of approximately +42% [5]. Second, BHYP and THYP combined attracted approximately $54 million in net inflows over the five trading days, with zero net-outflow days; the May 20 single-day reading of $25.5 million was the strongest of the week (THYP $16.6 million plus BHYP $8.8 million), followed by $16.15 million on May 21 [6][7]. Third, Bitwise announced Monday May 18 via its official social channel that 10% of BHYP management fees will be allocated to direct purchase of HYPE for the firm's balance sheet, with the acquired HYPE staked through Bitwise Onchain Solutions and a 12-month lock-up: "In that spirit, we're pleased to announce that Bitwise will be devoting 10% of the Bitwise Hyperliquid ETF ($BHYP) management fee to holding HYPE on the Bitwise balance sheet." [8]. The fee-to-treasury structure has no precedent in the U.S. spot crypto ETF universe and constitutes a new institutional-flow vector for the underlying token. HIP-3 deployed-market open interest rose to approximately $2.56 billion mid-week per Loris.tools on-chain telemetry [30], from the $2.47 billion Issue 6 baseline. trade.xyz retained roughly 93.7% of HIP-3 market share through the week per Bitget aggregation [31]. The HIP-3 / core perp OI inversion documented in Issue 6 sustains into the second observed week.

SIGNAL (Deep Dive 3 Reverse Signal A)—Market-share concentration above 70%. STATUS: No model concentration breach. BitMEX's Q1 attribution (Binance 62.7%, Hyperliquid 29.7%) remains the most recent independent baseline; Coinbase U.S. derivatives share continues around 63%. No new third-party data published this week. The five-model coexistence thesis from Deep Dive 3 holds.

SIGNAL (Deep Dive 3 Reverse Signal B)—Cross-architecture unified regulatory framework. STATUS: No unified framework; legislative momentum paused for one week. The Clarity Act remained in committee-passed-but-unscheduled status through the week. No new ESMA, FCA, MAS, JFSA, BIS, or Basel statements were issued. The CME 24/7 cryptocurrency futures and options expansion launching May 29 [32] is a venue-microstructure change inside the existing U.S. designated-contract-market framework, not a cross-jurisdiction harmonization step. The Hong Kong Monetary Authority did not announce a third stablecoin license following the HSBC and Anchorpoint pair from April. The five-model regulatory divergence documented in Deep Dive 3 remains the state of record.

SIGNAL (Deep Dive 3 Reverse Signal C)—Model 5 regulatory failure. STATUS: Maximally non-confirming. Four developments this week strengthen the non-confirmation beyond Issue 6's "strongly non-confirming" read. First, Bitwise's commitment to allocate 10% of BHYP management fees to direct HYPE accumulation [8][9]—a structural innovation that channels U.S.-regulated ETF revenue into the native protocol token—has no analog elsewhere in the U.S. spot crypto ETF set. Second, Ventuals's May 18 SPCX-USDC launch [11] extends the HIP-3 builder ecosystem into synthetic equity exposure on the same venue that houses crypto perpetuals. Third, Goldman Sachs's Q1 2026 13F filing (made public May 15) disclosed exit from $153.8 million in XRP ETF and full exit from its SOL ETF position, while opening a new $3.3 million PURR (Hyperliquid Strategies) position [10]—the first major prime-broker disclosed Hyperliquid-related equity allocation. Fourth, weekly net ETF inflows of approximately $54 million across BHYP and THYP [6][7] sustain through the entire first full trading week post-launch with no single-day outflow. No transaction has been blocked, unwound, or restructured. The Model 5 convergence rail—on-chain native execution wrapped by U.S.-regulated capital access and now augmented by U.S.-regulated capital recycled back into the token—is empirically further strengthened. The signal direction is now maximally non-confirming of the Model 5 regulatory-failure hypothesis posed in Deep Dive 3.

Caveats

This issue's principal numerical claims are anchored to source disclosures available through Friday May 22, 2026 (ET). U.S. spot Bitcoin ETF net flow figures are sourced primarily from SoSoValue's daily aggregation as referenced by The Block's May 25 weekly summary; Farside Investors aggregations may differ by single-digit-million amounts depending on whether reporting cutoffs include intraday creations and redemptions. The HYPE all-time high of $62.14 on May 21 references CoinPaprika's exchange-aggregated spot reading; intraday peaks of $62.16–$62.53 are observed across CoinGecko, CoinMarketCap, and exchange-level feeds with the variance reflecting venue-specific liquidity. The HIP-3 open interest figure of approximately $2.56 billion mid-week is sourced from Loris.tools on-chain telemetry; comparable readings on ASXN and other on-chain analytics platforms may differ by single-digit-percent amounts depending on the aggregation window. Strategy's weekly BTC acquisition cost basis is taken directly from the company's May 18 8-K filing; market-cap-weighted average prices may vary slightly depending on the intra-week timing of individual purchases not separately disclosed. The CME FedWatch December rate-hike probability of approximately 43% is a real-time post-Waller reading captured Friday evening and is expected to evolve materially as additional Fed communication arrives ahead of the June 16–17 FOMC. None of the foregoing is investment advice; investors should consult their own qualified advisors and independent diligence before making any investment decision based on the data points discussed.

References

[1] The Block, "U.S. spot bitcoin ETFs end week with $1.26B in cumulative outflows, six-day streak totals $1.55B," May 25, 2026. SoSoValue weekly summary, cumulative net inflows $57.1B and category net assets $98.9B. https://www.theblock.co/

[2] KuCoin, "U.S. Spot Bitcoin ETFs Record $649M Net Outflow on May 18," May 19, 2026. https://www.kucoin.com/news/flash/u-s-spot-bitcoin-etfs-record-649m-net-outflow-on-may-18

[3] The Market Periodical, "Bitcoin ETFs See $101M Outflows, Extend Losing Streak to 5 Days," May 22, 2026. IBIT –$103.65M; ARKB +$2.83M. https://themarketperiodical.com/2026/05/22/bitcoin-etfs-see-101m-outflows-extend-losing-streak-to-5-days/

[4] Farside Investors, "Spot Ethereum ETF Flow Data," accessed May 25, 2026. Nine-day consecutive outflow streak through May 21. https://farside.co.uk/eth/

[5] CoinPaprika, "Hyperliquid ETFs Draw $54 Million in Launch Week as HYPE Hits All-Time High," May 22, 2026. HYPE all-time high $62.14 May 21; weekly gain ~+42%. https://coinpaprika.com/news/hyperliquid-etfs-draw-54-million-launch-week/

[6] The Block, "Hyperliquid ETFs see $25M inflows on May 20," May 21, 2026. BHYP $8.8M + THYP $16.6M = $25.5M. https://www.theblock.co/post/402120/hyperliquid-etfs-25-million-inflows

[7] CoinMarketCap, "HYPE ETFs Record 50% Volume Jump and $25.5M in Daily Inflows," May 21, 2026. https://coinmarketcap.com/academy/article/hype-etfs-volume-inflows-surge

[8] The Block, "Bitwise to add HYPE to balance sheet using fees from Hyperliquid ETF," May 19, 2026. Bitwise official X announcement May 18; full quote: "In that spirit, we're pleased to announce that Bitwise will be devoting 10% of the Bitwise Hyperliquid ETF ($BHYP) management fee to holding HYPE on the Bitwise balance sheet." https://www.theblock.co/post/401688/bitwise-add-hype-balance-sheet-fees-hyperliquid-etf

[9] FXStreet, "Bitwise to allocate 10% of BHYP ETF fees to HYPE treasury," May 19, 2026. 12-month lock-up; staking through Bitwise Onchain Solutions. https://www.fxstreet.com/cryptocurrencies/news/bitwise-to-allocate-10-of-bhyp-etf-fees-to-hype-treasury-202605190021

[10] Memeburn, "Goldman Sachs Sells XRP and SOL ETF, Pivots to Hyperliquid in Q1 2026," May 16, 2026. Q1 13F filing made public May 15: full exit $153.8M XRP ETF, full exit SOL ETF, new $3.3M PURR (Hyperliquid Strategies). https://memeburn.com/goldman-sachs-sells-xrp-and-sol-etf-pivots-to-hyperliquid-in-q1-2026/

[11] Tokenist, "SpaceX Pre-IPO Market Goes On-Chain: Hyperliquid Launches Synthetic Trading," May 19, 2026. Ventuals SPCX-USDC launch May 18; reference $150, open $208, close $202.89 (+12.72%), first-day volume ~$33M. https://tokenist.com/spacex-pre-ipo-hyperliquid-synthetic-trading/

[12] NBC News, "Warsh sworn in as Federal Reserve Chair—live updates," May 22, 2026. White House East Room ceremony; Justice Clarence Thomas administered oath; attendee list including Kavanaugh, Bessent, Duffy, Rollins, Johnson, Scalise, Hassett, Rice, Youngkin. https://www.nbcnews.com/politics/trump-administration/live-blog/trump-fed-chair-warsh-mike-lawler-ice-budget-iran-live-updates-rcna346431

[13] CNN, "Kevin Warsh sworn in as 17th Fed Chair," May 22, 2026. Greenspan 1987 White House precedent. https://www.cnn.com/2026/05/22/economy/kevin-warsh-sworn-in-fed-chair

[14] CNBC, "Trump on Warsh swearing-in: 'I want Kevin to be totally independent,'" May 22, 2026. Trump quote and Warsh inaugural address. https://www.cnbc.com/2026/05/22/trump-kevin-warsh-fed-chair-interest-rates.html

[15] Federal Reserve, "Meeting calendars and information," accessed May 25, 2026. June 16–17, 2026 FOMC. https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm

[16] Forex Factory, "US FOMC Meeting Minutes—May 20, 2026 release," accessed May 25, 2026. Standout phrases on easing bias, hike conditionality, inflation expectations. https://www.forexfactory.com/calendar/304-us-fomc-meeting-minutes

[17] PNC Economics, "FOMC Minutes—20 May 2026," May 20, 2026. Market reaction commentary. https://www.pnc.com/content/dam/pnc-com/pdf/aboutpnc/EconomicReports/EconomicUpdates/2026/PNC\_Economics\_Research\_FOMC\_Minutes\_20\_May\_2026.pdf

[18] CNBC, "Fed interest rate decision April 2026: Fed holds rates steady amid dissent," April 29, 2026. 8–4 vote; Miran dissent for cut; Hammack, Kashkari, Logan dissents against easing-bias language; October 1992 last comparable four-dissent count. https://www.cnbc.com/2026/04/29/fed-interest-rate-decision-april-2026.html

[19] Federal Reserve, "Governor Christopher J. Waller—'Policy Risks Have Changed,'" Frankfurt, Germany, May 22, 2026. PCE 3.8% headline three-year high; core PCE 3.3% approximately. https://www.federalreserve.gov/newsevents/speech/waller20260522a.htm

[20] TheStreet, "CME FedWatch repricing post-Waller, December rate-hike probability ~43%," May 23, 2026. https://www.thestreet.com/

[21] Advisor Perspectives, "Treasury Yields Snapshot: May 22, 2026," May 22, 2026. 10Y 4.56%; 2Y 4.13%; intraday testing 4.62% mid-week. https://www.advisorperspectives.com/dshort/updates/2026/05/22/treasury-yields-snapshot-may-22-2026

[22] CNBC, "ICE U.S. Dollar Index (.DXY) real-time quote," accessed May 25, 2026. May 22 close 99.319. https://www.cnbc.com/quotes/.DXY

[23] Fortune, "Current price of Bitcoin for May 18, 2026," May 18, 2026. 9:15 AM ET reading ~$77,447.38. https://fortune.com/article/price-of-bitcoin-05-18-2026/

[24] Yahoo Finance, "Bitcoin and ethereum prices today, Friday, May 22, 2026: Prices moved little this week," May 22, 2026. 7:55 AM ET intraday $77,288.79. https://finance.yahoo.com/personal-finance/investing/article/bitcoin-and-ethereum-prices-today-friday-may-22-2026-prices-moved-little-this-week-120513396.html

[25] U.S. Securities and Exchange Commission, "Strategy Inc 8-K filing," May 18, 2026. 24,869 BTC purchase for $2.01B, average $80,985; total holdings 843,738 BTC at average $75,700. https://www.sec.gov/Archives/edgar/data/0001050446/000119312526227918/mstr-20260504.htm

[26] Cryptonews, "TD Cowen raises Strategy price target to $400, citing faster bitcoin accumulation and accretive deleveraging," https://cryptonews.net/news/finance/32885153/

[27] Yahoo Finance MSTR 5/22 close $159.89 (–3.01% daily); Morningstar MSTR 5/15 close $177.42 。 https://finance.yahoo.com/quote/MSTR/history/ + https://www.morningstar.com/stocks/xnas/mstr/quote

[28] Yahoo Finance, "Strategy Inc (MSTR) summary commentary," May 22, 2026. https://finance.yahoo.com/quote/MSTR/

[29] Crypto Briefing, "21Shares' Hyperliquid ETF hits $37.2M AUM in first week," May 21, 2026. Cumulative net inflows $24.4M. https://cryptobriefing.com/21shares-hyperliquid-etf-37m-aum/

[30] Loris Tools, "HIP-3 Data & Analytics—Hyperliquid Builder DEX Stats," accessed May 22, 2026. Mid-week OI ~$2.56B. https://loris.tools/hip3

[31] Bitget News, "Trade.xyz Dominates the Hyperliquid Ecosystem, Holding Over 90% Market Share of HIP-3," May 2026. ~93.7% HIP-3 share. https://www.bitget.com/news/detail/12560605309092

[32] CME Group, "CME Group to Launch 24/7 Cryptocurrency Futures and Options Trading on May 29," official press release, February 19, 2026. Trading begins Friday May 29, 2026 at 4:00 PM Central Time on CME Globex, with a two-hour weekly maintenance window over weekends; pending regulatory review. https://www.cmegroup.com/media-room/press-releases/2026/2/19/cme\_group\_to\_launch247cryptocurrencyfuturesandoptionstradingonma.html

[33] ODaily, "Trade.xyz 220 days after its launch, Hyperliquid is becoming the 'New Nasdaq,'" May 2026. Hyperliquid network-aggregate RWA OI ~$2.6B mid-month; tokenized-stock turnover cumulative peak ~$3.57B. https://www.odaily.news/en/post/5210888

[34] Trading Economics, "Brent crude oil price chart," accessed May 25, 2026. May 22 ~$105; WTI ~$97; weekly –4 to –6%. https://tradingeconomics.com/commodity/brent-crude-oil

[35] 24/7 Wall St, "SPR weekly drain May 16: largest ever weekly amount, almost 10 million barrels," May 20, 2026. Citing EIA Weekly Petroleum Status Report. Total reserves now below 375 million barrels. https://247wallst.com/investing/2026/05/20/trump-promised-to-refill-americas-emergency-oil-reserve-instead-it-just-saw-its-largest-weekly-drain-in-history/

[36] Bitrue, "Stablecoin Trends May 2026: USDT vs USDC, Market Cap & GENIUS Act Explained," May 2026. GENIUS Act July 18, 2026 compliance trigger. https://www.bitrue.com/blog/stablecoin-trend-may-2026

[37] Bitbase Research, "When Momentum Breaks: A Structural Framework for Reading Meme Markets" (Deep Dive 4), May 22, 2026. Chapter 7 reverse-signal enumeration.

[38] Investment Company Institute, "Money Market Fund Assets," May 21, 2026 release covering week ended May 20. Total MMF assets $7.77 trillion; weekly change +$16.88B (government +$16.34B, prime +$946M, tax-exempt –$409M); retail +$4.04B to $3.09T. https://www.ici.org/research/stats/mmf