Publication date: April 24, 2026

Executive Summary

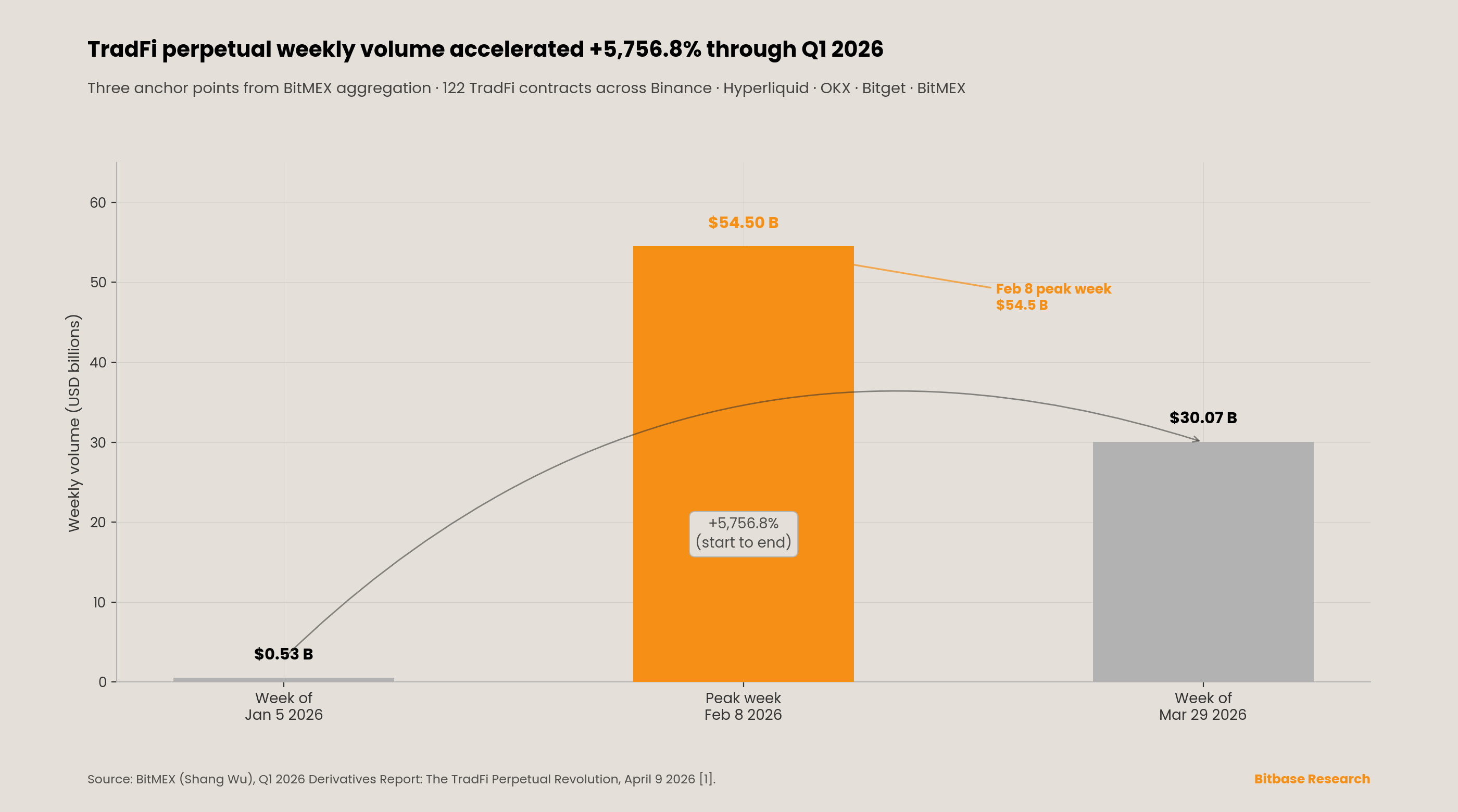

Crypto exchange expansion into traditional-finance asset classes accelerated materially between October 2025 and April 2026. BitMEX's Q1 2026 Derivatives Report—a venue-aggregated analysis authored by a TradFi-perpetual market participant—found that weekly TradFi-perpetual volume grew from $525.8 million at the start of Q1 2026 to $30.7 billion, a growth rate the report calculates at +5,756.8% [1]. The commodity sub-segment grew from $38.1 million to $25.0 billion per week (+65,463%), with a peak single-week volume of $54.5 billion in the week of February 8, 2026 [1]. These figures originate from BitMEX's internal aggregation across Binance, Hyperliquid, OKX, Bitget, and BitMEX APIs covering 122 TradFi perpetual contracts; no independent replication by Kaiko, CCData, Coin Metrics, or Messari has been located as of the publication date of this report.

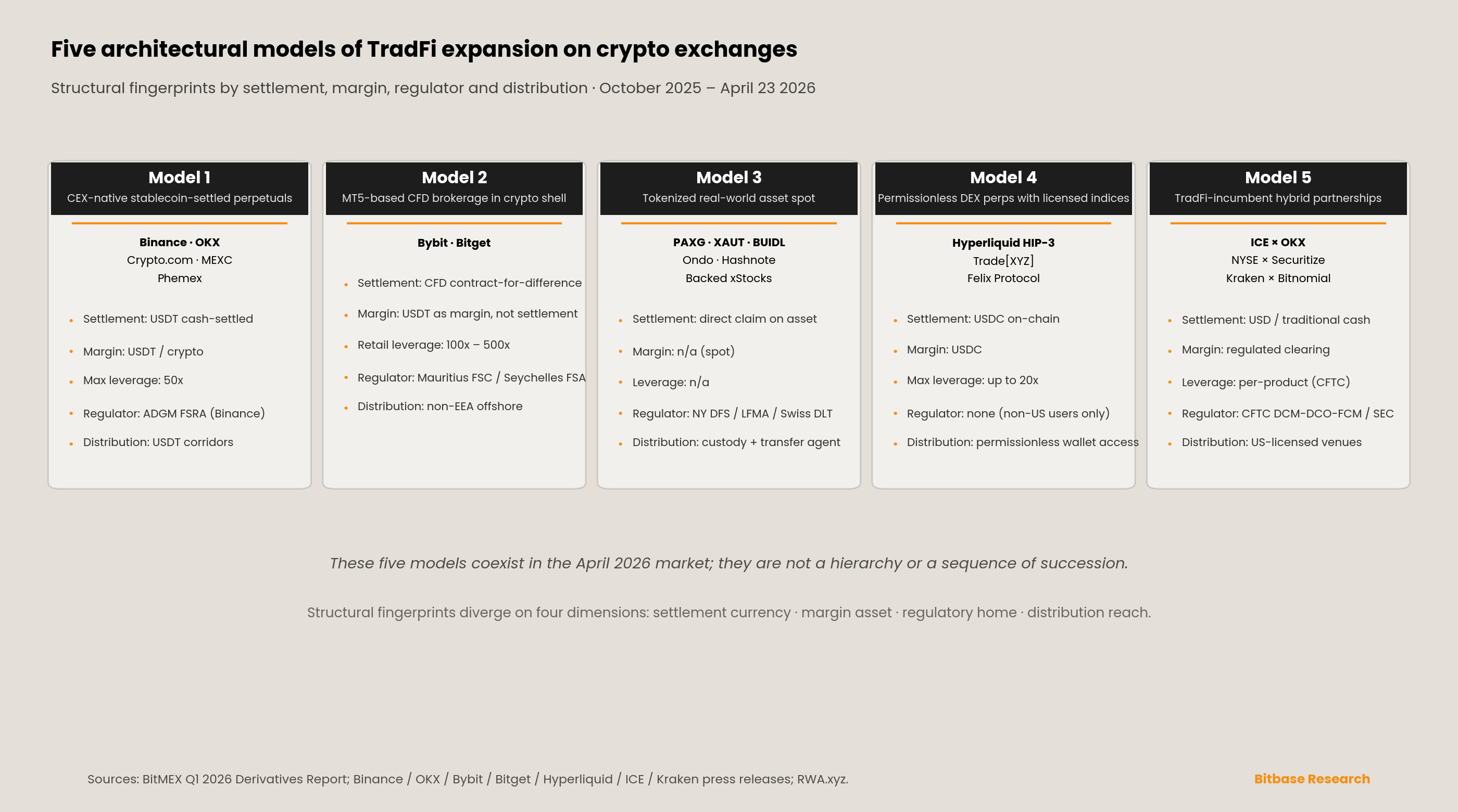

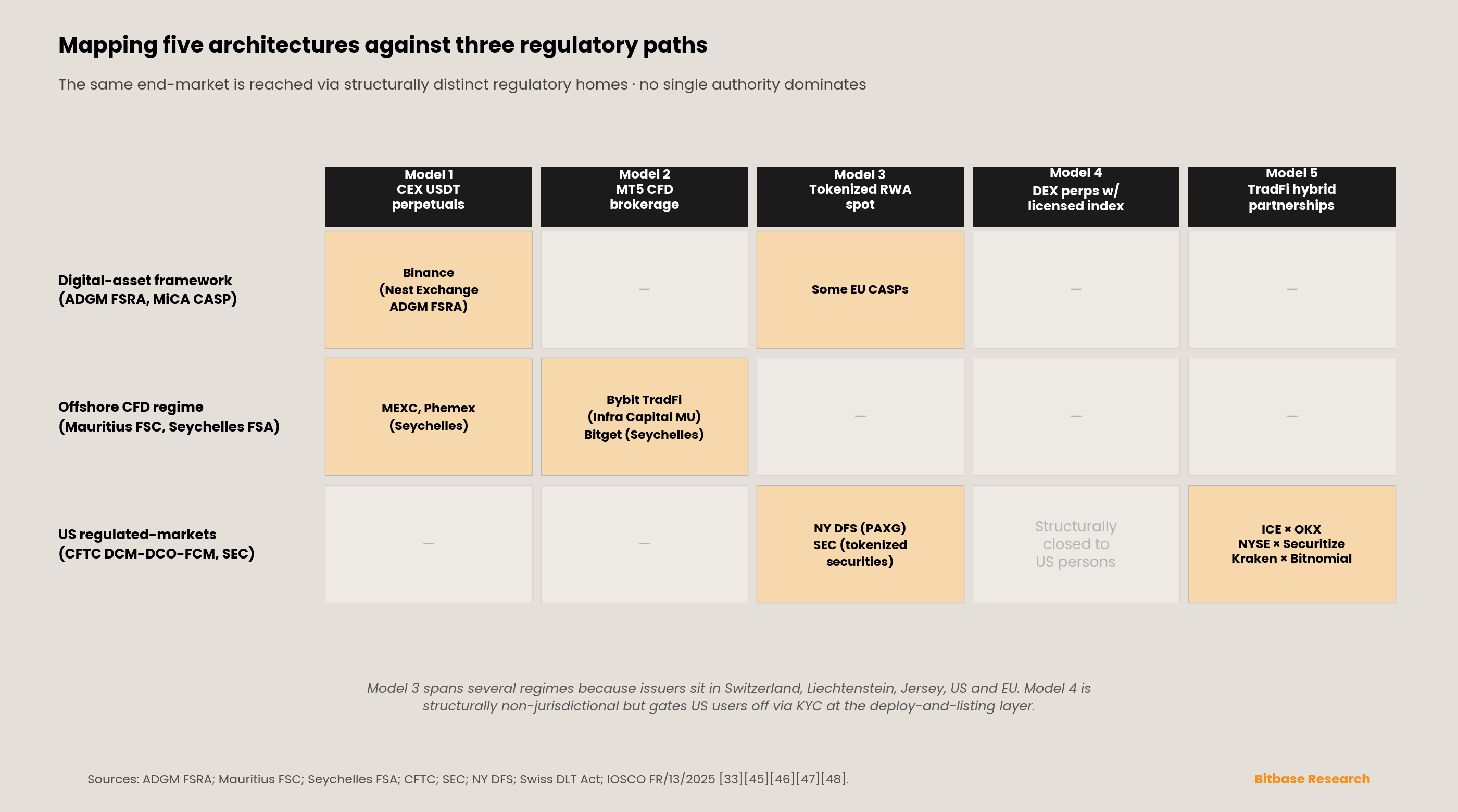

The observation this report develops is that the aggregate growth figure obscures a more consequential structural fact: the underlying architecture did not converge on a single path. Over the six-month window, crypto-exchange TradFi products fractured into five architecturally distinct models, each anchored to a different regulator, a different collateral standard, and a different class of end-user. We refer to them throughout the report as Models 1 through 5 and summarize them here.

Model 1 is the CEX-native stablecoin-settled perpetual. On January 5, 2026, Binance, through its ADGM-licensed entity Nest Exchange Limited, listed XAUUSDT (gold) and two days later XAGUSDT (silver) as cash-settled USDT-denominated perpetual contracts under the FSRA framework [2]. OKX, Phemex, MEXC, and Crypto.com published subsequent versions of the same template during Q1 2026. The architectural fingerprint is: stablecoin collateral, stablecoin settlement, no expiry, leverage up to 50×, no underlying-asset redemption, venue regulated inside a digital-asset framework rather than under a CFD regime.

Model 2 is the MT5-based CFD brokerage operating inside a crypto-wallet interface. Bybit TradFi, launched in April 2025 and formalized via its June 17, 2025 announcement, is powered by Infra Capital (Mauritius FSC licensed) and offered 78 stock CFDs plus commodities, indices, and FX on a single daily-volume peak of $24 billion on April 17, 2025 [3]. Bitget TradFi followed with a public launch on January 5, 2026 [4]. The architectural fingerprint is: MT5 or equivalent CFD engine, offshore (Mauritius / Seychelles) licensing, retail leverage in the 100×–500× range, USDT used as margin rather than as contract settlement, client-creditor rather than client-beneficiary asset structure.

Model 3 is tokenized real-world-asset spot. PAXG, XAUT, BlackRock BUIDL, Ondo OUSG and USDY, Franklin Templeton BENJI, Hashnote USYC (acquired by Circle), Superstate USTB, and Backed Finance xStocks together constitute a category in which the on-chain token is a direct claim on an off-chain asset custodied by a regulated trustee and attested by an independent auditor [5][6]. By the April 2026 RWA.xyz snapshot used for this report, tokenized U.S. Treasuries totaled $13.4 billion and tokenized commodities $7.37 billion, with XAUT and PAXG together representing approximately 74% of the commodity sub-category [5].

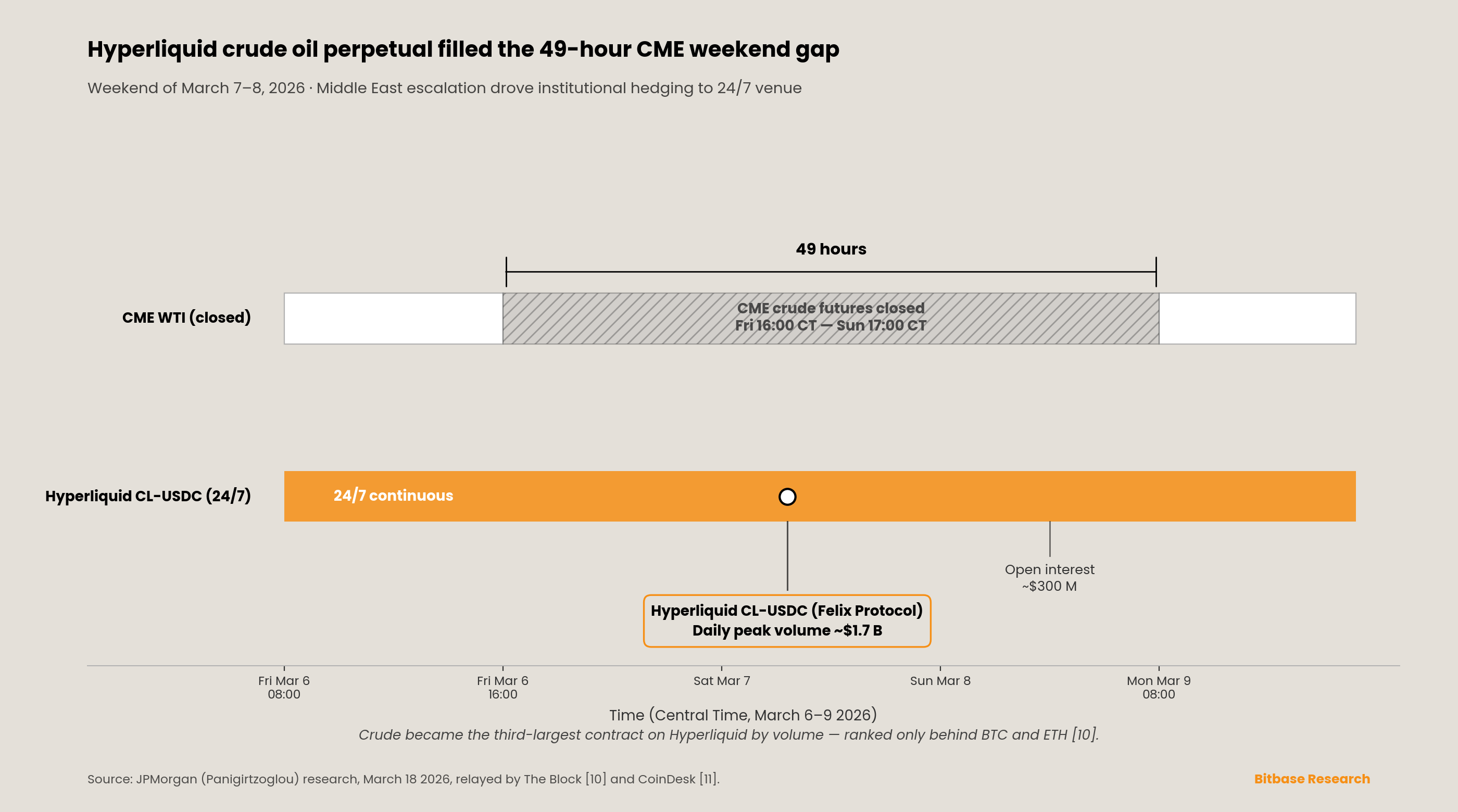

Model 4 is the permissionless DEX perpetual with a licensed index overlay. Hyperliquid activated HIP-3 on mainnet on October 13, 2025, allowing any party that stakes 500,000 HYPE to deploy a perpetual market with custom oracle, leverage, and settlement logic [7][8]. On March 18, 2026, S&P Dow Jones Indices announced it had licensed the S&P 500® to Trade[XYZ] to launch what SPDJI described as "the first and only officially licensed perpetual derivative contract based on The 500®" on Hyperliquid [9]. A JPMorgan note published the same day, led by Managing Director Nikolaos Panigirtzoglou and reported by The Block and CoinDesk on March 18–20, 2026, found that the Crude Oil (WTI) perpetual deployed under HIP-3 by Felix Protocol peaked at approximately $1.7 billion in daily volume with roughly $300 million in open interest during the Middle-East-escalation weekend of March 7–8, 2026 [10][11]. JPMorgan's note ranked oil as Hyperliquid's third-most-traded product behind BTC and ETH [10]. The architectural fingerprint is: public-chain settlement, USDC collateral, licensed benchmark overlay, non-U.S.-only distribution under current CFTC perimeter.

Model 5 is the TradFi-native hybrid partnership. Intercontinental Exchange announced a strategic investment in OKX on March 5, 2026 at a $25 billion valuation, reported by Bloomberg at approximately $200 million, with a board seat, licensing of OKX's spot crypto price feeds into new U.S.-regulated futures at ICE Futures U.S., and reciprocal distribution of ICE's futures and NYSE tokenized equities to OKX's 120 million global accounts subject to regulatory approval [12][13]. The model is mirrored by several additional transactions. NYSE announced its tokenized-securities platform with BNY and Citi on January 19, 2026 [14]. The March 24, 2026 NYSE–Securitize memorandum of understanding named Securitize as the first digital transfer agent eligible to mint blockchain-native securities on the platform [15]. On April 17, 2026, the SEC posted notice of filing and immediate effectiveness of NYSE Rule 7.50 enabling tokenized-securities trading during the pendency of DTC's tokenization pilot [16]. And Kraken announced its agreement to acquire Bitnomial on April 17, 2026 for up to $550 million in cash and stock [17]. The architectural fingerprint is: incumbent exchange capital plus crypto-native venue technology, U.S. regulatory perimeter, onshore product launches under existing DCM, DCO, and ATS frameworks.

Five regulators, five architectures, five collateral standards, five retail-protection regimes. This report develops each model in turn, examines retail usage patterns, documents the data-infrastructure limits of the period, surveys the regulatory topology, identifies three reverse signals that would falsify the five-model thesis, and closes with a discussion of why coexistence rather than convergence remains the structural expectation on an 18-to-36-month horizon.

Chapter 1 · Stablecoin-Settled Perpetuals on Centralized Exchanges

Binance's January 2026 launch set the template for Model 1. The January 8, 2026 PR Newswire release, datelined Abu Dhabi, announced what Binance described as "the first regulated TradFi perpetual contracts settled in stablecoin" [2]. XAUUSDT went live on January 5, 2026 and XAGUSDT on January 7, 2026. Binance chose the ADGM Financial Services Regulatory Authority as the home regulator rather than an offshore jurisdiction, a meaningful choice given that FSRA requires Recognized Investment Exchange status and capital-adequacy disclosures considerably above offshore norms. Jeff Li, Binance VP Product, described the launch as "a key step in bridging traditional finance and crypto innovation" [2]. The January 8 PR confirms the ±3% off-hours deviation band and the EWMA-smoothed mark-price methodology engineered specifically for the gap between continuous crypto markets with native oracle price discovery and gold markets with weekend closures and exchange-published fixings. Leverage levels up to 50× and the ten-plus subsequent contract expansions (XPT, XPD, COPPER, TSLA, INTC, HOOD, MSTR, AMZN, CRCL, COIN, PLTR) are not enumerated in the January 8 release itself but are documented in BitMEX's Q1 2026 Derivatives Report and Binance Futures product data [1].

OKX followed on March 24, 2026 with an equity-perpetuals suite covering the Magnificent Seven (NVDA, TSLA, AAPL, GOOGL, MSFT, AMZN, META), crypto-adjacent names (MSTR, COIN, HOOD, CRCL), plus PLTR, INTC, MU, SNDK, and SPY, at up to 5× leverage, USDT-denominated, accepting BTC, ETH, USDT, and OKX Auto Earn–yielding assets as collateral—a capital-efficiency feature that CFD brokerage rails cannot replicate [18][19]. OKX Founder and CEO Star Xu framed the launch as "an important step toward bringing a broader range of real-world assets onto our platform" [18]. Distribution is explicitly non-U.S.: Asia, the Commonwealth of Independent States, Latin America, and Türkiye. The launch followed the ICE investment in OKX by precisely 19 days.

Crypto.com added commodity and U.S. index perpetual contracts on April 1, 2026, covering gold, oil, and major U.S. indices, with retail users restricted to isolated margin and non-retail users able to toggle between isolated and cross [20]. MEXC's self-published Q1 2026 TradFi report claims +246% quarter-over-quarter TradFi-futures volume growth, expansion from 71 instruments in January to 115 in March, and top-of-book depth leadership in gold across seven major platforms [21]. Each of those MEXC figures is entirely self-disclosed, based on a snapshot methodology dated March 23, 2026, and unaudited by any independent third party; they are directionally consistent with BitMEX's aggregated finding [1] but the specific market-share claims should not be cited without the self-disclosure caveat. Phemex disclosed WTI and Brent volumes rising roughly +300% week-over-week in the week ending April 9, 2026, during the Middle-East-ceasefire volatility episode [22]; the same self-disclosure caveat applies.

The structural feature of Model 1 is that the stablecoin is the settlement currency, not merely the margin currency. A trader in XAUUSDT never posts dollars and never receives physical gold; the trader posts USDT, receives USDT, and the contract's payoff is a USDT delta indexed to a gold reference price. ESMA's March 19, 2025 guidelines qualify perpetual contracts as derivative financial instruments under MiFID II Annex I Section C when the underlying is a listed commodity or security [23]. Combined with ESMA's public position that USDT does not meet MiCA-compliant e-money token requirements, the effect is that Model 1 is structurally foreclosed to EU retail distribution by authorized CASPs. The architecture thrives in the corridors where USDT circulates freely—MENA, the CIS region, Latin America, Türkiye, and Southeast Asia—and where MiCA does not reach.

Two structural limitations of Model 1 warrant explicit discussion. First, USDT settlement introduces a single-currency credit exposure that is absent from cleared-futures alternatives. A XAUUSDT trader's payoff is conditioned on both the gold price and the solvency of Tether Holdings Limited as the issuer; a CME COMEX gold futures position, by contrast, is backstopped by CME Clearing's central-counterparty guarantee. The two products are not risk-equivalent, and that difference becomes material under tail scenarios. Second, stablecoin-settled perpetuals on centralized venues are not yet eligible collateral under the U.S. CFTC's December 8, 2025 Digital Assets Pilot, which authorized "Bitcoin, Ether, and eligible payment stablecoins" as collateral at regulated derivatives firms; USDT does not currently qualify as an eligible payment stablecoin under the relevant Staff Letter 25-40 criteria [24]. The practical consequence is that Model 1 cannot at present interoperate with U.S. FCM margin frameworks, and any convergence of Model 1 with Model 5 would require either a change in U.S. stablecoin eligibility rules or a re-issuance of Model 1 products in USDC, which would re-configure the product's economics.

Chapter 2 · The MT5 CFD Shell

Bybit's claim to have been the first major crypto exchange to launch a TradFi product in 2022 requires correction, and the correction matters for the broader taxonomy. No Bybit CFD, commodity, FX, or equity-index launch occurred in 2022. The earliest 2022 Bybit product innovation identified via primary-source search is its USDC-margined Bitcoin options launch, described in a contemporaneous Bybit–Circle partnership announcement as "the first stablecoin-margined option contract in the market"—a crypto derivative with a stablecoin collateral innovation, not a TradFi product. The actual Bybit MT5 TradFi launch occurred in April 2025. Bybit's June 17, 2025 PR Newswire announcement, "Introducing Bybit TradFi: Trading the World on Bybit," states verbatim that the offering "evolved from Bybit's popular Gold & FX service, which recorded its highest daily trading volume of over $24 billion on 17 April, 2025," and that "Bybit TradFi is powered by Infra Capital (Mauritius FSC licensed)," with "78 leading stock CFDs via Bybit, including FAANG stocks" [3]. On January 29, 2026, Bybit CEO Ben Zhou's keynote "BUIDLing a New Financial Era" declared that Bybit TradFi integrated more than 200 TradFi instruments with a stated plan to launch 500 trading pairs in Q1 2026, alongside MyBank (multi-currency IBAN retail banking) and ByCustody (institutional custody above $5 billion in reported AUM) [25].

Bitget's version launched on January 5, 2026 after a December 2025 private beta with over 80,000 users reportedly waitlisted. Bitget's own January 2026 Transparency Report disclosed TradFi daily volume reaching approximately $4 billion within weeks of public launch, with three instrument types on the platform—MT5 CFDs, stock perpetual contracts, and Ondo-issued tokenized equities—operated under a Seychelles entity [4]. Those Bitget figures are self-disclosed and not independently audited.

The regulatory substrate of Model 2 warrants attention because it explains the economics. Mauritius's Investment Dealer (Full Service Dealer, excluding Underwriting) Licence under the Securities Act 2005 and the Securities (Licensing) Rules 2007 requires a minimum unimpaired capital of MUR 1,000,000 (approximately USD 25,000), together with two resident directors, an MLRO, and GBC status under the Financial Services Act 2007. The Mauritius Broker sub-category requires only MUR 700,000; the Full Service dealer license that includes underwriting requires MUR 10 million; the Full-Service-excluding-underwriting tier is the middle path widely used by offshore CFD brokerages. Crucially, none of these sub-tiers impose an ESMA-style retail leverage cap. Seychelles's Securities Dealer Licence under the Securities Act 2007 is similar: minimum paid-up capital USD 100,000 (raised from USD 50,000 in amendments effective January 1, 2025), with perpetual licensing introduced in 2025 (an annual USD 6,000 fee remains payable), and again no retail leverage caps. Mandatory negative-balance protection is not a Seychelles licensing condition.

Both regimes stand in direct structural contrast to ESMA Decision 2018/796. The Decision was adopted on May 22, 2018, published in the Official Journal on June 1, 2018, and applied from August 1, 2018 for CFDs. It imposed the retail-CFD cap matrix that has since defined EU retail derivatives regulation: 30:1 for major currency pairs; 20:1 for non-major currency pairs, gold, and major equity indices; 10:1 for commodities other than gold and non-major equity indices; 5:1 for individual equities and other reference values; and 2:1 for cryptocurrencies [26]. ESMA's March 27, 2018 press release disclosed that across National Competent Authority analyses, "74–89% of retail accounts typically lose money on their investments, with average losses per client ranging from €1,600 to €29,000" [26]. The Central Bank of Ireland's 2015 thematic inspection had found 75% of Irish retail CFD clients lost money, with average losses of €6,900. The FCA's Policy Statement PS19/18, confirmed July 1, 2019 and applied August 1, 2019 for CFDs and September 1, 2019 for CFD-like options including turbo certificates and knock-outs, converted ESMA's temporary caps into permanent UK rules and, per the FCA, was "expected to save retail consumers between £267 million and £451 million per year" [27].

The Bybit and Bitget TradFi stacks are architecturally identical to the pre-2018 offshore CFD industry—MT5 engine, wide leverage ranges, a client-creditor asset structure, and retail-loss dynamics—distinguishable primarily by the wallet integration, the USDT margin rail, and the crypto-native user acquisition flywheel. The primary regulatory exposure of the model sits not in the crypto layer but in the CFD layer, where MiFID II and its analogues in the UK, Australia, Singapore, and Japan have built a decade of disclosure, leverage, and negative-balance-protection requirements that Mauritius and Seychelles have not adopted. The model's viability rests on regulatory-arbitrage economics rather than technology, and that anchoring determines both its distribution geography and its pricing power.

Two points of neutrality should be stated alongside the regulatory critique, because they describe the model's legitimate trader-value proposition. First, the MT5 engine is familiar to a large professional CFD trader population and carries a two-decade execution pedigree; the technology stack is mature, not experimental. Second, the stablecoin-margined, single-account structure that Bybit and Bitget offer—one USDT balance across crypto perpetuals, stock CFDs, commodity CFDs, and FX—produces a unified margin efficiency that CFD brokers working inside traditional broker-dealer architectures typically cannot match. For traders whose primary exposure is cross-asset and whose primary need is consolidated collateral, Model 2 offers a product the regulated EU/UK CFD market deliberately does not.

Chapter 3 · Tokenized Real-World-Asset Spot

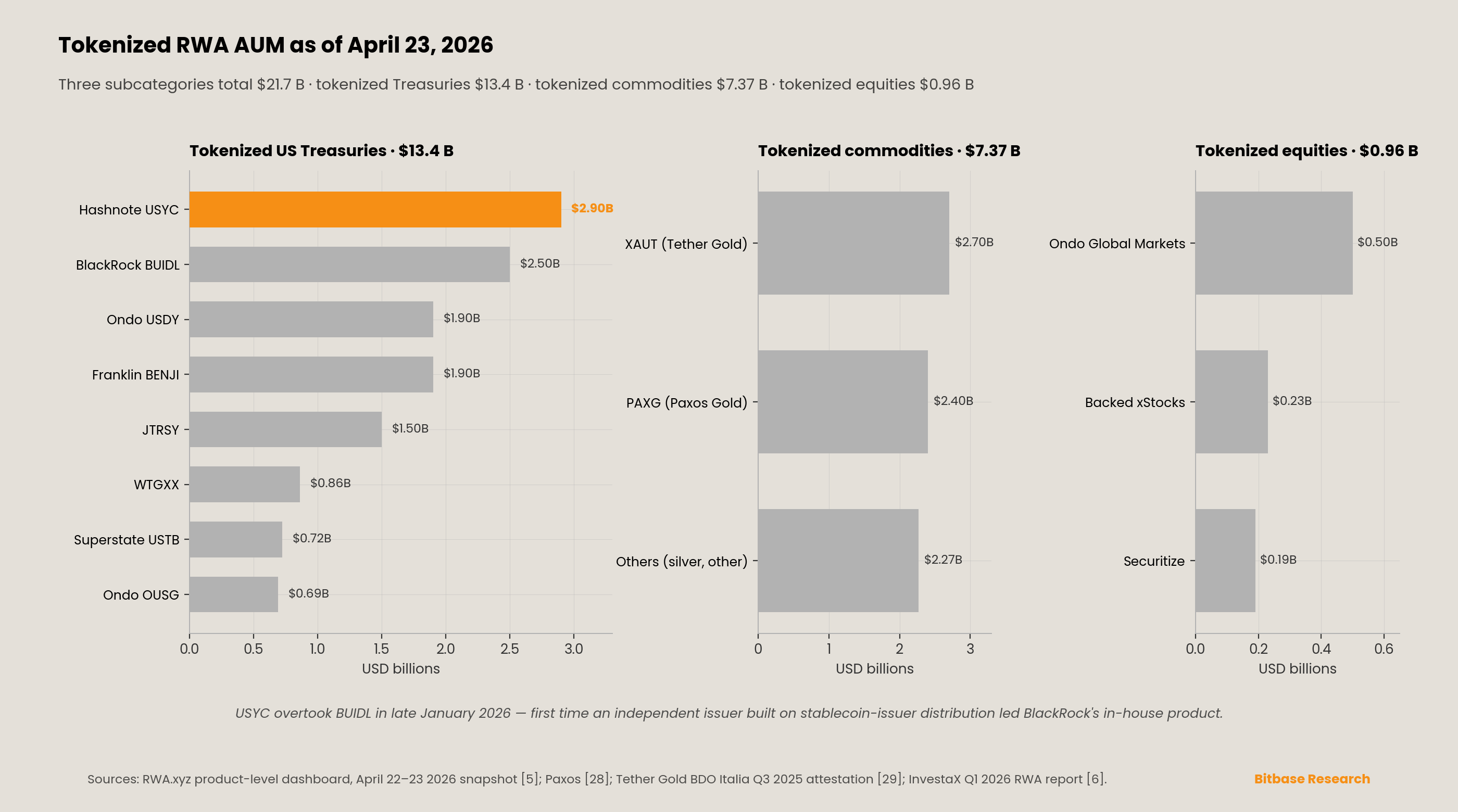

The RWA spot layer grew from roughly $21 billion at the start of 2026 to $27.5 billion by the end of Q1 2026, approximately +30% in a single quarter, according to Q1 2026 RWA.xyz-sourced aggregations [5][6]. Growth is concentrated in two sub-segments.

Tokenized U.S. Treasuries reached $13.4 billion by April 23, 2026, up from $9.6 billion at year-end 2025. The $10 billion milestone was crossed on January 22, 2026, with RWA.xyz-sourced reporting documenting the crossing on January 22–23, 2026 (some secondary summaries incorrectly placed the crossing in February). The April 2026 product-level live leaderboard on RWA.xyz, as of April 23, 2026, reads as follows: Hashnote USYC at $2.9 billion (having sustained its flip above BlackRock BUIDL on January 21–22, 2026), BlackRock BUIDL at $2.5 billion, Ondo USDY at $1.9 billion, Franklin Templeton BENJI at $1.9 billion, Superstate USTB at $725 million, and Ondo OUSG at $691 million. JTRSY at $1.5 billion and WTGXX at $862 million also sit in the top tier [5]. The USYC-over-BUIDL rotation is a notable positional shift in the Treasury tokenization market, representing the first sustained period during which an independent issuer built on top of a major stablecoin issuer's distribution has outscaled BlackRock's direct offering.

Tokenized commodities reached a category total of $7.37 billion by April 2026, dominated by gold. Paxos Gold (PAXG) stands at approximately $2.4 billion market capitalization, with physical London Good Delivery gold custodied in Brink's London LBMA-accredited vaults. Paxos replaced WithumSmith+Brown, PC with KPMG LLP as the PAXG attestation provider effective February 28, 2025, pursuant to NYDFS Dollar-Backed Stablecoin guidance [28]. Tether Gold (XAUT) reached approximately $2.7 billion market capitalization by April 2026. The latest XAUT attestation published as of April 23, 2026 is the Q3 2025 BDO Italia ISAE 3000R reasonable-assurance report dated September 30, 2025 (released October 28, 2025), confirming 375,572.297 fine troy ounces of allocated gold valued at approximately $1.449 billion at the reporting-date price [29]. (Tether's first XAUT-specific attestation, for Q1 2025, was published April 28, 2025 and documented 246,523.33 fine troy ounces at $3,123.57/oz for an aggregate market value of approximately $770 million [29].) XAUT and PAXG together represent approximately 74% of the tokenized-commodity category.

Tokenized equities sit at approximately $960 million as of March 2026, up from roughly $424 million as of mid-year 2025 (June 30, 2025 RWA.xyz snapshot). Ondo Global Markets holds roughly 52% category share, Backed Finance (the xStocks issuer) approximately 24%, and Securitize approximately 20%. Backed Finance's architecture is worth understanding in detail because it is the substrate beneath Kraken's February 24, 2026 tokenized-equity perpetuals launch. xStocks tokens are issued by Backed Assets (JE) Limited, a Jersey special-purpose vehicle wholly owned by Backed Finance AG in Zug, Switzerland. The base prospectus is approved by the Liechtenstein Financial Market Authority (FMA) under the EU Prospectus Regulation, giving EEA passporting. Each xStock is legally a tracker certificate—a bearer debt instrument backed 1:1 by the underlying security held by regulated custodian banks in Switzerland and the United States, with redemption for cash value rather than for the underlying share. Token holders are secured creditors, not direct equity owners; a Swiss Security Agent protects holders in a default scenario under the Swiss DLT Act. U.S. persons and UK retail investors are excluded from primary issuance.

Kraken (Payward) announced the acquisition of Backed Finance AG on December 2, 2025, vertically integrating the issuer into its derivatives stack [30]. The acquisition was a full-company transaction; financial consideration was not disclosed. The February 24, 2026 Kraken launch of the "world's first regulated, tokenized-equity perpetual futures, using xStocks" was therefore a first-party product rather than a licensing relationship [31]. The launch is operated through Payward Digital Solutions Ltd. (PDSL), licensed by the Bermuda Monetary Authority, with 20× leverage and an initial ten-ticker roster: SPYx, QQQx, GLDx, AAPLx, NVDAx, GOOGLx, TSLAx, HOODx, MSTRx, and CRCLx, available in 110-plus countries excluding the United States and UK retail [31].

The Bitget–Ondo partnership (announced July 17, 2025, live September 3, 2025, and expanded on January 9, 2026 with 98 additional U.S. stocks and ETFs) is notable because Bitget self-reported $15 billion in tokenized-stock volume during 2025 and an 89% share of tokenized-stock trading in December 2025. RWA.xyz does not publish per-exchange volume breakdowns, so those Bitget figures remain self-disclosed and unaudited; the directional rise of Ondo Global Markets to the top of the tokenized-equity category is consistent with them. The Bitget–Ondo arrangement is centered on Ondo Global Markets tokenized equities, ETFs, and money-market funds rather than on OUSG or USDY specifically.

The governance structure of Model 3 is what separates it from Models 1 and 2. A PAXG holder has a legal claim on an allocated ounce of gold custodied by a regulated trustee. A USDT-settled gold perpetual trader has a contractual USDT payoff conditioned on the stablecoin issuer's solvency. An MT5 gold CFD trader has a client-creditor claim against the broker's balance sheet, typically domiciled in Mauritius or Seychelles. The attestation cadence, custody standard, and redemption right differ categorically across these three layers, and so does the bankruptcy waterfall. Treating "gold exposure on a crypto exchange" as a single product category misses the regulatory and credit structure that will ultimately determine which layer absorbs the next market-stress event without loss to end-users.

Chapter 4 · Permissionless DEX Perpetuals with Licensed Benchmark Overlays

HIP-3 is the consequential DeFi infrastructure shift of the research period. Hyperliquid's official documentation describes it as "builder-deployed perpetuals" and "a key milestone toward fully decentralizing the perp listing process" [7]. The mainnet activation date of October 13, 2025 is cross-confirmed by the CoinDesk activation report, Hyperliquid's own community posts, and independent trackers at CoinGecko and FalconX [8]. The economic controls deserve precise citation: the staking requirement for mainnet is 500,000 HYPE, held for a minimum 30-day post-halt window during which the deployer's stake remains slashable by stake-weighted validator vote. The first three assets a deployer lists bypass auction; additional assets go through a Dutch auction using HIP-1 hyperparameters. Fee split between deployer and protocol is 50/50 on base tiers of approximately 3 basis points maker and 9 basis points taker, before discounts.

HIP-3's output in six months is material. Per CoinGecko's Q1 2026 estimate, HIP-3 markets had grown to represent over 35% of all Hyperliquid trading volume. Two deployments define the category.

Felix Protocol's Crude Oil WTI perpetual, settled in USDC, was deployed under HIP-3 on January 9, 2026 at 09:47 UTC. Felix's own launch post documents the starting parameters: "Starting max leverage is 5x" and "Starting OI cap is set at 2.5M USD" [32]. Leverage was raised to 20× over the first quarter of operations. JPMorgan's research note, published on March 18, 2026 and led by Managing Director Nikolaos Panigirtzoglou, as reported by The Block and CoinDesk on March 18–20, 2026, found that daily trading volume in the Crude Oil perpetual peaked at approximately $1.7 billion with open interest rising to roughly $300 million, making oil the third-most-traded product on Hyperliquid behind BTC and ETH [10][11]. The peak coincided with the weekend of March 7–8, 2026, during which CME crude futures closed on Friday at 4:00 p.m. Central Time and did not reopen until Sunday at 5:00 p.m. Central Time—a 49-hour window during which the only deep, liquid venue accepting global crude flow was Hyperliquid's CL-USDC market. The CoinDesk report quotes Panigirtzoglou directly: "Oil trading exploded on the Hyperliquid exchange early this month when the Iran war erupted as CME traders were unable to react when Iranian infrastructure strikes broke over the weekend" [11].

Trade[XYZ]'s S&P 500 perpetual is the second pillar. The joint S&P Dow Jones Indices and Trade[XYZ] press release datelined New York on March 18, 2026 is the authoritative primary source and opens with the following verbatim formulation: "S&P Dow Jones Indices ('S&P DJI'), the world's leading index provider, announced today that it has licensed the S&P 500® to Trade[XYZ] ('XYZ') to launch the first and only officially licensed perpetual derivative contract based on The 500®" [9]. SPDJI Chief Product & Operations Officer Cameron Drinkwater is quoted: "This collaboration expands access and utility of our flagship benchmarks within digital trading environments" [9]. Collins Belton, identified in the release as Chief Operating Officer and General Counsel of Trade[XYZ]'s parent company, is quoted describing the S&P 500 as "a natural starting point" [9]. The release discloses that "since October 2025, XYZ markets have exceeded $100B in volume with a current annualized run rate in excess of $600B" [9]. Those two figures are self-disclosed by Trade[XYZ] within the joint release; Hyperliquid's stats endpoint is a self-published aggregator; DefiLlama segments by chain rather than by HIP-3 deployer; no independent aggregator such as Kaiko or The Block Research has yet published a cumulative Trade[XYZ]–specific figure. The directional scale is consistent with BitMEX's independent finding that Hyperliquid grew +953.4% in Q1 2026 and reached 29.7% TradFi-perpetual market share [1], but the specific $100 billion cumulative and $600 billion annualized figures originate in the Trade[XYZ] marketing release.

The regulatory exposure of Model 4 is structurally distinctive. BitMEX's Q1 2026 report observes that Hyperliquid's index partnership with S&P has attracted U.S. CFTC attention [1]. The Trade[XYZ]–SPDJI release is explicit that access is restricted to "eligible, non-US investors" [9]. But on January 29, 2026, three weeks before Model 1's Kraken launch and less than two months before the Trade[XYZ]–SPDJI announcement, CFTC Chairman Michael S. Selig delivered his "Next Phase of Project Crypto" speech at the joint CFTC-SEC Harmonization Event. Selig had been sworn in on December 22, 2025 as the 16th CFTC Chairman after Brian Quintenz withdrew his nomination [34]. In the January 29 speech, Selig stated verbatim: "And—under my leadership—the CFTC will use the tools at its disposal to onshore perpetual and other novel derivative products so that they can flourish across both centralized and decentralized markets, subject to appropriate safeguards" [33]. The inclusion of "decentralized markets" in a sitting CFTC chairman's prepared remarks is a shift in U.S. regulatory posture that establishes the runway under which Model 4's U.S. exclusion could eventually narrow, though the path and timing remain subject to rulemaking, staff guidance, and individual enforcement decisions that have not yet been announced.

Chapter 5 · TradFi-Native Hybrid Partnerships

The fifth model is the one many market observers underestimated through 2024 and 2025: regulated incumbents buying their way into crypto rails rather than being disrupted by them. Historical perspective helps situate the development. The New York Stock Exchange traces its origins to the 1792 Buttonwood Agreement; Intercontinental Exchange was founded in 2000 and acquired NYSE in 2013; the Chicago Mercantile Exchange's lineage runs back to the 1848 Chicago Board of Trade. These institutions have absorbed technology waves from the ticker tape in 1867 to electronic matching in the 1990s to algorithmic and co-located trading in the 2000s. Each wave produced a round of "incumbent disruption" forecasts, and each time the incumbents ended the wave larger than they began it—through a mix of acquisition, regulatory inheritance, and clearing-layer control. The 2025–2026 crypto expansion is unfolding along a comparable template. This is not a claim that incumbents always win; it is an observation that a 200-year-old infrastructure layer with regulatory capital and clearing-layer control is structurally difficult to displace by technology alone. A more useful framing than "incumbent disruption" is that incumbents participate in technology transitions by buying, licensing, and clearing—rarely by building the frontier themselves—and the 2025–2026 period fits that pattern.

On March 5, 2026, Intercontinental Exchange announced a strategic investment in OKX at a $25 billion valuation, with Bloomberg reporting the commitment at approximately $200 million [12][13]. The joint release described it as a minority position "not expected to have material impact on ICE's 2026 financial results" [12]. The structure includes five elements. First, a minority equity stake. Second, a board seat on OKX's board of directors. Third, licensing of OKX's spot crypto price feeds into new U.S.-regulated futures—the release refers to "U.S.-regulated futures contracts tied to those markets"; market interpretation and subsequent CFTC filings would be expected to specify ICE Futures U.S. as the listing venue. Fourth, reciprocal access for OKX's approximately 120 million global accounts to ICE's futures and NYSE tokenized equities, subject to regulatory approval. Fifth, joint workstreams on clearing, risk, and multichain custody. ICE Chair and CEO Jeffrey C. Sprecher said: "Our strategic relationship with OKX will expand global retail access to ICE's pre-eminent regulated markets and accelerate our plans to offer on-chain infrastructure and tokenized assets to U.S. investors" [12].

The ICE–OKX transaction is distinct from ICE's separate strategic investment in Polymarket, announced October 7, 2025 and structured as an investment of up to $2 billion at an $8 billion pre-investment valuation ($9 billion post-money) [35]. Some secondary coverage has conflated the two transactions; they are separate deals, announced five months apart, with different capital commitments, different valuations, and different product scopes.

The ICE–OKX deal did not emerge in isolation. On January 19, 2026, NYSE, via ICE investor relations, announced development of "a platform for trading and on-chain settlement of tokenized securities," built in partnership with BNY and Citi on tokenized deposits, and combining "the NYSE's cutting-edge Pillar matching engine with blockchain-based post-trade systems, including the capability to support multiple chains for settlement and custody" [14]. NYSE committed to 24/7 trading of U.S. listed equities and ETFs, fractional share trading, and stablecoin-based funding. On March 24, 2026, NYSE named Securitize as the first digital transfer agent eligible to mint blockchain-native securities on the platform under a memorandum of understanding [15]. On April 17, 2026, the SEC posted notice of filing and immediate effectiveness of NYSE rule SR-NYSE-2026-17, adopting new Rule 7.50 enabling trading of securities in tokenized form during the pendency of DTC's tokenization pilot program [16]. The April 17 filing is a notice-of-immediate-effectiveness filing under Rule 19b-4(f)(6), meaning the rule took effect upon filing but remains subject to SEC suspension within 60 days; it is not a full SEC approval order, and Nasdaq had received a corresponding staff action approximately one month earlier, with DTC receiving no-action relief in December 2025.

The capstone is Kraken's April 17, 2026 agreement to acquire Bitnomial for up to $550 million in a cash-and-stock transaction that valued Payward's equity at $20 billion, giving Kraken direct ownership of a CFTC-licensed Designated Contract Market, Derivatives Clearing Organization, and Futures Commission Merchant—three licenses within a single combined entity that only a handful of regulated U.S. venues hold [17]. Bitnomial had been the first U.S. CFTC-regulated exchange to list perpetual futures, launching BTC/USD perpetuals on April 28, 2025 via self-certification under CFTC Regulation 40.2(a), with eight-hour funding-rate intervals and a 25-year nominal expiry [36][37]. Bitnomial was also the first CFTC-regulated exchange to accept Bitcoin and Ether as margin collateral in early September 2025 [38], and the first to launch a CFTC-regulated leveraged retail spot crypto exchange in the week of December 8, 2025 [39]. Coinbase Derivatives launched its own BTC and ETH "perpetual-style futures" on July 21, 2025, structured as long-dated five-year futures contracts with 24/7 trading hours, funding accrued hourly and settled twice daily, up to 10× intraday leverage for crypto and 20× for metals [40]. The CME Group, as of April 2026, has not launched a CFTC-approved perpetual contract; its 2025 and early-2026 rollouts have been confined to expiry-dated BTC, ETH, SOL, and XRP futures and options. The implication is that the perpetuals beachhead in the U.S. market has been taken by Bitnomial and Coinbase, and the $550 million price tag for Bitnomial (within a $20 billion valuation for Payward) provides the clearest market-revealed valuation of U.S. perpetuals licensing documented in the research period [17].

Model 5's structural advantage is that it offers U.S. retail and institutional access to products that Models 1, 2, and 4 cannot serve onshore. Model 1 depends on USDT, which does not currently qualify as "eligible payment stablecoin" collateral under the CFTC's December 8, 2025 Digital Assets Pilot Staff Letter 25-40 criteria [24]; Bitcoin, Ether, and USDC are the named eligible collateral types during the first three months of FCM reliance. Model 2 is an offshore CFD model that U.S. retail has been fenced out of since Dodd-Frank (2010). Model 4 is explicitly non-U.S. and survives only so long as HIP-3's geographic restrictions and the CFTC's enforcement posture remain as they stand on the publication date of this report. Model 3 is jurisdiction-agnostic but offers only spot exposure, not leveraged trading. Only Model 5 can at present serve leveraged TradFi-adjacent exposure to U.S. retail under the existing CFTC regime. The ICE and Kraken transactions carry the capital weights they do because that asymmetry is pricing through.

Chapter 6 · Who Uses These Products: Retail and Institutional Segmentation

The five architectural models serve overlapping but non-identical user populations, and the primary-source broker data makes the segmentation visible.

eToro priced its Nasdaq IPO at $52 on May 13, 2025, closed at $67 on its first trading day (May 14, 2025) for a first-day close valuation of approximately $5.4 billion, and disclosed in its F-1/A approximately 3.5 million funded accounts at December 31, 2024 (3.58 million at March 31, 2025) across 75 countries, against 40 million registered users [41][42]. eToro's FY2024 commission mix was crypto 38%, equities 38%, commodities 20%, and currencies 4% on total commissions of $931 million, up 45.6% year-over-year [41]. A separate metric in the F-1/A—net trading contribution share—rose from 10% in 2023 to approximately 25% in 2024 for crypto; the commission-mix share and the net-trading-contribution share are distinct ratios that should not be conflated. The structural point is that eToro is a multi-asset retail broker that added crypto, while Bybit, Bitget, and Kraken are structurally crypto exchanges that added equities and commodities. The two cohorts are converging from opposite sides of the same river.

Plus500's FY2024 Annual Report, published March 24, 2025, documents 254,138 Active Customers (up from 233,037 in FY2023) and 118,010 New Customers (up from 90,944), with total customer deposits at a record $3.0 billion and total revenue of $768.3 million (trading revenue $711.6 million plus interest income $56.7 million) [43]. Non-OTC business (share dealing, U.S. futures, and options) contributed approximately 10% of total group revenue, leaving roughly 90% from OTC CFDs. Plus500 specifically discloses that "67% of FY 2024 OTC revenue was generated by customers who have been trading with Plus500 for more than three years" [43]—a retention metric rarely reported in the crypto-exchange cohort.

IG Group's FY25 results, for the year ended May 31, 2025 and published July 24, 2025, report 820,000 active customers—a 137% increase that includes the Freetrade acquisition's 457,300 accounts, plus organic growth of approximately 5% to 362,800 active accounts in the core business. Total revenue was £1,075.9 million (up 9%), with adjusted profit before tax of £535.8 million at a 49.8% margin [44]. The business is diversified across OTC derivatives (the largest single revenue source), exchange-traded derivatives (£159.4 million, up 13%), stock trading and investments (£31.6 million, up 39%, including £3.7 million from Freetrade), and net interest income (£133.1 million, down 6%). Within the U.S. division, IG notes that "customer cash balances held off balance sheet at the end of the period were $2.0 billion (FY24: $1.9 billion). This contributed £67.7 million of interest income (FY24: £75.6 million)" [44]. The £67.7 million figure is interest income on U.S. off-balance-sheet cash, not tastytrade trading revenue.

The scale comparison across channels matters. Plus500 and IG Group together carry roughly 1.07 million active CFD customers; Bybit reports tens of millions of global users; eToro reports 40 million registered and 3.5 million funded [41][43][44]. The CFD channel is small, concentrated, and highly profitable; the crypto channel is large, dispersed, and only beginning to monetize TradFi flow.

The retail-loss data is the connective tissue that makes the five-model taxonomy matter. ESMA Decision 2018/796 disclosed that 74–89% of retail CFD accounts typically lose money, with average losses per client ranging from €1,600 to €29,000 [26]. The Central Bank of Ireland's 2015 inspection found 75% of Irish CFD retail clients lost money with an average loss of €6,900. The BIS Quarterly Review of December 2019 (Schrimpf and Sushko) documents that after the January 15, 2015 Swiss-franc shock, individual losses to banks providing prime brokerage to specialized retail FX margin brokers were in the hundreds of millions of dollars, triggering a wave of industry consolidation. BIS Working Paper 1094 (Chaboud, Rime, and Sushko, 2023) discusses the structural role of retail FX margin markets, particularly in Japan, as amplifiers of volatility through margin-call cascades. The ESMA and CBI figures are European-regulated-broker findings; the BIS research separately documents the post-2018 contraction in retail FX turnover as evidence that leverage caps bind the industry's economics.

Those 74–89% loss-rate figures apply, by original derivation, to EU-regulated CFD brokers operating under ESMA retail protections. The offshore Mauritius and Seychelles brokers that underpin Model 2 operate without the 50% margin close-out rule, without a uniform retail leverage cap, and, in Seychelles, without mandatory negative-balance protection—conditions ESMA's 2018 analysis identified as drivers of the upper end of the loss range. It is a reasonable hypothesis that the loss rate on Model 2 products falls near or above the upper bound of the ESMA range, though Mauritius and Seychelles do not publish the disclosure statistics required for independent verification. That asymmetry of disclosure is itself an institutional-relevance point of the report.

Chapter 7 · Data Infrastructure: What We Can and Cannot See

A recurring theme across this research is the gap between self-disclosed exchange metrics and independently verifiable data. The BitMEX Q1 2026 Derivatives Report, which serves as the primary aggregate source for TradFi-perpetual volume in this paper, is itself authored by a TradFi-perpetual market participant and relies on venue-API aggregation across Binance, Hyperliquid, OKX, Bitget, and BitMEX, covering 122 TradFi contracts [1]. No publication by Kaiko, Messari, CCData, Coin Metrics, or The Block Research has independently replicated the +65,463% commodity-perp or +5,756.8% TradFi-perp growth figures as of April 23, 2026. Binance Research has published directionally consistent daily-volume trajectories (reported via CoinDesk, April 11, 2026), and JPMorgan's Panigirtzoglou note corroborates Hyperliquid's specific market position [10][11]. But the quantum of Q1 2026 growth rests on BitMEX as originator.

MEXC's Q1 2026 TradFi Report (April 22, 2026) is a notably assertive single self-disclosure of the period—first-place gold order-book depth claimed on a March 23, 2026 snapshot methodology across seven self-selected platforms [21]. The claim may be accurate; the methodology is promotional, and no third-party ranking aggregator has validated it. Similarly, Phemex's April 9, 2026 CNW release claims +300% week-over-week WTI and Brent growth [22]; Bitget's January 2026 Transparency Report claims approximately $4 billion TradFi daily volume [4]; Bybit's January 29, 2026 keynote includes a 16% global XAUT spot market-share claim [25]. Each of these figures is self-authored and distributed via PR wire; an institutional reader should treat them as directionally informative and quantitatively unaudited, and should anchor specific volume figures to BitMEX, JPMorgan, or RWA.xyz wherever possible.

On the RWA side, RWA.xyz is the category's public dashboard and is independent of issuers, though its underlying data combines on-chain indexing with issuer disclosures [5][6]. The April 2026 live dashboard occasionally surfaces apparent anomalies—a large "USDM1" aggregation that can exceed category totals and should not be cited as product AUM without a specific methodology check. Investax's Q1 2026 RWA report and MetaMask's April 2026 RWA categorization post both produce figures consistent with the $13.4 billion tokenized-Treasury and $7.37 billion tokenized-commodity aggregates cited in Chapter 3 of this report.

Hyperliquid's stats endpoint and associated Dune dashboards are on-chain data: the raw flows are verifiable by any observer. But the attribution of volume to specific HIP-3 deployers—Trade[XYZ], Felix Protocol, and others—relies on the deployer's own contract addressing, which the deployer controls. The $1.7 billion Crude Oil peak reported by JPMorgan is independently observable on-chain; the $100 billion Trade[XYZ] cumulative figure is not trivially reproducible, because Trade[XYZ] operates multiple instruments and the aggregation method is the issuer's [9][10].

The practical implication for institutional readers: when citing Q1 2026 TradFi-perp volume, cite BitMEX Q1 2026 as the method-transparent originator; when citing product AUM in tokenized RWAs, cite RWA.xyz with a specific date-stamp; when citing exchange market-share rankings, require a disclosed methodology; and when citing Hyperliquid HIP-3 deployer volume, prefer JPMorgan's Panigirtzoglou note or on-chain DefiLlama aggregates over issuer marketing releases.

Chapter 8 · The Regulatory Topology

Institutional readers should carry four regulatory anchors from this research.

First, ESMA's March 19, 2025 guidelines qualify perpetual futures as MiFID II financial instruments where the underlying is listed in MiFID II Annex I Section C [23]. Combined with ESMA Decision 2018/796 on retail CFD leverage caps (30:1 for major FX, descending to 2:1 for cryptocurrencies) and ESMA's MiCA positions on non-compliant stablecoins, the effect is that Model 1 products cannot be offered to EU retail by authorized CASPs in their current form, and Model 2 products cannot be offered to EU retail without the 2018 leverage caps applied [23][26].

Second, Mauritius's VAITOS Act 2021, which commenced on February 7, 2022, and its implementing FSC Rules effective July 1, 2022, together provide the Virtual Asset Service Provider licensing framework under which Mauritius-licensed exchange entities operate [45]. The Investment Dealer Licence under the Mauritius Securities Act 2005, with its tiered capital minima (MUR 700,000 for Broker; MUR 1,000,000 for Full Service excluding Underwriting; MUR 10,000,000 for Full Service), provides the complementary CFD-brokerage regulatory path [46]. The Seychelles Securities Dealer Licence under the Securities Act 2007, amended January 1, 2025 to raise minimum paid-up capital from USD 50,000 to USD 100,000 and to introduce perpetual licensing, provides a parallel offshore path [47]. Neither jurisdiction imposes ESMA-style retail leverage caps, and neither requires negative-balance protection on the same terms as EU or UK regulation.

Third, CFTC Chairman Michael Selig's January 29, 2026 "Next Phase of Project Crypto" speech, delivered at the joint CFTC-SEC Harmonization Event, signals a deliberate U.S. regulatory posture of bringing perpetuals inside the CFTC perimeter rather than continuing to push them offshore, with explicit reference to "both centralized and decentralized markets" [33]. The CFTC's December 8, 2025 Press Release 9146-25, announcing the Digital Assets Pilot Program for Tokenized Collateral in Derivatives Markets, operationalized part of that posture by authorizing Bitcoin, Ether, and eligible payment stablecoins (with USDC as the identified example) as collateral at regulated derivatives firms during the first three months of FCM reliance under Staff Letter 25-40 [24]. USDT does not at present meet the "eligible payment stablecoin" criteria identified in the Staff Letter, and that non-qualification is the mechanism by which Model 1 is structurally separated from Model 5 in the U.S. jurisdiction.

Fourth, IOSCO's October 16, 2025 Thematic Review FR/13/2025 (IOSCOPD801) of its 2023 Crypto and Digital Asset Recommendations (IOSCOPD747) found that "overall, significant progress is being made, but there is still much more to be done, especially as new crypto-asset business models are being developed" [48]. No IOSCO document specifically addresses crypto derivatives as a standalone policy category in 2025–2026; crypto-derivative regulation is currently a composite of national MiFID II, CFTC, FCA, and ESMA action under the IOSCO CDA recommendations umbrella.

The interaction of these four anchors produces the jurisdictional map that explains the five-model divergence. MiCA-authorized CASPs cannot run Models 1 or 2 for EU retail. Mauritius and Seychelles run Model 2 without retail leverage caps. ADGM (Nest Exchange Limited for Binance) and Bermuda (Payward Digital Solutions for Kraken) run Models 1 and 3 under tailored digital-asset frameworks that sit outside both MiCA and the ESMA CFD regime. Hyperliquid runs Model 4 outside any single regulator's direct reach, with the licensed-benchmark overlay (S&P DJI) as the only formal legal connection to the TradFi stack. The CFTC runs Model 5 under Regulation 40.2 self-certification and the December 2025 Digital Assets Pilot. Five regulators, five architectures, five collateral standards, five retail-protection regimes—the divergence is topology, not coincidence.

Chapter 9 · Reverse Signals

A research thesis earns its keep by being falsifiable. Three observable conditions, if any one of them materializes within the next 12–24 months, would require the five-model framework in this report to be substantially revised or withdrawn.

Signal A · Market-share concentration above 70%. The five-model thesis predicts coexistence. The falsification condition has two possible triggers. First, if by end-2026 or end-2027 any single architectural model captures more than 70% of TradFi-perpetual volume, measured weekly or monthly on an aggregated basis across BitMEX, Kaiko, or CCData methodology. Second, if any single model captures more than 70% of active TradFi-exposed users on crypto venues on the same aggregation basis. If either trigger fires, the coexistence thesis is falsified; the market would then be converging rather than diverging, and the appropriate framing would be a consolidation study rather than a taxonomy. The current Q1 2026 distribution—Binance-led Model 1 plus OKX; Bybit-and-Bitget-led Model 2; RWA.xyz-documented Model 3; Hyperliquid-led Model 4; and ICE-Kraken-Bitnomial-led Model 5—has no single model above 45% of aggregate TradFi-perpetual volume on the BitMEX Q1 2026 decomposition [1]. A shift to above 70% concentration would be a qualitative regime change.

Signal B · Cross-architecture unified regulatory framework. The thesis predicts that five regulators, five collateral standards, and five retail-protection regimes underpin the five models. If a major jurisdiction—the United States, the European Union, the United Kingdom, Singapore, or Japan—publishes by end-2027 a unified regulatory framework that treats USDT-settled perpetuals, offshore CFDs, and licensed-overlay DEX perpetuals as a single product category under a shared disclosure, capital, and retail-protection regime, the "architectures are anchored to distinct regulators" premise is substantially weakened. Early-warning indicators would include CFTC-ESMA-FCA joint statements, IOSCO CDA-follow-up recommendations extending to perpetuals specifically, or MiCA Level 2 delegated acts that bring third-country perpetuals into the same classification as EU-CASP-offered derivatives.

Signal C · Model 5 regulatory failure. The thesis treats Model 5—ICE-OKX, NYSE-Securitize, Kraken-Bitnomial—as the mechanism by which U.S.-onshore, incumbent-cleared TradFi-crypto convergence becomes feasible. If the ICE-OKX transaction is blocked, unwound, or materially restructured by U.S. or other regulators; if the April 17, 2026 NYSE tokenized-securities rule is suspended by the SEC within the 60-day window; or if the Kraken-Bitnomial acquisition is delayed beyond 18 months from announcement for regulatory reasons, Model 5's viability as a near-term convergence rail is substantially weaker, and the analysis would need to re-weight Models 1, 3, and 4 accordingly.

We commit to publishing a Signal Tracking follow-up in Q4 2026 that revisits each of these three signals against then-current data.

Chapter 10 · Why Coexistence Rather Than Convergence

The natural question after a five-model taxonomy is whether the models will converge. On the 18-to-36-month horizon that institutional allocators typically plan against, we see no structural pathway to convergence based on the regulatory and collateral constraints documented in Chapters 1 through 8. The reasons are structural rather than contingent, and the section below summarizes them.

USDT settlement has not been approved as collateral at U.S. CFTC-regulated derivatives firms; the December 8, 2025 Digital Assets Pilot authorized "Bitcoin, Ether, and eligible payment stablecoins," and USDT does not at present meet the eligibility criteria in Staff Letter 25-40 [24]. That non-qualification separates Model 1 from Model 5 under current U.S. rules. Similarly, the MiCA regime's position on non-compliant stablecoins separates Model 1 from EU-authorized-CASP distribution [23]. USDT is, in practice, a jurisdictional commitment rather than a currency choice; exchanges building Model 1 have implicitly chosen the MENA, CIS, Latin America, and Southeast Asia corridors over the U.S. and EU axes. Incumbents building Model 5 have implicitly chosen the U.S. and EU axes over the offshore corridor. The two choices do not reconcile on current rules.

MT5 is unlikely to evolve into a tokenized-RWA issuer on the current regulatory and economic constraints. The Bybit and Bitget TradFi stacks run on infrastructure whose economics depend on leverage, spread, and client churn under a bilateral broker-client model. The xStocks stack runs on infrastructure whose economics depend on custodian segregation, prospectus compliance, and 1:1 redemption. The two can be packaged as adjacent features in the same app—Bitget already does this—but the underlying books and the bankruptcy waterfalls are not interchangeable. A CFD is a bilateral derivative; a tokenized share is a bearer claim on a segregated asset; merging them would dissolve the regulatory premise of both.

HIP-3 is not a natural substrate for the ICE, NYSE, and Kraken-Bitnomial stacks. Model 4's permissionless DEX is designed to route around the gatekeeping function that Model 5's CFTC-regulated DCM, DCO, and FCM architecture is designed to provide. A permissionless S&P 500 perpetual with a licensed benchmark overlay is not a substitute for a CFTC-regulated S&P 500 futures contract with central clearing and FCM margin segregation. The two will likely run in parallel with different user bases, different clearing arrangements, different collateral, and different regulatory surfaces—much as OTC swaps and listed futures have coexisted for more than four decades after Dodd-Frank was expected by some to collapse them.

The tokenized-RWA category (Model 3) will grow inside whichever regulator each issuer has chosen. Hashnote operates under Cayman, Circle is federally regulated in the United States, Ondo Global Markets distributes through Oasis Pro's SEC-licensed broker-dealer and ATS, Backed Finance operates under Liechtenstein FMA approval with Swiss DLT Act recognition, and Paxos operates under NYDFS and OCC. These are not competing interpretations of a single jurisdictional framework; they are distinct jurisdictional claims, each of which will be tested independently over the next credit cycle.

The single institutional framing that holds up against the primary sources is this: the period from October 2025 through April 2026 is when crypto-exchange TradFi expansion stopped being one story and became five. Volume grew approximately fifty-seven-fold on BitMEX's aggregation [1]; positional rotations occurred at issuer level; a CFTC chairman used the word "decentralized" in prepared remarks [33]; and NYSE filed for tokenized-securities trading [14][16]. No single one of those is the defining development; the defining development is that the architectures diverged sufficiently that a future consolidation thesis would have to reconcile with the primary sources documented in this report. Any institutional reader modeling this market should allocate across the five models as distinct exposures, price each against its own regulator, and avoid the analytically convenient mistake of treating "crypto exchange TradFi" as a single product category. It is five categories. On the evidence available as of April 23, 2026, the five will still be five when we update this report in Q4 2026.

Statement

Research scope and limitations. This report focuses on the architectural, regulatory, and user-segmentation structure of crypto-exchange expansion into traditional-finance asset classes during the six-month window from October 2025 to April 23, 2026. It does not cover: price predictions for any crypto asset or traditional asset class; specific trading strategy recommendations; fundamental analysis of any commodity (including oil, gold, silver, or platinum-group metals); fundamental analysis of any tokenized equity or ETF; technical comparison of RWA issuance, custody, and redemption layers at sub-issuer detail; or unit-economic comparison of the five architectural models at the exchange level. Each of those would be an independent research topic.

Data currency. All market data, regulatory citations, and exchange announcements referenced in this report are based on publicly available information as of April 23, 2026. High-frequency indicators—TradFi-perpetual weekly volume, tokenized-RWA AUMs, ETF and exchange flows, Hyperliquid HIP-3 deployer volume—may change materially within days of publication. Readers should treat this report as an analysis at a specific time slice.

Research independence. This report is independently written by Bitbase Research, and its analytical conclusions are based on publicly available primary sources and the research team's independent judgment. The five-model taxonomy (Models 1 through 5) is a research construct developed in this report and does not represent the official classification of any regulator or standards body. Specific institution names in this report (Binance, Nest Exchange Limited, OKX, Kraken, Payward Digital Solutions Ltd., Bybit, Bitget, MEXC, Phemex, Crypto.com, Hyperliquid, Felix Protocol, Trade[XYZ], BlackRock, Hashnote, Ondo, Franklin Templeton, Superstate, Paxos, Tether, Backed Finance, Coinbase, Bitnomial, CME Group, ICE, NYSE, Securitize, BNY, Citi, Infra Capital, eToro, Plus500, IG Group) serve only as objective references for describing the industry landscape; inclusion is not an endorsement, and absence is not a negative signal.

Conflict-of-interest disclosure. Bitbase operates a centralized exchange and may offer products within Model 1 (CEX-native stablecoin-settled perpetuals) as analyzed in this report. Readers should take this into account when interpreting the report's analysis of Model 1 and its comparison to the other four models. The analytical framework in this report was developed independently of any specific product plan, and the report makes no statement about any specific Bitbase product, upcoming or otherwise. The report's arguments and reverse signals apply symmetrically to all five models, including the model Bitbase may occupy.

Tools and generation assistance. This report used advanced large language models as research-assistance tools in material gathering, cross-source fact verification, structured argument, and draft writing. All primary data, regulatory documents, attestation reports, and market indicators were human-verified against their original sources. Specific numerical figures, quoted language from regulators and executives, and licensing-entity names were manually traced to primary sources (press releases, regulatory filings, attestation PDFs, and issuer documentation). We acknowledge the inherent error risk of AI-assisted research in long-tail data handling and have reduced it through multi-round fact-checking, but we cannot fully eliminate it.

Non-investment-advice statement. This report does not constitute investment advice, a recommendation to buy, sell, or hold any financial instrument, or a solicitation for any financial product or service. The five-model taxonomy is a research framework; it is not a portfolio-construction methodology and does not carry any statement about the expected return, risk, or suitability of any product within any of the five models. Readers should consult independent, licensed financial, legal, and tax advisors before acting on any information in this report.

Forward-looking-statement risk. Statements in this report concerning CFTC posture, ESMA and MiCA evolution, IOSCO guidance, and the future structure of U.S., EU, UK, Mauritius, and Seychelles regulation are forward-looking and carry uncertainty. Regulatory outcomes depend on rulemaking processes, enforcement decisions, and political developments that are not under any single actor's control. Readers should treat forward-looking statements as conditional on publicly available information as of April 23, 2026 and subject to revision.

Signal tracking. Bitbase Research commits to publishing a Signal Tracking follow-up in Q4 2026, revisiting the three reverse signals defined in Chapter 9 against then-current data.

References

[1] BitMEX (Shang Wu), "Q1 2026 Derivatives Report: The TradFi Perpetual Swap Revolution," published April 9, 2026. https://www.bitmex.com/blog/2026q1-derivatives-report

[2] Binance / PR Newswire, "Binance Launches First Regulated TradFi Perpetual Contracts Settled in Stablecoin, Starting with Gold and Silver," dated January 8, 2026 (Abu Dhabi dateline; XAUUSDT live January 5, 2026; XAGUSDT live January 7, 2026). https://www.prnewswire.com/news-releases/binance-launches-first-regulated-tradfi-perpetual-contracts-settled-in-stablecoin-starting-with-gold-and-silver-302656186.html

[3] Bybit / PR Newswire, "Introducing Bybit TradFi: Trading the World on Bybit," June 17, 2025. https://www.prnewswire.com/news-releases/introducing-bybit-tradfi-trading-the-world-on-bybit-302482656.html

[4] Bitget, "Bitget January 2026 Transparency Report: TradFi Hits $4B Daily," January 2026. https://www.bitget.com/blog/articles/bitget-january-2026-transparency-report-tradfi-4b-daily-volume

[5] RWA.xyz, Tokenized Treasuries and Tokenized Commodities dashboards, snapshot accessed April 22–23, 2026. https://app.rwa.xyz/treasuries ; https://app.rwa.xyz/commodities

[6] InvestaX, "Q1 2026 Real World Asset Tokenization Market Report," April 2026 (citing RWA.xyz aggregations). https://investax.io/blog/q1-2026-real-world-asset-tokenization-market-report

[7] Hyperliquid Documentation, "HIP-3: Builder-deployed perpetuals." https://hyperliquid.gitbook.io/hyperliquid-docs/hyperliquid-improvement-proposals-hips/hip-3-builder-deployed-perpetuals

[8] CoinDesk, "Hyperliquid's HIP-3 Upgrade to Unlock Permissionless Perp Market Creation," October 13, 2025. https://www.coindesk.com/business/2025/10/13/hyperliquid-s-hip-3-upgrade-to-unlock-permissionless-perp-market-creation

[9] S&P Dow Jones Indices / Trade[XYZ], "S&P Dow Jones Indices Licenses S&P 500® to Trade[XYZ] for Perpetual Contracts on Hyperliquid," March 18, 2026 (New York). https://press.spglobal.com/2026-03-18-S-P-Dow-Jones-Indices-Licenses-S-P-500-R-to-Trade-XYZ-for-Perpetual-Contracts-on-Hyperliquid

[10] The Block, "JPMorgan notes Hyperliquid gaining traction as traders seek 24/7 oil trading," March 18, 2026 (reporting on JPMorgan research note led by Managing Director Nikolaos Panigirtzoglou). https://www.theblock.co/post/394380/jpmorgan-hyperliquid-crypto-traction-24-7-oil-trading

[11] CoinDesk, "Hyperliquid oil volume booming thanks to war in Middle East: JPMorgan," March 20, 2026. https://www.coindesk.com/business/2026/03/20/iran-war-volatility-is-driving-oil-trading-boom-on-hyperliquid-says-jpmorgan

[12] ICE / BusinessWire, "ICE Makes Investment in OKX, Establishing Strategic Relationship," March 5, 2026. https://www.businesswire.com/news/home/20260305216092/en/ICE-Makes-Investment-in-OKX-Establishing-Strategic-Relationship

[13] Bloomberg, "NYSE Owner Invests in Crypto Exchange at $25 Billion Valuation," March 5, 2026. https://www.bloomberg.com/news/articles/2026-03-05/nyse-owner-invests-in-crypto-exchange-at-25-billion-valuation

[14] NYSE / ICE Investor Relations, "The New York Stock Exchange Develops Tokenized Securities Platform," January 19, 2026. https://ir.theice.com/press/news-details/2026/The-New-York-Stock-Exchange-Develops-Tokenized-Securities-Platform/

[15] NYSE / ICE Investor Relations, "New York Stock Exchange and Securitize Agree to Memorandum of Understanding to Support Tokenized Securities," March 24, 2026. https://ir.theice.com/press/news-details/2026/New-York-Stock-Exchange-and-Securitize-Agree-to-Memorandum-of-Understanding-to-Support-Tokenized-Securities/

[16] U.S. Securities and Exchange Commission, Release No. 34-105260, File No. SR-NYSE-2026-17, "Notice of Filing and Immediate Effectiveness of Proposed Rule Change" (new NYSE Rule 7.50), posted April 17, 2026. https://www.sec.gov/files/rules/sro/nyse/2026/34-105260.pdf

[17] Kraken (Payward), "Payward to acquire Bitnomial, creating a fully CFTC-licensed derivatives platform," April 17, 2026. https://blog.kraken.com/news/payward-acquires-bitnomial

[18] Decrypt, "OKX Rolls Out Round-the-Clock Trading for Mag Seven Stocks Using Crypto Collateral," March 24, 2026. https://decrypt.co/362158/okx-equity-perps-mag-7-sp-500

[19] The Block, "OKX launches equity perpetual swaps, offering 5x leverage to 'Mag 7' stocks," March 24, 2026. https://www.theblock.co/post/394776/okx-equity-perpetual-swaps

[20] Crypto.com, "Introducing Commodity and U.S. Index Perpetual Contracts on the Crypto.com Exchange," April 1, 2026. https://crypto.com/en-ae/product-news/exchange-tradfi-perpetuals-launch

[21] MEXC, "MEXC Ecosystem & Growth Report Q1 2026," April 22, 2026 (self-published; snapshot methodology dated March 23, 2026). https://blog.mexc.com/mexc-ecosystem-growth-report-q1-2026/

[22] Phemex / CNW, "Phemex TradFi Crude Oil Trading Surges 300% as Ceasefire Volatility Sparks Record Demand," April 9, 2026. https://www.newswire.ca/news-releases/phemex-tradfi-crude-oil-trading-surges-300-as-ceasefire-volatility-sparks-record-demand-858534546.html

[23] European Securities and Markets Authority, Guidelines on the qualification of crypto-assets as financial instruments under MiFID II, published March 19, 2025; and ESMA public statements on non-compliant stablecoins under MiCA. https://www.esma.europa.eu/

[24] Commodity Futures Trading Commission, Press Release 9146-25, "Acting Chairman Pham Announces Launch of Digital Assets Pilot Program for Tokenized Collateral in Derivatives Markets," December 8, 2025 (Staff Letter 25-40 specifying Bitcoin, Ether, and eligible payment stablecoin collateral). https://www.cftc.gov/PressRoom/PressReleases/9146-25

[25] Bybit / PR Newswire, "Bybit CEO Ben Zhou to Unveil 2026 Roadmap in Keynote Heralding New Era for Digital Finance," January 29, 2026. https://www.prnewswire.com/news-releases/bybit-ceo-ben-zhou-to-unveil-2026-roadmap-in-keynote-heralding-new-era-for-digital-finance-302663331.html

[26] European Securities and Markets Authority, Decision 2018/796 (adopted May 22, 2018; OJ publication June 1, 2018; applied from August 1, 2018 for CFDs); and ESMA press release "ESMA agrees to prohibit binary options and restrict CFDs to protect retail investors," March 27, 2018. https://www.esma.europa.eu/press-news/esma-news/esma-agrees-prohibit-binary-options-and-restrict-cfds-protect-retail-investors

[27] UK Financial Conduct Authority, Policy Statement PS19/18, "Restricting contract for difference products sold to retail clients," confirmed July 1, 2019 (CFD rules from August 1, 2019; CFD-like options from September 1, 2019). https://www.fca.org.uk/publications/policy-statements/ps19-18-restricting-contract-difference-products ; press release https://www.fca.org.uk/news/press-releases/fca-confirms-permanent-restrictions-sale-cfds-and-cfd-options-retail-consumers

[28] Paxos, "Pax Gold (PAXG) Transparency Reports" (auditor change to KPMG LLP effective February 28, 2025, pursuant to NYDFS Dollar-Backed Stablecoin guidance; prior auditor WithumSmith+Brown, PC). https://www.paxos.com/paxg-transparency

[29] Tether Gold, Q1 2025 and Q3 2025 Attestation Reports by BDO Italia S.p.A., ISAE 3000R reasonable-assurance engagements. Q1 2025 PDF (reporting date March 31, 2025; published April 28, 2025): https://gold.tether.to/docs/reports/attestations/ISAE\_3000R\_-\_Opinion\_TGRR\_31.03.2025\_RC187322025BD0035.pdf ; Q3 2025 PDF (reporting date September 30, 2025; published October 28, 2025): https://gold.tether.to/docs/reports/attestations/

[30] Kraken (Payward), "Payward announces acquisition of Backed Finance AG," December 2, 2025. https://blog.kraken.com/news/backed-acquisition

[31] Kraken (Payward), "Announcing the world's first regulated, tokenized-equity perpetual futures, using xStocks," February 24, 2026. https://blog.kraken.com/product/xstocks/tokenized-equity-perpetual-futures

[32] Felix Protocol, launch announcement for Crude Oil (WTI) perpetual on Hyperliquid via HIP-3, January 9, 2026 at 09:47 UTC. https://x.com/felixprotocol/status/2009638142035320907

[33] CFTC Chairman Michael S. Selig, "The Next Phase of Project Crypto: Unleashing Innovation for the New Frontier of Finance," remarks at the joint CFTC-SEC Harmonization Event, January 29, 2026. https://www.cftc.gov/PressRoom/SpeechesTestimony/opaselig1

[34] Willkie Farr & Gallagher LLP, "Willkie Alum Michael Selig Confirmed as 16th CFTC Chairman," December 2025 (documenting Senate confirmation December 18, 2025; sworn in December 22, 2025). https://www.willkie.com/news/2025/12/willkie-alum-michael-selig-confirmed-as-16th-cftc-chairman ; CFTC Chairman page: https://www.cftc.gov/About/Commissioners/MichaelSelig/index.htm

[35] ICE Investor Relations, "ICE Announces Strategic Investment in Polymarket," October 7, 2025 (up to $2 billion investment at $8 billion pre-investment valuation / $9 billion post-investment). https://ir.theice.com/press/news-details/2025/ICE-Announces-Strategic-Investment-in-Polymarket/

[36] Bitnomial / PR Newswire, "Bitnomial Exchange Self-Certifies First Ever U.S. Perpetual Futures Contracts," April 23, 2025 (trading live April 28, 2025; self-certification under CFTC Regulation 40.2(a)). https://www.prnewswire.com/news-releases/bitnomial-exchange-self-certifies-first-ever-us-perpetual-futures-contracts-302435713.html

[37] Bitnomial Exchange, Product Filing 25-016 (CFTC submission dated April 23, 2025; eight-hour funding intervals; 25-year nominal expiry). https://bitnomial.com/exchange/regulatory/cftc/product-filings/25-016.pdf

[38] Markets Media, "Bitnomial Is First CFTC-Regulated Exchange to Accept Digital Asset Margin," September 17, 2025. https://www.marketsmedia.com/bitnomial-is-first-cftc-regulated-exchange-to-accept-digital-asset-margin/

[39] Bitnomial / PR Newswire, "Bitnomial Announces Launch of Leveraged Retail Spot Crypto Exchange," December 4, 2025 (first CFTC-regulated leveraged retail spot crypto exchange; live week of December 8, 2025). https://www.prnewswire.com/news-releases/bitnomial-announces-launch-of-leveraged-retail-spot-crypto-exchange-302633203.html

[40] Coinbase, "Coming July 21: US Perpetual-Style Futures" and subsequent launch post "Perpetual futures have arrived in the U.S.," July 2025 (5-year expiry; hourly funding settled twice daily; up to 10× crypto and 20× metals leverage; nano BTC and nano ETH contracts). https://www.coinbase.com/blog/coming-july-21-us-perpetual-style-futures ; https://www.coinbase.com/blog/perpetual-futures-have-arrived-in-the-us

[41] eToro Group Ltd., Form F-1/A (SEC EDGAR, declared effective May 13, 2025); Q1 2025 press release, May 2025 (approximately 3.5 million funded accounts at December 31, 2024; 3.58 million at March 31, 2025; 40 million registered users across 75 countries; FY2024 commissions $931 million with crypto 38%, equities 38%, commodities 20%, currencies 4%; crypto net trading contribution 10% in 2023 to ~25% in 2024). https://investors.etoro.com/news-releases/

[42] CNBC, "Stock trading app eToro pops 29% in Nasdaq debut after pricing IPO above expected range," May 14, 2025 (first-day close valuation above $5.4 billion; ticker ETOR). https://www.cnbc.com/2025/05/14/stock-trading-app-etoro-ipos-debuts-on-nasdaq.html

[43] Plus500 Ltd., FY2024 Annual Report, published via RNS on March 24, 2025. https://cdn.plus500.com/media/Investors/Reports/Plus500\_FY\_Annual\_Report\_2024.pdf

[44] IG Group Holdings plc, FY25 Results Statement (year to May 31, 2025), published July 24, 2025. https://www.iggroup.com/\~/media/Files/I/IG-Group/documents/investors/financial-results/results-reports-and-presentations/2025/ig-group-fy25-results-statement.pdf

[45] Mauritius Financial Services Commission, Virtual Asset and Initial Token Offering Services Act 2021 (commenced February 7, 2022 via Proclamation No. 12/2022; FSC VAITOS Rules effective July 1, 2022). https://www.fscmauritius.org/media/119928/the-virtual-asset-and-initial-token-offering-services-act.pdf ; VAITOS FAQs https://www.fscmauritius.org/media/119930/faqs-vaitos-act-2021.pdf

[46] Mauritius FSC, Investment Dealer Licence tiers under the Securities Act 2005 and Securities (Licensing) Rules 2007: Broker (MUR 700,000), Full Service Dealer excluding Underwriting (MUR 1,000,000), Full Service Dealer including Underwriting (MUR 10,000,000); Global Business Corporation status under the Financial Services Act 2007. https://www.fscmauritius.org/

[47] Seychelles Financial Services Authority, Securities Act 2007 as amended by the Securities (Amendment) Act 2024 (effective January 1, 2025; minimum paid-up capital raised from USD 50,000 to USD 100,000; perpetual licensing introduced with an annual fee of USD 6,000). https://fsaseychelles.sc/

[48] IOSCO, FR/13/2025 / IOSCOPD801, "Thematic Review: Assessing the Implementation of IOSCO Recommendations for Crypto and Digital Asset Markets," October 16, 2025 (thematic review of the 2023 CDA Recommendations, IOSCOPD747). Report: https://www.iosco.org/library/pubdocs/pdf/IOSCOPD801.pdf ; press release: https://www.iosco.org/news/pdf/IOSCONEWS774.pdf