Executive summary

Crypto derivatives infrastructure is going through a structural divergence. This is not a violent paradigm break but a long-wave cycle that plays out across 2026 to 2030. On March 17, 2026, the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) jointly issued the "Project Crypto" interpretive guidance, establishing a five-class asset framework — digital commodities, digital collectibles, digital tools, stablecoins, and digital securities — with the first four expressly held not to be securities [1]. Three days later, on March 19, the Federal Reserve, the OCC, and the FDIC re-proposed the U.S. Basel III endgame rule, cutting large banks' total CET1 requirement by roughly 2.4% versus the 2023 version [2]. At the same time, the EU's Markets in Crypto-Assets regulation (MiCA) transition period runs out on July 1, 2026, with the Netherlands, Poland, Finland, Latvia, Hungary, and Slovenia having ended their transition early back in mid-2025 [3]. Read together, these three regulatory events are not a coordinated crackdown on "offshore" — they are an institutional competition in which the major financial jurisdictions are racing to bring crypto inside their existing frameworks.

This report rests on four falsifiable theses.

Thesis 1 — two tracks coexist; there is no single winner. Crypto derivatives will evolve along two main tracks: multi-jurisdiction compliant centralized clearing entities (spanning CFTC-regulated DCOs/FCMs in the U.S., MiCA CASP-licensed firms in the EU, and licensed venues across other financial centers) and on-chain native decentralized derivatives protocols (represented by a perpetual-DEX ecosystem that turned over $7.9 trillion in 2025 [4]). The thesis is falsified if, five years out, either track's market share stabilizes below 5% of the industry total.

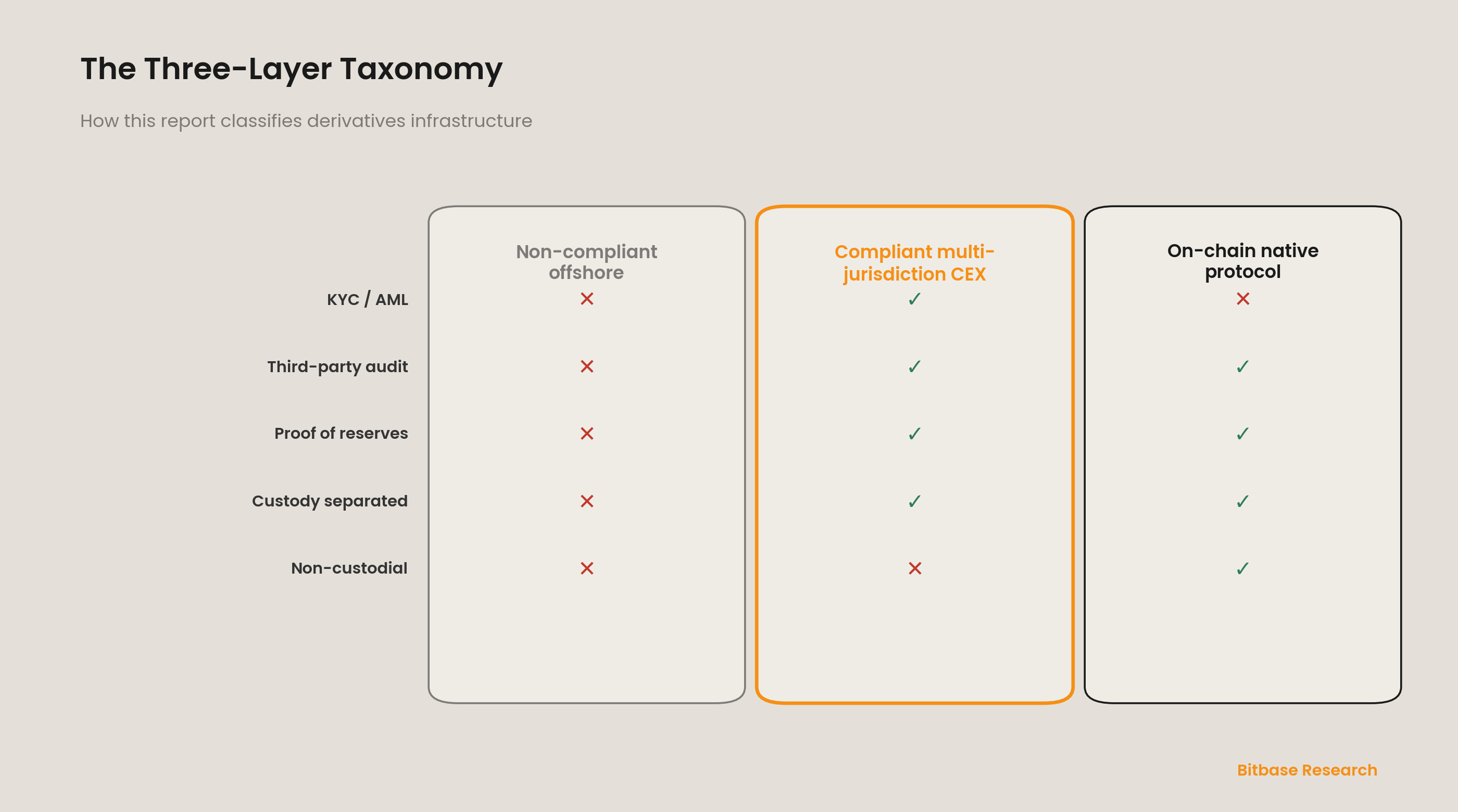

Thesis 2 — what gets culled is "non-compliant offshore," not "offshore" itself. The architectures under real structural pressure are those without KYC/AML, without third-party audits, without proof of reserves, running a B-book internalized house position, with custody and matching fused together. Jurisdiction of registration is a secondary variable; compliance architecture, custody isolation, and reserve transparency are the primary discriminants.

Thesis 3 — the macro-liquidity channel is switching asymmetrically. Under the Fed's ample-reserves framework and a 3.50%–3.75% federal funds rate [5], capital is shifting from "retail fiat spillover" to "institutional allocation plus compliant ETF inflows." As of April 2026, U.S. spot Bitcoin ETFs held roughly $85–98 billion in assets [6]. This channel shift is an asymmetric tailwind for the compliant-centralized and on-chain-native tracks, and an asymmetric headwind for non-compliant offshore architecture.

Thesis 4 — hidden execution-quality costs are shared across both tracks. The adverse-selection cost of CEX internalized market-making and the LVR/MEV borne on DEXs are two expressions of the same phenomenon on different infrastructure — both tracks push a hidden cost onto liquidity providers, differing only in observability and in how institutions respond.

To keep the analysis consistent, the report uses a three-layer taxonomy. Layer 1, non-compliant offshore — no KYC/AML, no third-party audit, no proof of reserves, B-book internalization, custody and matching fused. Layer 2, compliant multi-jurisdiction centralized exchanges — licensed under internationally recognized frameworks, full KYC/AML, proof of reserves, independent custody, and third-party audit. Layer 3, on-chain native derivatives protocols — non-custodial, transparent code, secured by cryptographic consensus. This framework runs through all six parts of the report.

The reason this divergence is a "long-wave cycle" rather than a sudden event is that regulatory frameworks need multiple rounds of rulemaking and case law to land (the U.S. Basel III endgame comment period runs to June 18, 2026; MiCA level-2 measures are still rolling out), the technology stack needs cross-chain interoperability and Layer-2 liquidity aggregation to mature, and behavioral change among market participants has to be validated across several volatility cycles.

The practical implication for allocators, brokers, and quant firms: in a two-track world, cross-venue execution-quality monitoring, transparent market-maker disclosure, and smart order routing become core competitive dimensions. Capital efficiency — especially the yield-ization of collateral — will displace pure fee competition as the first-order consideration when choosing a derivatives venue.

What would overturn the core thesis? We identify three reverse signals observable within 12 to 24 months. First, if two or more of the major compliant jurisdictions (the U.S., EU, Singapore, Japan) withdraw or materially freeze their crypto-derivatives licensing frameworks before the end of 2027, the institutional-competition premise fails. Second, if monthly perpetual-DEX volume shrinks back below the Q1-2025 level (about $150 billion per month) through end-2027 with no recovery, the structural-expansion premise for the on-chain-native track fails. Third, if spot Bitcoin ETFs see six consecutive months of net redemptions and total AUM contracts by more than 40%, the institutional-allocation channel-switch thesis needs to be re-assessed.

Part 1 · The repricing of macro liquidity

The crypto derivatives market's long-standing assumption of "macro-liquidity spillover" — that broad money-supply expansion automatically seeps into crypto risk assets — is being systematically repriced in 2026 by the combined force of the Fed's ample-reserves regime, the money-market-fund siphon, and a high-rate environment. This does not mean the end of the crypto market; it means a fundamental change in the channel and the character of capital inflows, from "retail fiat spillover" to "institutional allocation and compliant ETF inflows."

One macro backdrop needs adding: on February 28, 2026, a sharp escalation in Middle East geopolitics pushed oil above $100 a barrel and kept it there, an exogenous shock to the Q1 narrative [100]. That energy shock pushed the Fed at its March 18 FOMC to raise its 2026 core-PCE projection from the December 2025 SEP's 2.5% to 2.7%, and to compress the market's expected 2026 rate cuts from two at the start of the year to at most one [101]. This "energy shock plus more hawkish Fed" combination does not shake this part's core thesis — if anything, it reinforces our read of the long-wave divergence in two ways: higher risk-free-rate expectations magnify the opportunity cost of non-yield-bearing collateral and accelerate the capital-efficiency generation gap, and inflation stickiness produced a structural inflection in the MMF siphon around March 18 (see the end of section 1.2).

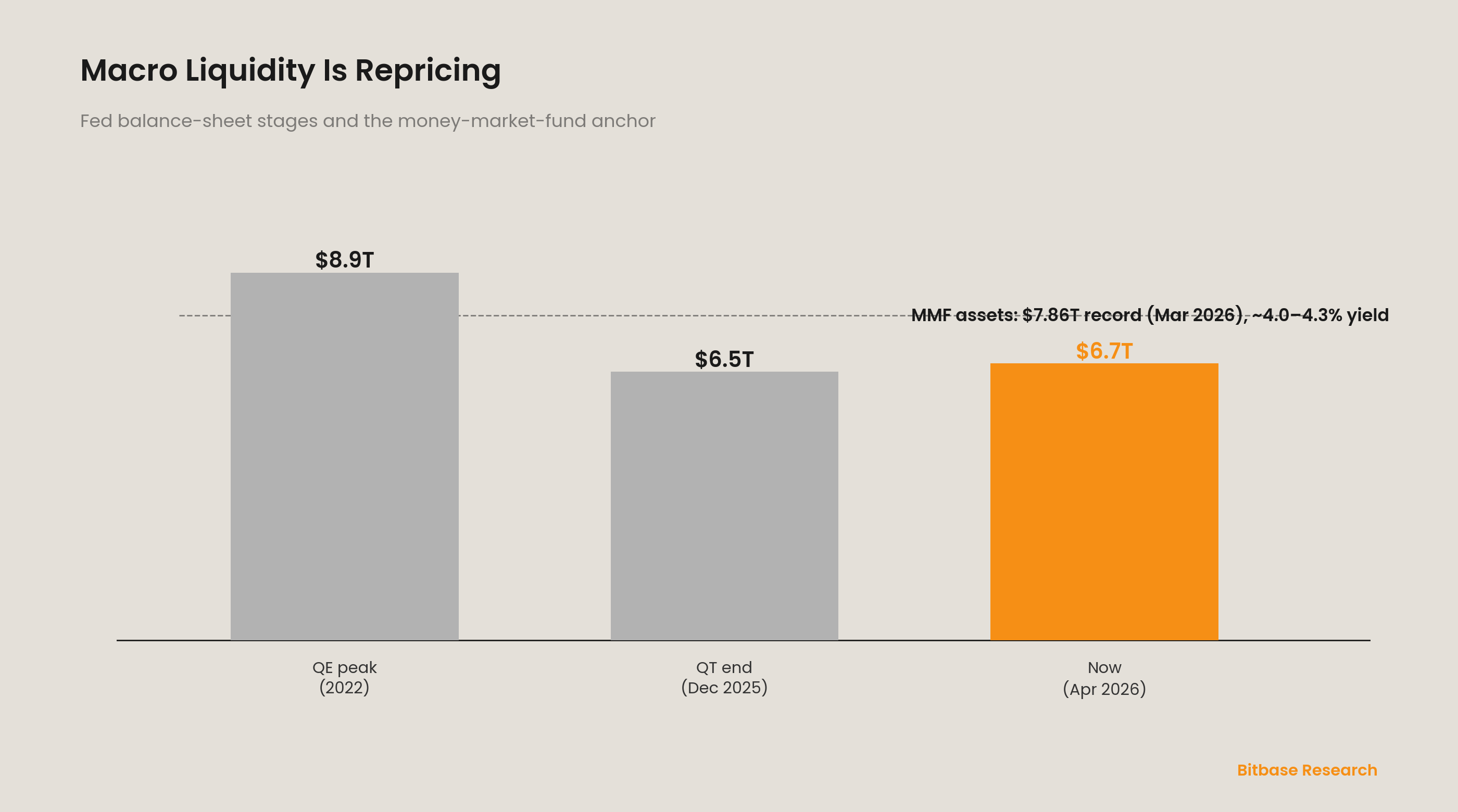

1.1 From QE to ample reserves: the three stages of the Fed balance sheet

Understanding crypto's liquidity environment means tracing three stages of the Fed's balance sheet. Unlimited quantitative easing from March 2020 to early 2022 lifted total assets from about $4 trillion to a peak near $8.9 trillion, creating the loosest liquidity conditions in history. Quantitative tightening, launched in June 2022 at up to $95 billion a month, ran until it formally ended on December 1, 2025, with total assets down to about $6.5 trillion — recovering only about half of the pandemic-era expansion [7].

The key pivot came in the post-QT transition. The Fed did not turn to a new round of QE; it entered a reserve-management-purchase phase, reinvesting maturing Treasury principal into newly issued Treasuries and maturing agency-MBS principal into short-dated T-bills, to keep reserves matched to banking-system demand [8]. The March 2026 FOMC statement was explicit that it would reinvest "all principal payments from maturing agency securities into Treasury bills" [9]. The policy characterization matters: T-bill purchases are reserve management, not a new round of QE. Participants who misread it as a liquidity-expansion signal face systematic mispricing risk.

The same FOMC meeting (March 18, 2026) published a hawkish Summary of Economic Projections: the Fed raised its 2026 core-PCE projection to 2.7% and its 2027 projection to 2.2%, nudged 2026 real GDP growth from 2.3% to 2.4%, but kept the median funds-rate path at just one cut. The dispersion is more telling: 14 of 19 participants saw one or zero cuts this year, up sharply from 11 in the December SEP, with only Governor Stephen Miran voting for an immediate cut [101]. Meanwhile, U.S. 2025 payrolls were revised down from an originally reported 584,000 to 181,000, and February 2026 shed about 92,000 jobs — a weakening labor market that layers an extra dimension onto the Fed's dilemma [101]. This hawkish path keeps "high short-term rates plus a high opportunity cost for non-yield-bearing collateral" in place through 2026, rather than easing from Q2 as markets had expected at the start of the year.

As of early April 2026, Fed total assets were about $6.7 trillion [10]. The standard measure of net liquidity is Fed total assets minus the Treasury General Account (TGA) minus overnight reverse repo (ON RRP). ON RRP has fallen from its December 2022 peak of about $2.2 trillion to near zero (about $2.8 billion in February 2026), and the TGA sits around $910 billion [11], putting net liquidity at roughly $5.7–5.8 trillion. With the ON RRP buffer exhausted, any future TGA rebuild (for example after heavy issuance) will drain bank reserves directly — the cushion for liquidity transmission has narrowed materially.

1.2 The money-market-fund siphon: the $7.86 trillion opportunity-cost anchor

With the funds rate held at 3.50%–3.75% [5], money-market funds (MMFs) became steadily more attractive to idle capital from H2 2025 into Q1 2026. Per Investment Company Institute (ICI) data, U.S. MMF total assets hit an all-time peak of $7.856 trillion in the week of March 18, 2026 (base measure, excluding funds ICI does not cover), of which government funds were about $6.47 trillion (roughly 82.3%), prime funds about $1.24 trillion, and tax-exempt funds $143.1 billion [12]. Net MMF inflows over the prior 52 weeks were about $779 billion, an annual growth rate near 11.1% [12].

But an inflection worth watching appeared after March 18 — the very day of the FOMC decision that raised the 2026 PCE projection to 2.7%. In the following week (week of March 25), MMF assets fell $53 billion to $7.803 trillion, the largest single-week drawdown in more than a year; the week of April 1 rebounded a modest $7.8 billion to $7.811 trillion, and the week of April 8 (released by ICI on April 9) kept fluctuating in that range [12]. The broader-coverage Crane Data Money Fund Intelligence Daily series (about $400 billion higher than ICI) gave a same-direction but larger read: MMF assets fell a net $49.3 billion across March 2026, the first monthly net decline since April 2025 [100].

If this inflection persists, it will trigger the MMF-scale condition listed under this part's "signals we are watching." For now we keep analytical discipline: a single week or month is not enough to confirm a structural weakening of the siphon — short-term MMF swings can reflect tax-season flows (April is the U.S. individual-tax deadline, historically a period of seasonal MMF drawdown) as much as a rebound in risk appetite or a repricing of rate expectations. Bitbase Research will track this on a rolling four-week average and a seasonally adjusted basis in its Q4 2026 tracking report.

This scale is a direct opportunity-cost anchor for the crypto market. For retail and institutional idle capital, MMFs offer roughly 4.0%–4.3% annualized (tracking the funds rate), T+1 liquidity, and near-zero default risk. By contrast, converting fiat to crypto and depositing it on a non-compliant offshore platform adds platform credit risk, withdrawal-delay risk, and regulatory uncertainty on top of market risk. In the zero-rate world of 2020–2021 that opportunity cost was almost nil and the fiat-spillover effect was pronounced; in today's high-rate environment, the MMF siphon is a structural drag on retail fiat entering crypto.

Notably, the siphon is not evenly distributed. It bears hardest on non-compliant offshore platforms that depend on retail fiat deposits, and only weakly on institutional capital routed through the ETF channel — the latter's allocation decisions rest on portfolio optimization, not on comparing yields against idle cash.

1.3 The unsustainability of non-yield collateral models in a high-rate world

The high-rate environment hits the crypto derivatives market not only on the inflow side but, more deeply, on collateral efficiency. The ISDA margin survey offers direct evidence: in traditional derivatives, cash as a share of all collateral fell to 51.3% at the end of 2024, the lowest on record and far below the roughly 80% peak of 2020 [13]. Cash within variation margin (VM) fell from 80.0% in 2020 to 68.3% in 2024, while non-government securities rose to a six-year high of 13.8%.

The logic is clear: when the risk-free rate is above 3.5%, the opportunity cost of posting non-yield-bearing assets as collateral rises sharply. Traditional markets have optimized capital efficiency by increasing the share of government bonds and other securities in their collateral. For crypto derivatives the implication runs deeper — an isolated-margin model that posts BTC or ETH as margin faces growing economic irrationality in a funding-cost environment above 3.5%.

This is the structural driver behind tokenized real-world assets (RWAs). As of early 2026, the on-chain tokenized-Treasury market was about $12 billion [14]. Tokenized Treasuries, as an "on-chain risk-free rate" vehicle, can serve both compliant centralized exchanges (as a margin-enhancement tool) and on-chain native protocols (as yield-bearing collateral). Under the Basel framework, tokenized traditional assets are classified as Group 1a and receive the same capital treatment as their non-tokenized counterparts [15] — a stark contrast with the 1250% risk weight on Group 2b unhedged crypto assets. This part treats tokenized collateral only as an introduction; its scale, issuer landscape, and legal path into the regulated derivatives system are developed in Part 3.

1.4 The institutional channel switch: what ETF inflows really mean

Against the contracting retail-fiat-spillover channel, the institutional-allocation channel is expanding steadily. As of April 2026, U.S. spot Bitcoin ETFs held roughly $85–98 billion in total assets — BlackRock's IBIT about $56.3 billion, Ark/21Shares' ARKB about $13.6 billion, Fidelity's FBTC about $12.4 billion [16]. Net inflows on April 6, 2026 reached $471 million, a six-week high [17]. Spot Ethereum ETFs held roughly $10–13 billion, materially smaller than Bitcoin ETFs, reflecting the layered nature of institutional allocation preferences.

An honest caveat: institutional allocation is not the same as sustained price appreciation. As of April 8, 2026, Bitcoin traded around $71,906, a market cap of about $1.33 trillion — down roughly $10,600 from a year earlier [18]. The coexistence of ETF net inflows and a falling price is precisely the point of the channel switch: institutions hold crypto exposure on portfolio-allocation logic (an alternative-asset sleeve of, say, under 5%), not on price momentum. That allocation logic is stickier and less leverage-dependent, but it also generates none of the high-frequency retail turnover that non-compliant offshore platforms rely on.

1.5 Core conclusion: the asymmetric impact of the liquidity-channel shift

The shift in the macro-liquidity channel affects the three layers asymmetrically. For non-compliant offshore architecture, the drying-up of retail fiat spillover, the MMF siphon, and the unsustainability of non-yield collateral models in a high-rate world form a triple structural headwind. For compliant multi-jurisdiction centralized exchanges, the expanding ETF channel, the rise of tokenized-RWA collateral, and improving regulatory certainty are positive supports. For on-chain native protocols, the non-custodial property attracts capital seeking to avoid intermediary risk, while integrating tokenized Treasuries as on-chain collateral lifts protocol-level capital efficiency. The 2025 data — $7.9 trillion in total perpetual-DEX volume, $5.74 trillion in H2, and monthly volume clearing $1 trillion in Q4 [4] — is strong evidence that the on-chain-native track is still in structural expansion.

The repricing of macro liquidity, then, is not "the crypto market losing its water source" but a switch in the inflow channel from indiscriminate flooding to targeted allocation — favoring tracks with compliant infrastructure or cryptographic trust mechanisms, and disadvantaging architectures that depend on regulatory arbitrage and information asymmetry.

The Q1 2026 geopolitical shock and hawkish Fed pivot reinforce this asymmetry from the outside. Higher risk-free-rate expectations raise the carrying cost of non-yield collateral directly, while geopolitical risk-off pushes some capital toward tokenized Treasuries and compliant crypto exposure that offer both yield and a hedge against traditional-finance risk — indirect demand for both main tracks. This exogenous variable does not change the core argument; it turns the dual-track divergence from a "long-wave structural migration" into a "long-wave structural migration accelerated under macro stress" — the thesis is not weakened by the shock but gains an extra layer of stress-test validation.

Signals we are watching (Part 1)

The scale and pace of the Fed's reserve-management purchases: if monthly net T-bill buying persistently exceeds the natural reinvestment of maturing MBS principal, the market may re-characterize it as "quasi-QE." The MMF inflection (early signal partially triggered): both the ICI weekly and Crane daily series show assets rolling off the March 18 peak; a rolling four-week average that stays negative through Q2 2026 after seasonal adjustment would confirm the inflection as structural. Adoption of tokenized Treasuries in exchange margin systems. The durability of BTC spot-ETF net inflows. Whether ON RRP climbs back above $100 billion. The geopolitics-and-energy path.

Part 2 · The true cost of microstructure

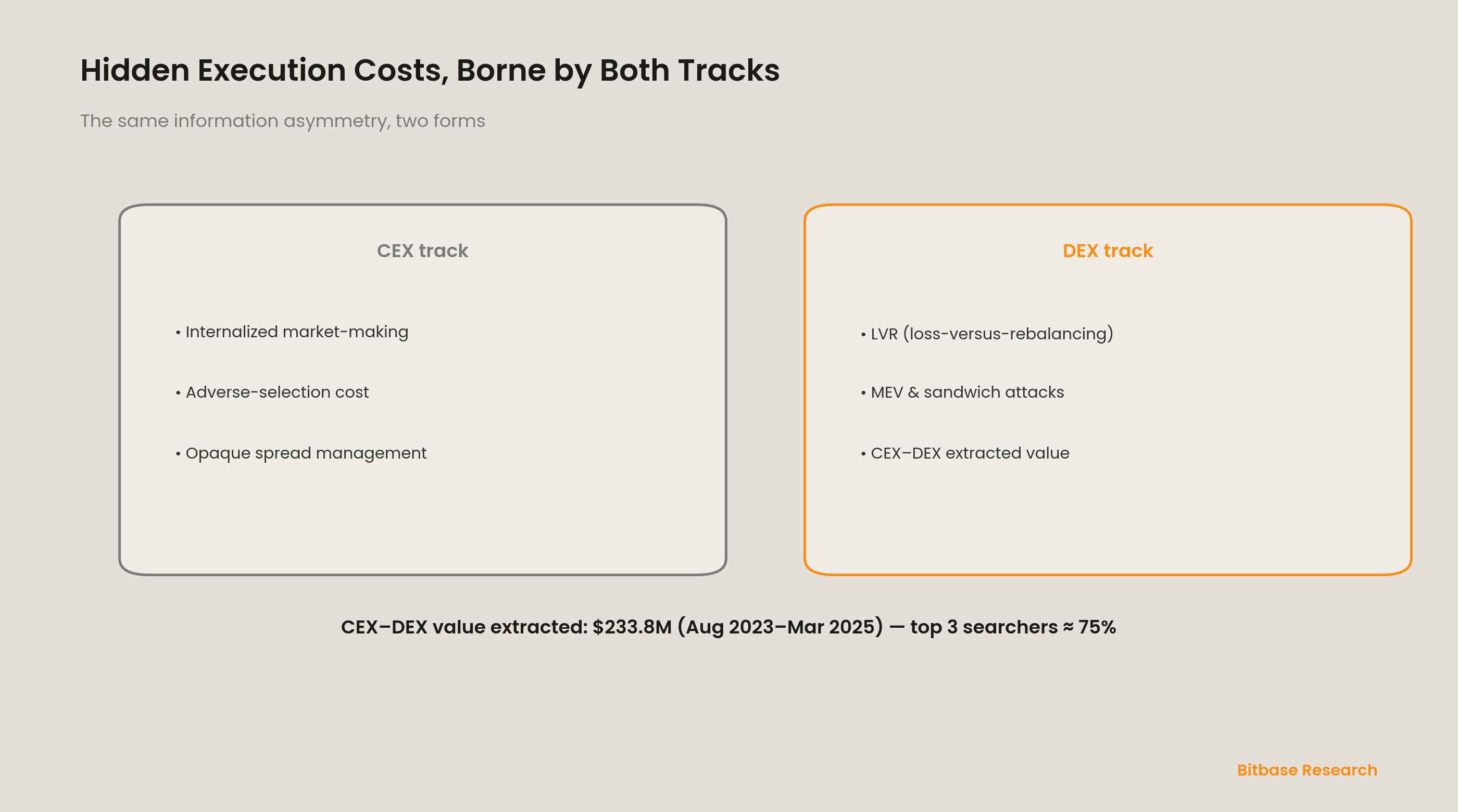

Part 1 argued that the macro-liquidity channel affects the three layers asymmetrically. This part drops from the macro level to the micro level and builds a second shared hard constraint: CEX internalized market-making and DEX LVR/MEV are, at root, the same phenomenon expressed on two different infrastructures — both transfer value from liquidity providers to counterparties with an information advantage. Both tracks pay a hidden cost for execution quality, but in different forms, with different observability, and with different institutional responses.

2.1 Pricing inventory risk in CEX internalized market-making: the Avellaneda–Stoikov frame

The starting point for understanding centralized market-maker behavior is Avellaneda and Stoikov's 2008 paper "High-frequency trading in a limit order book" in *Quantitative Finance* [19], which gives an analytic optimal-quoting solution. Its core mechanism: a market maker's inventory risk grows with the square of volatility. When volatility jumps, market makers systematically widen spreads and pull depth, passing inventory-risk cost onto liquidity takers. In crypto derivatives, some centralized venues play both platform operator and principal market maker — a structural incentive misalignment in which the taker cannot tell whether a widening spread is fair inventory pricing or the extraction of an information advantage. This is not an accusation of active "hunting," which would need trade-by-trade forensics; it is a structural incentive problem. The standard compliant response is organizational separation (matching split from proprietary market-making), disclosure transparency (execution-quality reports), and regulatory constraint (in the spirit of MiFID II best-execution duties).

2.2 VPIN and order-flow toxicity: quantifying information asymmetry

The frontier tool for quantifying order-flow information asymmetry is VPIN (Volume-Synchronized Probability of Informed Trading), from Easley, López de Prado, and O'Hara [20][21]. VPIN buckets order flow in volume time rather than clock time and uses bulk-volume classification to estimate the probability of informed trading in real time; empirically, VPIN climbed sharply in the hours before the May 6, 2010 U.S. equity "flash crash" [20]. Applying it to crypto needs two caveats: its predictive power is academically contested — Andersen and Bondarenko argued VPIN is mechanically tied to trading intensity and not robustly better than conventional volatility measures [22] — and cross-venue information flow (CEX price discovery leading DEX) makes order-flow toxicity more complex, since informed trading may come from arbitrageurs systematically exploiting price lags, not only from fundamentals.

2.3 CEX–DEX extracted value (CEV): the concentration of cross-venue arbitrage

The asymmetry between CEX and DEX is not just theory. Wu, Sui, Thiery, and Pai's 2025 paper "Measuring CEX-DEX Extracted Value and Searcher Profitability" (arXiv:2507.13023, accepted to ACM AFT 2025) offers the most detailed empirical measurement to date [23]. Tracking 19 major CEX–DEX arbitrage searchers over a 19-month window (August 2023–March 2025), it identified 7,203,560 arbitrage trades extracting $233.8 million in total value. The most sobering finding is concentration: just three searchers captured about 75% of the volume and extracted value [23]. CEX–DEX trades were under 2% of block space but produced over 15% of total block value, and the paper documents exclusive searcher–builder relationships in which vertically integrated players earn systematically higher margins.

The implication for the dual-track thesis is twofold. First, the existence and concentration of CEX–DEX arbitrage confirm that cross-venue execution-quality differences are quantifiable and non-trivial — the $233.8 million is, in essence, a hidden cost paid by on-chain liquidity providers to those with a CEX price-information edge. Second, the extreme concentration means that even on "decentralized" infrastructure, value extraction trends toward oligopoly — a mirror image of the concentration problem in CEX internalized market-making.

2.4 The structural cost of LVR for DEX liquidity providers

Inside the on-chain-native track, the structural cost facing AMM liquidity providers is precisely captured by the LVR (Loss-Versus-Rebalancing) framework of Milionis, Moallemi, Roughgarden, and Zhang (arXiv:2208.06046) [24], often called the "Black-Scholes of AMMs." LVR decomposes an AMM LP's loss into market risk (hedgeable) and adverse-selection risk (unhedgeable); by using a rebalancing portfolio as the benchmark, it isolates the loss caused purely by the AMM price lagging the external market — value systematically extracted by informed arbitrageurs. With Ethereum's ~12-second block time, the AMM price is "stale" within every block, and CEX–DEX arbitrageurs harvest that lag deterministically [24]. LVR and the CEV data of section 2.3 paint one picture: on both CEX and DEX, the faster-informed party extracts value from the passive side; the difference is only in form. ESMA's July 2025 report "Maximal Extractable Value" confirmed the phenomenon from a regulatory angle, noting that front-running and sandwich attacks would be illegal in traditional finance and that 85%–95% of Ethereum blocks have used MEV-Boost since November 2022 — proposer-builder separation improved MEV distribution but did not remove MEV itself [25].

2.5 State fragmentation and the physical cost of cross-chain liquidity

The on-chain-native track carries another hidden cost from Layer-2/Layer-3 state fragmentation. L2 DeFi TVL follows a pronounced power law: Base holds about 46.6% of L2 DeFi TVL and Arbitrum about 30.9%, together more than three-quarters, with dozens of other L2/L3 chains sharing the rest [26]. There is irony here: the old narrative that "state fragmentation is the on-chain deadlock" assumed liquidity would scatter disorderly, but liquidity is in fact concentrating rapidly into a few leading L2s — a dual of the volume concentration seen among top centralized venues. This does not mean the cross-chain hidden-cost problem is solved: bridge latency and fees, price differences for the same instrument across chains, and the capital tied up by market makers maintaining inventory on multiple chains remain material frictions for large institutional orders.

2.6 Core conclusion: a shared hidden cost, and the institutional response

Hidden execution-quality cost is shared across both tracks. On the CEX track it shows up as adverse selection in internalized market-making, opaque spread management, and potential incentive misalignment; on the DEX track as LVR, MEV (including cross-domain CEV), and fragmentation friction. The common essence is the monetization of information asymmetry. The rational institutional response is not to flee one track for the other but to build cross-venue execution-quality monitoring: require market-maker disclosure of internalization ratios and adverse-selection metrics, monitor LVR and MEV cost on the DEX side, and deploy smart order routing (SOR) to allocate execution dynamically between CEX and DEX. Institutional competition will ultimately push both tracks toward convergence on execution-quality transparency.

Signals we are watching (Part 2)

Standardized execution-quality reporting by major CEXs. On-chain adoption of LVR-mitigation mechanisms (dynamic fees, oracle-driven pricing such as Uniswap v4 hooks). Penetration of MEV-Share/MEV-Burn-type mechanisms across major L2s. Changes in CEX–DEX searcher concentration (a fall below 50% for the top three would signal a more competitive, user-friendlier structure). The commercialization of institution-grade cross-venue SOR products.

Part 3 · The hard constraint of capital efficiency

Part 2 exposed the hidden execution cost on both tracks. This part argues a second shared hard constraint: capital throughput. With the funds rate held at 3.5%–4%, every dollar of non-yield collateral carries an explicit opportunity cost. Traditional derivatives markets are visibly migrating their collateral structure — cash at record lows, non-government securities at six-year highs. The long-run competitiveness of crypto derivatives infrastructure will hinge on whether one unit of collateral can simultaneously carry risk-exposure hedging and risk-free yield capture. This is an engineering challenge, not the innate advantage of any single architecture.

3.1 Collateral migration in traditional derivatives

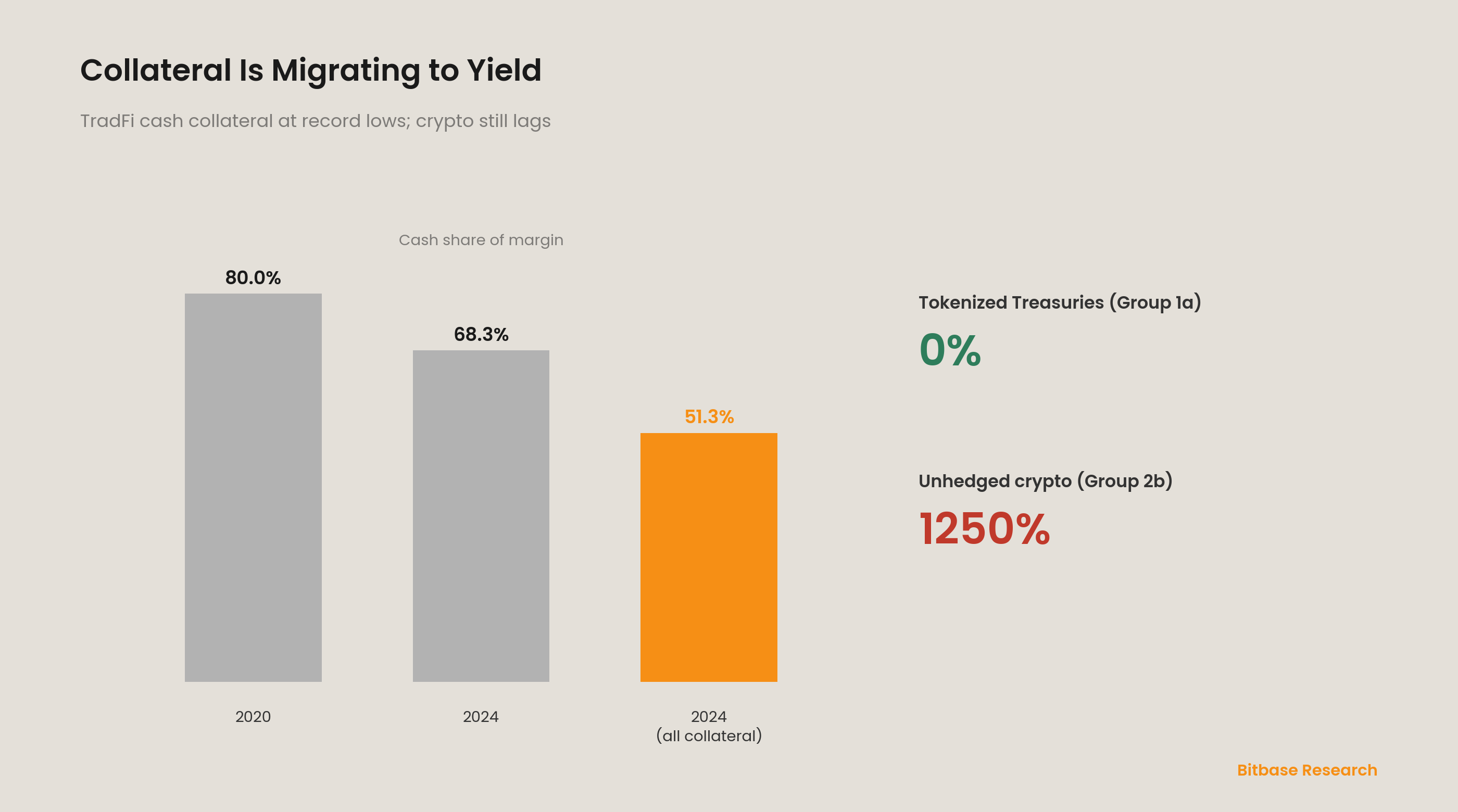

Understanding the crypto capital-efficiency dilemma starts with the traditional market. ISDA's end-2024 margin survey provides a key signal [13]: among 32 top dealers, cash within variation margin fell from an 80.0% peak in 2020 to 68.3%; non-government securities rose to a six-year-high 13.8%; cash across all collected collateral fell to a record-low 51.3%. On the initial-margin side it is more pronounced — government securities 54.5%, other securities 34.7%, cash just 10.7% [13]. Total margin reached $1.5 trillion, up 6.4% year on year [13]. The driver is the phased rollout of Uncleared Margin Rules (UMR); the FSB's December 2024 report on margin-and-collateral-call liquidity preparedness noted that full UMR implementation systematically raised the system's reliance on high-quality collateral [28]. The lesson is clear: collateral portfolios are migrating from cash to yield-bearing assets. With traditional dealers already at 10.7% cash in IM, the crypto market's common demand for full cash margin in non-yield stablecoins like USDT or USDC reveals an obvious efficiency generation gap.

3.2 The structural gap in crypto capital efficiency

The gap first shows up in margin architecture. Isolated margin ring-fences each position's collateral, reducing cascade risk at the cost of capital duplication — three positions lock three separate margins that cannot net. Cross margin shares a collateral pool but adds full-account-liquidation tail risk. Neither is Pareto-optimal; it is an engineering trade-off. Portfolio margin is the real leap: it sizes margin to the portfolio's net risk, recognizing hedges and offering offsets. CME's rates portfolio-margining program saved about $8.4 billion a day in 2025 and first topped $10 billion in early 2026 [30] — but it covers only rates products; CME's crypto futures still margin as standalone products, settled in USD cash, so an arbitrageur cannot post spot BTC against a futures position and must "double-fund" [31]. Within the CFTC perimeter, Bitnomial is a striking counter-example: holding DCM, DCO, and FCM licenses together, in September 2025 it became the first CFTC-regulated exchange to accept BTC and ETH as margin collateral, with cross-product portfolio margin across spot, perps, futures, and options [32].

3.3 Tokenized-RWA collateral: from proof of concept to a regulated channel

As of early April 2026, the tokenized U.S. Treasury market reached about $13 billion [34], nearly 80% growth from about $7.3 billion in mid-2025. The leaderboard shifted decisively in Q1 2026: Circle's USYC (about $2.7 billion) overtook BlackRock's BUIDL (about $2.4 billion) as the largest product, with BUIDL's share down from a ~46% peak in May 2024 to about 18% [35][98]. The real institutional breakthrough came on December 8, 2025, when the CFTC issued three staff letters: 25-39 confirmed technology-neutral treatment and that tokenized Treasuries and MMF shares can serve as regulated margin; 25-40 (reissued as 26-05 in February 2026) allowed FCMs to accept BTC, ETH, and USDC as margin; and 25-41 withdrew the earlier advisory that had limited FCM acceptance of virtual-currency collateral [40][41]. The legal channel and commercial deployment are not simultaneous, but the most milestone case is Circle USYC as off-exchange collateral in Binance institutional derivatives — reaching about $1.84 billion in supply on BNB Chain by March 2026, most of it attributable to that one institutional collateral use case [98]. Notably, Binance is not a CFTC-regulated entity but a diversified venue in international compliant jurisdictions — meaning tokenized-collateral adoption does not require a U.S. license, and other major jurisdictions are advancing the same innovation on their own compliance paths. Under Basel's SCO60 (global implementation January 1, 2026), Group 1a tokenized traditional assets get the same risk weight as their underlying — tokenized Treasuries can carry 0% — while Group 2b unhedged crypto carries 1250%, effectively a full capital deduction [15]. That gap is reshaping the institutional capital-allocation decision tree.

3.4 Capital-efficiency engineering on on-chain native protocols

On-chain protocols are iterating fast on capital efficiency along different paths (described objectively, not as endorsements). Hyperliquid runs on a purpose-built L1 with HyperBFT consensus (~0.2s finality) and in 2026 launched a Portfolio-Margin alpha that unifies spot and perp positions in one account, routing idle assets into a lending pool for yield [43]. Aster embeds yield-bearing assets directly into margin, letting traders post asBNB and USDF as collateral that keeps earning during a trade [44]; note that a Q4-2025 volume spike drew data-integrity scrutiny, and DefiLlama adjusted some of its volume accounting in October 2025 [45]. Lighter, built as an Ethereum zk-rollup by former Citadel engineers, verifies every match and liquidation via zk-SNARK proofs, encoding price-time priority directly in the circuit so the operator cannot reorder trades [46]. Capital-efficiency innovation is not exclusive to on-chain protocols: on February 24, 2026, Kraken — via its Bermuda-BMA-licensed Payward Digital Solutions — launched the first regulated tokenized-equity perpetual futures, offering up to 20x, 24/7, on the xStocks framework to non-U.S. clients across 110+ countries [102]. The xStocks issuer Backed Finance, acquired by Kraken in December 2025, passed $25 billion in cumulative volume within eight months of launch [102]. This carries four implications that map directly onto the report's thesis: the perpetual structure is migrating from the on-chain track into the compliant track and is therefore regulation-neutral; tokenized RWAs can serve as the settlement reference layer; "compliant offshore" and "non-compliant offshore" are empirically distinct (Kraken's Bermuda license places it squarely in Layer 2); and two-way product-structure borrowing between the tracks has moved from theory to deployment.

3.5 Core conclusion: capital efficiency is a shared direction

Capital efficiency is not any single track's exclusive advantage. Compliant multi-jurisdiction CEXs pursue it through regulator-approved tokenized-Treasury margin and cross-product portfolio margin; on-chain protocols through yield-bearing-collateral integration, unified margin accounts, and cryptographically verified risk engines. Both converge on one proposition: collateral yield-ization is redefining what "cost of capital" means. Under the three-layer lens, non-compliant offshore platforms — lacking custody separation, third-party audit, and regulatory infrastructure — cannot offer a credible collateral-yield solution, cannot access Basel Group 1a treatment, and cannot access the CFTC tokenized-collateral channel. That is a structural disadvantage, not a negotiable one. Engineering innovation ultimately needs regulatory confirmation to scale — which is Part 4's subject.

Signals we are watching (Part 3)

Whether CFTC-regulated DCOs formally accept tokenized Treasuries as initial margin in H2 2026. Whether CME's tokenized-cash infrastructure (with Google Cloud) ships on schedule. Whether ISDA's end-2025 survey shows IM cash below 10%. Whether Hyperliquid's portfolio margin moves from alpha to general availability. Whether the Basel Committee responds to industry calls to recalibrate the Group 2b 1250% weight.

Part 4 · A directional re-reading of regulation

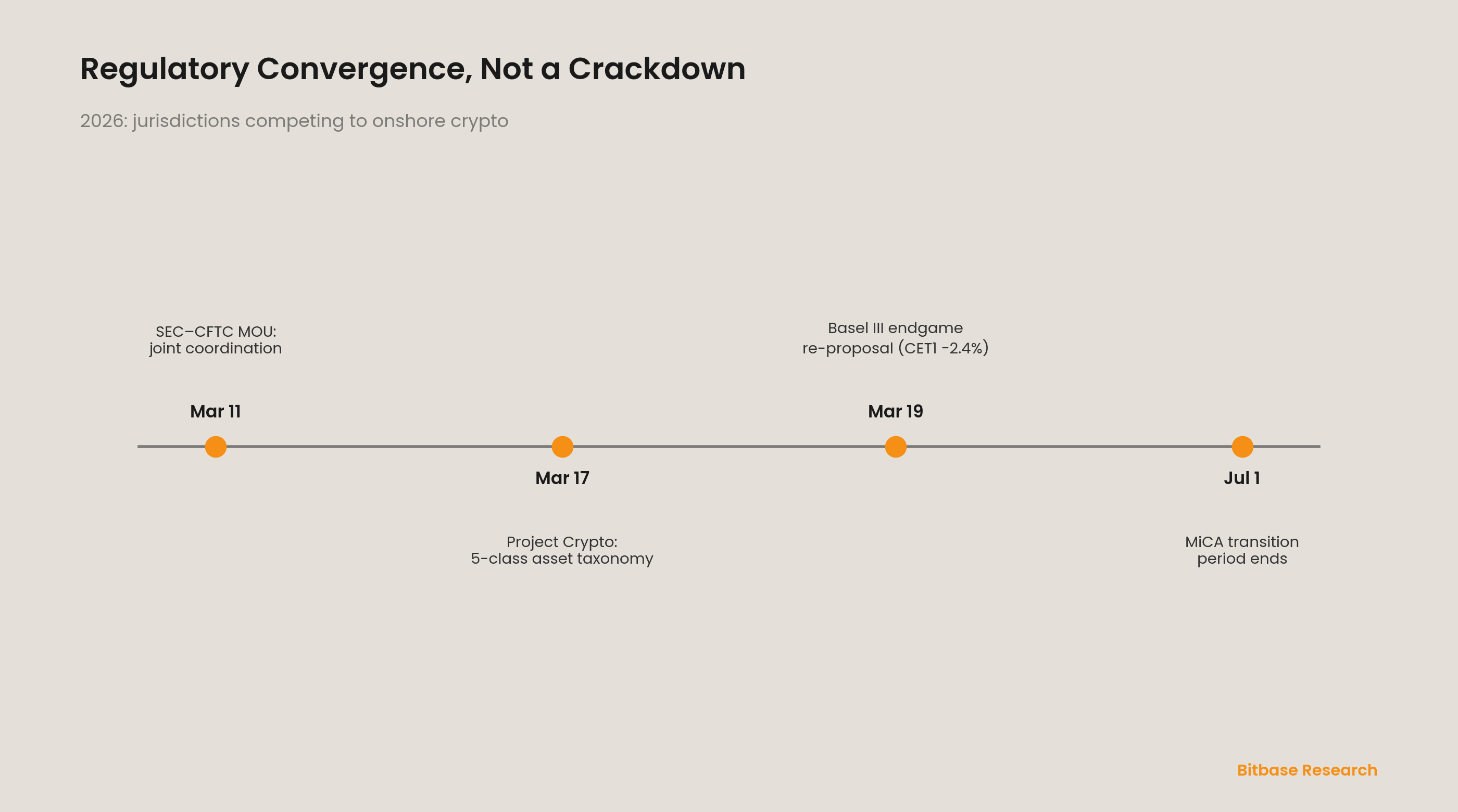

Part 3 argued that capital-efficiency engineering needs regulatory confirmation to reach institutional scale. This part re-reads the 2026 global regulatory landscape directionally: the current wave is not a coordinated crackdown on offshore but an institutional competition in which each jurisdiction is tuning its own rules to attract — not expel — compliant crypto-derivatives business. The U.S. "Project Crypto" guidance is explicit about an onshoring intent; the Basel III endgame re-proposal is net loosening, not tightening; MiCA's uneven transition reflects member-state choices on pace. The biggest loser is not any jurisdiction but the non-compliant architecture still trying to arbitrage regulatory ambiguity.

4.1 The U.S.: from enforcement-led to rulemaking-led

Three documents mark the 2026 U.S. pivot. First, the SEC–CFTC memorandum of understanding of March 11, 2026, establishing a joint coordination initiative across six priority workstreams; SEC Chair Atkins stated plainly that "for decades, regulatory turf battles stifled innovation and pushed market participants to other jurisdictions" [47]. Second, the SEC–CFTC joint interpretive guidance of March 17 (91 Fed. Reg. 13714, 68 pages), which set the five-class asset taxonomy and listed 16 specific assets (BTC, ETH, SOL, XRP, ADA, LINK, AVAX, DOT, and others) as digital commodities; its stated intent is "to keep blockchain innovation in the United States" [1][48]. Third, CFTC Chairman Michael Selig's public commitment to "bring perpetual futures and other novel derivatives back onshore" and to "reclaim liquidity that migrated to Asia, Europe, and the Bahamas" [49][50]. As of this report (April 2026), that perpetuals framework had not been formally published — more than five weeks past Selig's "within a month or so" — a delay that is itself a data point about institutional pace, not a reversal of direction, given the CFTC has only one Senate-confirmed commissioner with four of five seats vacant [103]. The delay is, if anything, positive evidence for the "long-wave cycle, not sudden event" thesis: rulemaking, institutional adaptation, and behavioral change all unfold on a scale of years.

4.2 The EU: MiCA's uneven transition

MiCA's CASP provisions applied from December 30, 2024, with Article 143(3) allowing member states up to an 18-month transition ending July 1, 2026 [51]. Choices diverged sharply: the Netherlands, Poland, Finland, Latvia, Hungary, and Slovenia took the shortest (6-month) transition, ending mid-2025; Germany, Austria, and Ireland took 12 months; Spain and Italy initially chose 12 then extended to 18 [3][52]. By December 2025, ESMA's interim register listed about 103 fully authorized CASPs — Germany's BaFin leading with 27 licenses, France's AMF 10, Austria 6 [53] — reflecting the first-mover advantage of shorter-transition jurisdictions. MiCA Article 61's reverse-solicitation carve-out is narrow: a third-country CASP may serve EU clients only where the client initiates entirely on their own exclusive initiative, and ESMA's February 2025 guidelines read "solicitation" broadly [54].

4.3 The Basel framework: the real direction of the endgame re-proposal

Two distinct legal events must not be conflated. First, the BCBS SCO60 standard (issued December 2022, global implementation January 1, 2026), which set the four-group classification and capital treatment: Group 1a (tokenized traditional assets, same weight as the underlying), Group 1b (qualifying stablecoins), Group 2a (hedgeable crypto), Group 2b (other crypto, 1250% weight, no hedge recognition); a 1250% weight is mathematically equivalent to a full capital deduction [15][55]. Second, the U.S. Basel III endgame re-proposal of March 19, 2026 by the Fed, FDIC, and OCC, which repealed the 2023 version; its overall direction is loosening. Per the Bank Policy Institute, the three proposals together cut Category I and II banks' CET1 requirement by about 2.4% net [2]. The "1250% mistake" debate is live: the Bitcoin Policy Institute argues the 1250% weight, designed for opaque securitization tranches, is a category error when applied to a transparent, globally traded, zero-counterparty-risk asset [55], and GFMA and ISDA jointly urged the BCBS to delay and recalibrate [57]. The 1250% weight is not a new 2026 U.S. invention but the 2026 global implementation of the 2022 BCBS standard — early narratives calling Basel a "capital guillotine" run against the actual policy direction.

4.4 The institutional competition among financial centers

Multiple centers are building crypto-derivatives frameworks along their own paths, together forming the institutional base of the compliant-centralized track. Switzerland leads with a technology-neutral, modular approach (the 2021 DLT Act; FINMA's first DLT-trading-facility license to BX Digital in March 2025) [59]. The UAE runs parallel federal and emirate regimes (ADGM's FSRA framework from 2018; Dubai's VARA) [60]. Singapore licenses digital-payment-token services under the 2019 PSA (33 licensees by 2025) and runs Project Guardian with 40+ global institutions [61]. The UK enacted its FSMA crypto regime in February 2026, with the full framework expected October 2027 [62]. Hong Kong's SFC VASP regime has been mandatory since June 2023 (9 licensees by February 2025), and its Stablecoins Ordinance took effect August 2025 [63]. Japan's FSA oversees 32 registered providers and in December 2025 proposed reclassifying crypto from the Payment Services Act to the Financial Instruments and Exchange Act [64]. These jurisdictions are not opponents of U.S. Project Crypto but participants in the same competition, differing on implementation path rather than on the basic philosophy of bringing crypto derivatives inside a regulatory framework.

4.5 The FSB and IOSCO global coordination frame

Beneath the multi-jurisdiction competition sits a consolidating global consensus. The FSB's July 2023 high-level recommendations (nine for crypto-asset activities, plus revised global-stablecoin recommendations) rest on "same activity, same risk, same regulation" [65]; IOSCO's November 2023 18 policy recommendations (IOSCOPD734) cover conflicts of interest, market abuse, cross-border cooperation, custody, operational risk, and retail access [66]. The October 16, 2025 thematic reviews from both bodies confirmed the key fact: the global direction is settled, but implementation depth and speed differ markedly across jurisdictions — the essence of institutional competition [67][68].

4.6 Core conclusion: the net effect of regulatory convergence

Three directional conclusions. First, convergence is not "the world against crypto" but "the world reaching directional consensus on how to regulate crypto" — the U.S. and Basel directions are loosening and onshoring, not tightening and expulsion. Second, the biggest loser is non-compliant offshore architecture, whose arbitrage of ambiguity is being systematically removed. Third, both main tracks adapt in different ways — compliant CEXs by acquiring licenses, on-chain protocols via protocol-level compliance modularity (KYC integration, geo-fencing, reporting interfaces). Regulatory frameworks solve "legitimacy"; trust minimization is a separate engineering problem — the subject of Part 5.

Signals we are watching (Part 4)

The actual arrival of the CFTC perpetuals framework (tracking node updated to end-Q3 2026). The real exit/conversion rate of third-country CASPs after the July 1 MiCA cliff. Whether the Basel endgame comment period produces large-scale industry opposition to the 1250% weight. The volume and pace of UK FCA applications (window opens September 30, 2026). Whether the FSB/IOSCO launch a second review or DeFi-specific guidance.

Part 5 · The migration of the trust paradigm

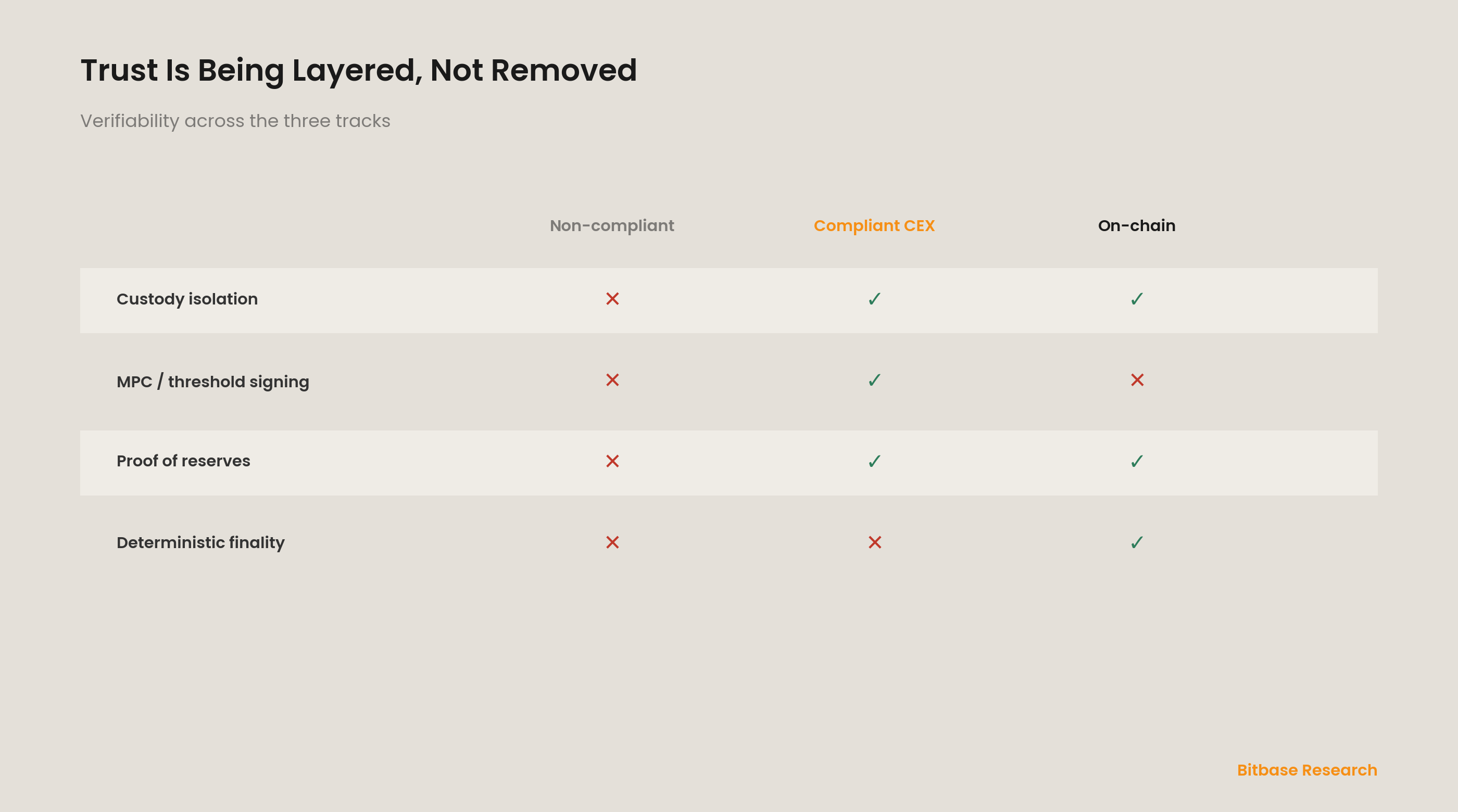

Part 4 covered "legitimacy." But legitimacy is not trustworthiness. This part focuses on a separate proposition: crypto derivatives infrastructure is undergoing a structural migration of its trust anchor — from "reliance on a single centralized entity's reputation and legal promises" to a layered defense-in-depth of "verifiable cryptographic proof plus independent custody plus deterministic settlement finality." This is not the elimination of trust but trust minimization — decomposing assumptions once concentrated in one entity into multiple independent, auditable, falsifiable components.

5.1 The evolution of the trust anchor: from legal promise to verifiable computation

The 2022–2024 collapses of several large centralized crypto institutions were, at core, single-point governance-trust failures: commingled client and proprietary funds, undisclosed liabilities, missing or misleading proof of reserves. Frequent commercial audits and legal promises did not prevent material misappropriation, because audits themselves depend on the integrity of information provided by the audited party. Institutional risk management shifted its base logic from "assume the counterparty will not misbehave" to "make it physically hard for the counterparty to misbehave" — via independent custody, multi-party key management, verifiable computation, and deterministic settlement. The CPMI-IOSCO PFMI Principle 8 anchors settlement finality as a legal concept requiring a clear legal basis, not just technical irreversibility [69] — a dimension the trust migration must also answer.

5.2 MPC and threshold signatures in institutional custody

Multi-party computation (MPC) and threshold signature schemes (TSS) are now mainstream in institutional custody: private-key generation, storage, and use are split across independent parties so no single party can reconstruct the full key. The market is multipolar — Fireblocks (MPC-CMP), BitGo (multisig + MPC, NYDFS and BaFin licensed), Anchorage (the first OCC-chartered crypto bank), Copper (ClearLoop off-venue settlement), Zodia (Standard Chartered/Northern Trust), Sygnum (Swiss FINMA banking license), and Taurus (State Street partnership) [70][71]. MPC/TSS is not a panacea: in 2023, Verichains disclosed the TSSHOCK attacks against GG18/GG20 threshold-ECDSA implementations, and Fireblocks independently found a Paillier key-verification gap (CVE-2023-33241) allowing full-key extraction in as few as 16 signatures; in 2024, Trail of Bits disclosed threshold-raising flaws in Pedersen DKG affecting FROST, GG18/GG20, and a dozen more implementations [72][73][74]. The takeaway is not "MPC is unusable" but that there is a persistent gap between cryptographic theory and production code — independent, repeated cryptographic audit is a necessary condition for MPC custody security, not a one-time compliance box.

5.3 The TEE debate and defense-in-depth

Trusted execution environments (TEEs) — Intel SGX/TDX, AMD SEV/SEV-SNP — are widely used for compute isolation and remote attestation, but a 2024–2026 stream of research shows they are empirically fragile as a sole root of trust: TDXDown (CCS 2024) recovered ECDSA keys from Intel TDX; WireTap (CCS 2025) extracted DCAP attestation keys from SGX using ~$1,000 of passive DDR4 probing hardware, with end-to-end attacks demonstrated on live deployments; Battering RAM (IEEE S&P 2026) used a $50 DDR4 interposer to bypass boot-time checks on both Intel and AMD; and CacheWarp (USENIX 2024) recovered an RSA key from AMD SEV-SNP in six seconds [75][76][77][78]. The conclusion is not "TEE is unusable" but "TEE as the only root of trust is fragile; TEE as one layer of defense-in-depth is reasonable" — the Confidential Computing Consortium recommends exactly this multi-dimensional posture [80].

5.4 Settlement finality: a two-layer read of the technical and the legal

Settlement finality has two related but distinct dimensions. Technical finality is protocol-level irreversibility; legal finality is irrevocable, unconditional legal effect under applicable law, even in a participant's bankruptcy. Proof-of-work systems provide probabilistic finality — reversal probability decays exponentially with confirmations but never reaches zero, as BIS Working Paper 44 notes [81] — while classical BFT protocols (Tendermint/CometBFT, HotStuff) provide deterministic finality mappable to the legal requirement. On the legal side, multiple jurisdictions are building the basis for tokenized-asset transfer: UNCITRAL's MLETR (adopted by 13 jurisdictions including Singapore, the UK, and France) [83]; the U.S. UCC Article 12 (2022), creating "controllable electronic records," adopted by 33 states plus D.C. by end-2025 including New York [84]; the UK's Electronic Trade Documents Act 2023 [85]; and the EU's DLT Pilot, which ESMA recommended making permanent, with the Commission proposing to raise the issuance cap to €100 billion [86]. The differences show a globally unified legal regime does not yet exist — jurisdiction-by-jurisdiction assessment of legal finality remains necessary for cross-border clearing entities.

5.5 The state and limits of proof of reserves

Proof of reserves (PoR) has become a core trust-recovery mechanism, but its limits must be understood. Merkle-tree PoR (Greg Maxwell, 2014) lets users verify their balance is included in claimed reserves, but it only proves "assets exist," not "assets exceed liabilities" or "assets are not rehypothecated"; it is a point-in-time snapshot, excludes off-chain liabilities, and depends on auditor trust [87]. Full solvency verification needs proof of reserves plus proof of liabilities. More advanced zero-knowledge PoR is developing — the Provisions protocol (Dagher et al., ACM CCS 2015) [88], IZPR (2023) with O(n·log n) proving and O(1) verification and 3.4KB proofs [89], and Xiezhi (2024) toward end-to-end succinct solvency [90] — and some venues have deployed zk-SNARK-based PoR, but these are not yet an industry standard. PoR should be positioned as "necessary but not sufficient" trust infrastructure; even the best zk-PoR cannot catch enterprise-level fraud hidden at the legal-entity layer.

5.6 Conclusion: layered trust, not the elimination of trust

The trust migration is not "trustlessness" but "layered trust." Non-compliant offshore architecture bears the most structural pressure because it lacks verifiability at every layer — no custody isolation, no proof of reserves, no independent audit, no deterministic-finality proof — and still relies entirely on a single operator's reputational promise, which 2022–2024 systematically discredited. The compliant-centralized and on-chain-native tracks achieve layered trust differently — the former via institutional MPC custody, regulated custodian banks, third-party audit, and PoR; the latter via non-custodial protocols, on-chain transparency, cryptographic proof, and open-source audit — but they converge on the same direction of trust decomposition.

Signals we are watching (Part 5)

Whether MPC custodians publish independently audited TSS security assessments. Whether major compliant venues add zk-based PoR with a liabilities component. Whether CPMI-IOSCO issue DLT finality guidance. Whether Intel/AMD add non-deterministic memory encryption in next-gen TEEs. Whether U.S. UCC Article 12 adoption passes 40 states before 2027.

Part 6 · The dual-track endgame

Part 5 argued that layered trust is the shared evolution of both tracks. This part pushes to the endgame: across 2026–2030, crypto derivatives infrastructure evolves into a dual-track, long-wave equilibrium. Compliant multi-jurisdiction clearing entities and on-chain native protocols are not zero-sum competitors but complementary infrastructures serving different institutional preferences, risk tolerances, and compliance needs. Non-compliant offshore architecture faces joint erosion from both tracks, but the process is gradual, regionally uneven, and measured in years.

6.1 Dual-track is functional differentiation, not binary opposition

The compliant-centralized track's value proposition is regulatory certainty, institutional-grade risk management, tokenized-RWA collateral integration, and TradFi interoperability; the on-chain-native track's is non-custodial access, borderless reach, composability, and censorship resistance. Their customer profiles differ — regulated asset managers, pensions, insurers, and bank desks bound by fiduciary duty on one side; crypto-native funds, quant teams, and global retail on the other. The analogy to exchange-traded vs OTC derivatives, which have coexisted in traditional finance for decades, is the key anchor against a "single winner" narrative.

6.2 Re-reading the 2025 perpetual-DEX data

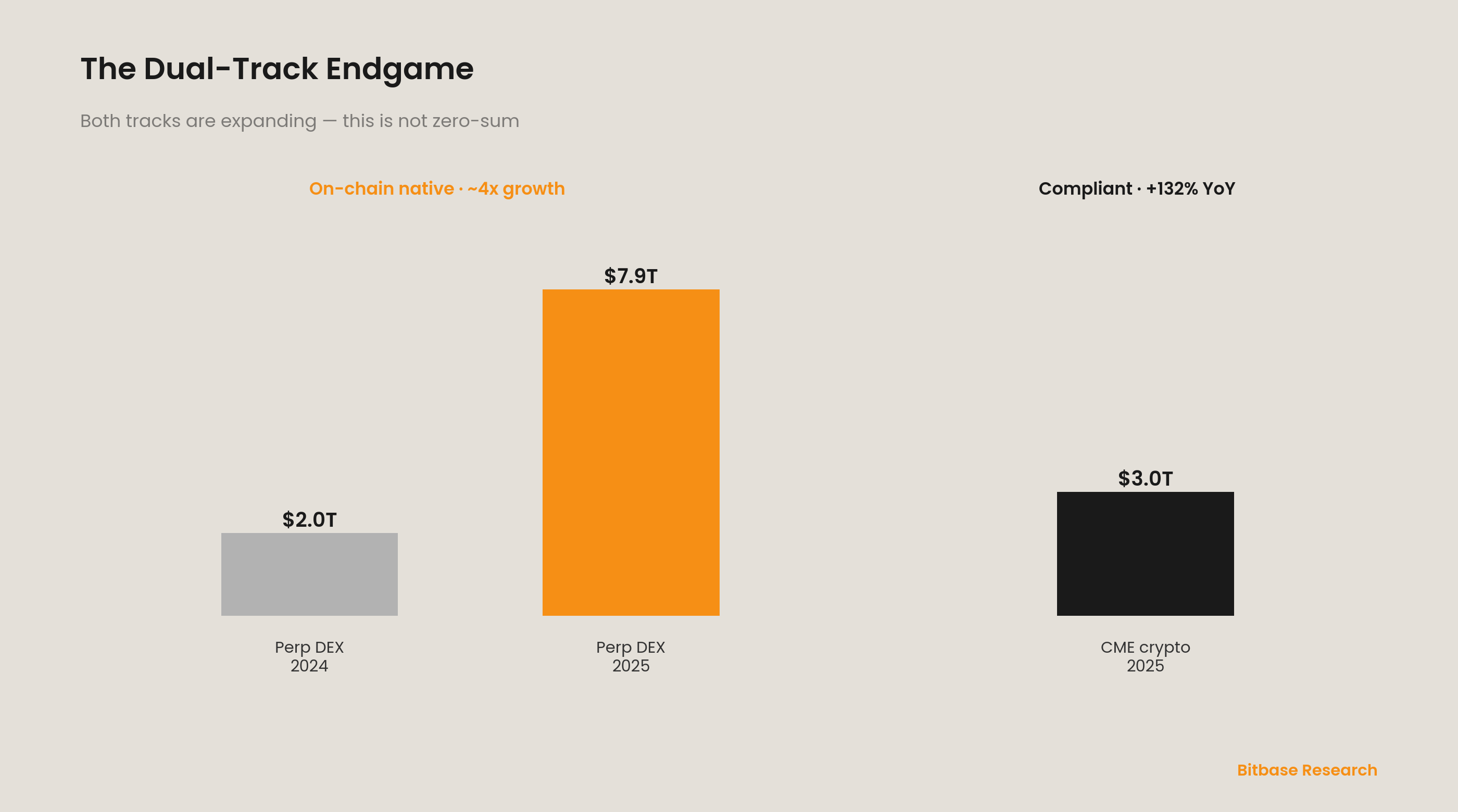

2025 was the on-chain track's structural breakout. Per DefiLlama, perpetual-DEX volume hit $7.9 trillion for the year, about 65% of the all-time cumulative total; H2 contributed $5.74 trillion (73%), and Q4 monthly volume cleared $1 trillion, peaking near $1.36 trillion in October [4][91]. The competitive structure re-converged in Q1 2026: Hyperliquid's volume share climbed from ~36.4% in January to ~44% in March, and it controls ~70% of open interest (~$5.15 billion), far ahead of Aster [104][105]. A new four-pole structure (Hyperliquid, Aster, Lighter, edgeX — the last building ~26.6% share on a StarkWare stack) is itself a sign of maturity, echoing the multi-venue coexistence of CME, ICE, Eurex, and HKEX in traditional finance [104]. The near-fourfold jump from about $2 trillion in 2024 reflects compounding gains in infrastructure maturity, market-maker depth, and execution quality — not a last gasp.

6.3 Growth on the compliant-centralized track

The compliant track grew just as strongly in the same period — dual-track divergence is two tracks expanding together, not one consuming the other. CME's 2025 crypto notional hit $3 trillion, average daily volume 270,900 contracts (~$12 billion notional), up 132% year on year; open interest rose 82% to 299,700 contracts (~$26.6 billion), setting a $39 billion record on September 18, 2025, with large open-interest holders passing 1,014 [93][94]. Coinbase Derivatives launched CFTC-regulated BTC/ETH nano futures in July 2025; Bitnomial became the first CFTC-approved venue to accept digital-asset margin; Cboe announced ten-year "continuous futures" approximating perpetuals [95][32][96]. On the ETF side, U.S. spot Bitcoin ETFs passed $65 billion in cumulative net inflows by early April 2026, with 2025 crypto-ETF inflows about $34.1 billion; BlackRock IBIT alone drew $25.1 billion in 2025, sixth among all U.S. ETFs [97]. Morgan Stanley launched its own MSBT spot Bitcoin ETF (14bps) on April 8, 2026 — a top U.S. wealth manager entering the market even with BTC down ~20% year-to-date signals a long-horizon allocation view [107].

6.4 Early signals of cross-track interoperability

Interoperability has left the concept stage. First, compliant CEXs adopting on-chain-native product structures: Kraken's xStocks perpetuals (Bermuda-licensed, $25 billion cumulative volume) wrap a DEX-native structure inside a compliant frame with tokenized equities as the reference layer [102]. Second, on-chain protocols carrying regulated RWA derivatives: Hyperliquid's HIP-3 framework already supports crude-oil and silver 24/7 perpetuals — a structural mirror image of Kraken [104]. Third, on-chain-native tokens entering the regulated ETF channel: Grayscale filed an S-1 for a spot HYPE ETF (GHYP) on March 20, 2026 [104]. Fourth, tokenized RWAs as shared collateral across both tracks: Circle USYC as off-exchange collateral on Binance (~$1.84 billion), plus the CFTC's tokenized-collateral letters and CME's tokenized-cash roadmap, make a tokenized Treasury a genuinely cross-track-neutral base layer [98][40][42]. Fifth, persistent basis and cross-track arbitrage economics between CME futures and on-chain perps.

6.5 The structural pressure on non-compliant offshore architecture

The first five parts establish five long-wave pressures on non-compliant offshore architecture: the liquidity-channel switch (Part 1); microstructure-transparency demands (Part 2); the capital-efficiency hard constraint (Part 3); regulatory convergence and enforcement coordination (Part 4); and layered-trust requirements (Part 5). None is a "sudden event"; all are "long-wave migration" — the essence of the report's difference from a "violent break" narrative. Non-compliant share will be eroded gradually and unevenly by region — migration in parts of Southeast Asia, the Middle East, and Africa may run materially slower than in North America and the EU — on a multi-year time scale.

6.6 Toward the conclusion: what this means for participants

An outline the conclusion develops: allocators must redefine "execution benchmark" and "collateral-efficiency assessment"; brokers must upgrade from "single-venue access" to "cross-track best-execution routing"; quant funds will find structural alpha in cross-track basis and liquidity differences; crypto-native projects must choose clearly between the compliant path and the on-chain-native path.

6.7 Where we might be wrong: a reflexive stress test

Any serious framework must stress-test its own hypothesis. Scenario one: a 180-degree regulatory reversal (e.g., a 2028 U.S. election unwinding the SEC/CFTC jurisdiction split) would weaken the compliant track's certainty premium — but the technical logic of the dual track (trust layering, capital efficiency, execution quality) runs independent of the regulatory cycle, so the structure would adjust, not dissolve. Scenario two: a Fed leadership change producing policy discontinuity — Chair Powell's term ends May 2026 amid a DOJ investigation — could reshape Part 1's macro-liquidity structure; a more dovish path would slow the divergence, a more hawkish one accelerate it, with policy continuity the base case. Scenario three: a major breakthrough in general quantum computing threatening current elliptic-curve cryptography before 2030 would force a multi-year migration to post-quantum schemes (NIST published FIPS 203/204/205 in 2024) [99]. Scenario four: a major systemic failure of a leading perpetual-DEX (contract bug, oracle manipulation, governance attack) could temporarily revert to a compliant-centralized-dominant structure. These scenarios do not negate the thesis; they show its reflexive self-awareness — a falsifiable long-horizon call is a mark of rigor, not a flaw.

Signals we are watching (Part 6)

Whether CME crypto OI holds above $30 billion through 2027. Whether annual perpetual-DEX volume stays above $5 trillion in 2026. Whether the CFTC approves more licensed perpetuals-style products before 2027. Whether the tokenized-Treasury market passes $25 billion before 2027. Whether a compliant clearing entity prototypes on-chain/traditional settlement interoperability. Whether non-compliant offshore's global OI share falls more than 15 points from its 2024 peak by end-2027. Whether post-quantum cryptography enters any major Layer-1 upgrade roadmap.

Conclusion

Structural divergence within a long-wave cycle

From macro-liquidity repricing, through true microstructure costs, capital-efficiency constraints, a directional re-reading of regulation, and the migration of the trust paradigm, to the dual-track endgame, the six parts form one progressive argument: crypto derivatives infrastructure is entering a multi-year structural-divergence long-wave cycle (2026–2030), not the violent break of common market narratives. The two main tracks — compliant multi-jurisdiction clearing entities and on-chain native protocols — each hold an irreplaceable functional position on trust mechanism, customer profile, and value proposition, forming a complementary infrastructure landscape. What is culled is not "offshore" itself but non-compliant offshore architecture: no KYC/AML, no third-party audit, no proof of reserves, B-book internalization, no custody/matching separation.

The driver is not a single regulatory event or technical breakthrough but a long-wave resonance across five dimensions — macro liquidity, microstructure, capital efficiency, regulatory evolution, and the trust paradigm — none of which is a "sudden event." Non-compliant offshore share will be eroded gradually across 2026–2030, unevenly by region, gated by local enforcement resources, financial-infrastructure maturity, and user education.

An action framework

For allocators: build a cross-track execution benchmark and collateral-efficiency assessment, fold the on-chain track's capital efficiency into portfolio optimization, and monitor the CME-OI-to-DEX-OI ratio as a leading indicator of institutional preference. For brokers: build execution capability on both tracks and shift core competitiveness from "single-venue access" to "cross-track best-execution routing and a unified risk view." For quant funds: harvest structural alpha from cross-track basis, volatility-surface differences, and settlement-timing gaps — alpha whose durability depends on how fast cross-track infrastructure matures. For crypto-native projects: choose clearly between the compliant path (institutional access at the cost of licensing and longer market-entry) and the on-chain-native path (decentralization and fast iteration, but limited large-institution access) — trying to do both usually means competitive depth on neither.

A methodological commitment

Every core thesis carries falsifiable conditions; the per-part "signals we are watching" form a structured hypothesis-test checklist observable over 6–24 months. Bitbase Research commits to a first "signal tracking" supplement in Q4 2026 — testing divergence speed, non-compliant share change, cross-track interoperability, and trust-infrastructure evolution. Exposing forecasts to empirical test is how a research practice builds long-run credibility, and the mark that separates this report from marketing narrative.

Bitbase's position

Based on the first five parts — the structural preference of the liquidity channel for compliant rails, institutional demand for deterministic settlement and auditable risk management, and the foundational requirement of layered trust for independent custody and proof of reserves — Bitbase treats compliant multi-jurisdiction centralization as its main track, an engineering judgment about the direction of structural evolution. Bitbase has chosen not to build a perpetual-DEX protocol nor a traditional all-in-one platform, but to position itself as an infrastructure builder on the compliant track: institutional-grade independent custody and multi-party key management; regular proof-of-reserves disclosure evolving toward fuller solvency proof; SOC 2-level controls and independent third-party audit; and compliance across multiple major jurisdictions. Current operations cover spot and perpetual trading. As an exchange built from scratch, Bitbase carries no legacy technical debt — a structural advantage that lets it encode trust layering, collateral yield-ization, and cross-track interoperability directly into its system design.

Methodology disclosure

This is Bitbase Research's first publication, and we aim to set our practice at an institutional transparency standard. Tools and generation assistance: advanced large language models were used as research aids in data gathering, cross-source fact-checking, structured argumentation, and drafting; all primary data, regulatory documents, academic papers, and market indicators were verified item by item against original sources, and all formulas, cryptographic details, and legal citations were human-reviewed. We acknowledge AI tools carry inherent error risk in long-tail data handling, reduced but not eliminated by multiple fact-checking rounds. Scope and limits: this report focuses on the structural evolution of crypto derivatives infrastructure — not price prediction, trading advice, or token fundamentals; the analytical frameworks (three-layer taxonomy, capital turnover, trust layering) are research constructs, not official definitions. Data timeliness: all cited macro, regulatory, and market data are as of April 9, 2026; high-frequency metrics can shift materially within days of publication. Research independence: the analysis rests on public primary sources and the team's independent judgment; all named entities (CME, Coinbase, Bitnomial, Hyperliquid, Aster, Lighter, Fireblocks, BitGo, and others) are cited as objective descriptions of the landscape, not as recommendations or endorsements. This is not investment advice, and reading it creates no fiduciary or advisory relationship. Forward-looking statements about the "dual-track endgame" are theoretical hypotheses subject to geopolitical, regulatory, or technological disruption; the per-part signals and the section 6.7 stress test are their built-in falsifiable conditions. Bitbase Research welcomes corrections and critique through public channels.

References

Regulatory and policy documents

[1] U.S. Securities and Exchange Commission & Commodity Futures Trading Commission, “Application of the Federal Securities Laws to Certain Types of Crypto Assets and Certain Transactions Involving Crypto Assets,” Interpretive Release, 91 Fed. Reg. 13714, March 23, 2026. govinfo.gov

[2] Bank Policy Institute, “BPInsights: March 21, 2026,” March 21, 2026. bpi.com

[3] European Securities and Markets Authority, “List of MiCA Grandfathering Periods Decided by Member States Under MiCA (Art. 143(3)),” December 2024 (updated December 2025). esma.europa.eu

[15] Basel Committee on Banking Supervision, “Prudential Treatment of Cryptoasset Exposures (SCO60),” December 2022, revised July 2024, global implementation January 1, 2026. bis.org

[40] Commodity Futures Trading Commission, Press Release №9146–25, “Acting Chairman Pham Announces Launch of Digital Assets Pilot Program for Tokenized Collateral in Derivatives Markets,” Staff Letters №25–39, 25–40, 25–41, December 8, 2025. cftc.gov

[41] Commodity Futures Trading Commission, Press Release №9180–26, “CFTC Staff Reissues Letter 25–40 Updating Payment Stablecoin Definition” (Letter 26–05), February 2026. cftc.gov

[47] U.S. Securities and Exchange Commission, “SEC and CFTC Announce Historic Memorandum of Understanding Between Agencies,” Press Release 2026–26, March 11, 2026. sec.gov

[48] Patomak Global Partners, “Classification of Crypto Assets Under Federal Securities Laws,” March 25, 2026. patomak.com

[49] Commodity Futures Trading Commission, Chairman Michael Selig, Inaugural Remarks, January 29, 2026. cftc.gov

[50] Bloomberg, “US Crypto-Linked Perpetual Futures Coming Soon, CFTC Chair Says,” March 3, 2026; CoinDesk, “CFTC Chief Selig to Clear Path for U.S. Perpetual Futures,” March 3, 2026.

[51] Regulation (EU) 2023/1114 of the European Parliament and of the Council on Markets in Crypto-Assets (MiCA), Article 143(3).

[52] Freshfields, “Grandfathering Under MiCA: How Member States Approach the Transitional Regime,” December 2024, updated December 2025; Latham & Watkins, “MiCA Cliff-Edge Risk in Spain Mitigated as ESMA Updates List of Grandfathering Periods,” December 2025.

[53] Compliance Corylated, “As MiCA Turns One: Member States Take Divergent Approach to Implementation,” December 2025.

[54] European Securities and Markets Authority, “Guidelines on Reverse Solicitation Under MiCA (ESMA35–1872330276–2030),” February 26, 2025. esma.europa.eu

[55] Conner Brown, Bitcoin Policy Institute, “Basel’s 1250% Mistake,” February 23, 2026. btcpolicy.org

[56] Mayer Brown, “US Banking Regulators Propose Reforms to Capital Requirements,” March 2026. mayerbrown.com

[57] Global Financial Markets Association and ISDA, “Joint Letter to BCBS on Recalibration of Cryptoasset Prudential Standards,” August 2025. gfma.org

[58] Michelle W. Bowman, “Basel III and Bank Capital Rules,” Speech at Cato Institute Policy Forum, March 12, 2026. bis.org

[59] Swiss Financial Market Supervisory Authority (FINMA), “First DLT Trading Facility Licensed,” Press Release, March 18, 2025. finma.ch

[60] Abu Dhabi Global Market, “ADGM FSRA Presents Key Enhancements to Digital Assets Framework,” November 2025; DLA Piper, “The UAE: Cryptocurrency and Digital Asset Regulation Series,” 2025.

[61] Monetary Authority of Singapore, “MAS Clarifies Regulatory Regime for Digital Token Service Providers,” Media Release, June 6, 2025. mas.gov.sg

[62] UK Financial Conduct Authority, “New Regime for Cryptoasset Regulation: Roadmap,” 2026. https://www.fca.org.uk/firms/new-regime-cryptoasset-regulation; Sidley Austin, “UK Cryptoasset Regulation: Action Points for 2026–2027,” January 2026.

[63] Hong Kong Securities and Futures Commission / Financial Services and the Treasury Bureau, “LEAP Framework for Digital Asset Leadership,” June 2025; CoinDesk, “Hong Kong Regulators Target 2026 Legislation for Virtual Asset Dealer and Custodian Rules,” December 25, 2025.

[64] Japan Financial Services Agency, “Review of Systems Related to Crypto-Assets,” Discussion Paper, April 2025. fsa.go.jp

[65] Financial Stability Board, “High-level Recommendations for the Regulation, Supervision and Oversight of Crypto-asset Activities and Markets: Final Report,” July 17, 2023. fsb.org

[66] International Organization of Securities Commissions, “Policy Recommendations for Crypto and Digital Asset Markets (IOSCOPD734),” November 2023. iosco.org

[67] Financial Stability Board, “Thematic Review on FSB Global Regulatory Framework for Crypto-asset Activities,” October 16, 2025. fsb.org

[68] International Organization of Securities Commissions, “Thematic Review Assessing the Implementation of IOSCO Crypto and Digital Asset Recommendations (IOSCOPD801),” October 16, 2025. iosco.org

[103] CoinDesk, “CFTC Chief Selig to Clear Path for U.S. Perpetual Futures in Coming Weeks,” March 3, 2026; Cryptonomist, “Crypto perpetual futures rules near rollout by CFTC,” March 4, 2026; The Coin Republic, “US Crypto Regulation: CFTC Eyes Revival of Perpetual Futures Trading,” March 26, 2026. coindesk.com

Central-bank and macroeconomic sources

[5] Board of Governors of the Federal Reserve System, “Federal Reserve Issues FOMC Statement,” March 18, 2026. federalreserve.gov

[7] Congressional Research Service, “The Federal Reserve’s Balance Sheet: A Primer and Projections,” updated March 2026; Board of Governors of the Federal Reserve System, FEDS Notes, “Quantitative Tightening: Lessons and Outlook,” December 2025.

[8] Federal Reserve Bank of New York, Markets Desk Operating Policy, “Statement Regarding Reserve Management Purchases of Treasury Securities,” December 2025. newyorkfed.org

[9] 与 [5] 同。

[10] Federal Reserve Bank of St. Louis, FRED Economic Data, “Assets: Total Assets (WALCL),” accessed April 2026. fred.stlouisfed.org

[11] Federal Reserve Bank of St. Louis, FRED, “Overnight Reverse Repurchase Agreements (RRPONTSYD)” and “U.S. Treasury General Account Balance (WTREGEN),” accessed April 2026.

[12] Investment Company Institute, “Money Market Fund Assets,” weekly statistical releases (week ended March 18, 2026 through week ended April 8, 2026, covering the peak-and-pullback period). https://www.ici.org/research/stats/mmf; ici.org

[100] Crane Data, “ICI: MMF Assets Rebound to $7.81 Tril.; OFR on Repo Market Participants,” April 5, 2026; “ICI: MMF Assets Hit Record $7.8 Tril.,” March 6 and March 20, 2026 coverage. cranedata.com

[101] Board of Governors of the Federal Reserve System, “FOMC Statement and Summary of Economic Projections,” March 18, 2026; CNBC, “Fed interest rate decision March 2026: Holds rates steady, sees 2.7% inflation,” March 18, 2026; TD Economics, “U.S. FOMC Meeting (March 2026),” March 18, 2026. federalreserve.gov

国际清算与市场基础设施

[27] BCBS-IOSCO, “Margin Requirements for Non-centrally Cleared Derivatives,” September 2013, revised March 2015. bis.org

[28] Financial Stability Board, “Liquidity Preparedness for Margin and Collateral Calls,” December 2024. fsb.org

[29] Manmohan Singh, “Velocity of Pledged Collateral: Analysis and Implications,” IMF Working Paper №11/256, November 2011.

[13] International Swaps and Derivatives Association, “ISDA Margin Survey Year-end 2024,” May 14, 2025. isda.org

[69] CPSS-IOSCO, “Principles for Financial Market Infrastructures,” Bank for International Settlements, April 2012. bis.org

[82] CPMI-IOSCO, “Application of the Principles for Financial Market Infrastructures to Stablecoin Arrangements,” Consultative Report, October 2021. bis.org

[81] Basel Committee on Banking Supervision, “Novel Risks, Mitigants, and Uncertainties with Permissionless Distributed Ledger Technologies,” Working Paper 44, 2024. bis.org

Academic and research papers

[19] M. Avellaneda & S. Stoikov, “High-Frequency Trading in a Limit Order Book,” Quantitative Finance, Vol. 8, №3, pp. 217–224, 2008. doi.org

[20] D. Easley, M. López de Prado, M. O’Hara, “The Microstructure of the ‘Flash Crash’: Flow Toxicity, Liquidity Crashes and the Probability of Informed Trading,” The Journal of Portfolio Management, Vol. 37, №2, pp. 118–128, Winter 2011.

[21] D. Easley, M. López de Prado, M. O’Hara, “Flow Toxicity and Liquidity in a High Frequency World,” Review of Financial Studies, Vol. 25, №5, pp. 1457–1493, 2012.

[22] T. G. Andersen & O. Bondarenko, “VPIN and the Flash Crash,” Journal of Financial Markets, Vol. 17, pp. 1–46, 2014.

[23] F. Wu, D. Sui, T. Thiery, M. Pai, “Measuring CEX-DEX Extracted Value and Searcher Profitability: The Darkest of the MEV Dark Forest,” arXiv:2507.13023 [cs.CR], July 2025; accepted by ACM Advances in Financial Technologies (AFT) 2025. arxiv.org

[24] J. Milionis, C. C. Moallemi, T. Roughgarden, A. L. Zhang, “Automated Market Making and Loss-Versus-Rebalancing,” arXiv:2208.06046 [q-fin.MF], August 2022, revised May 2024. arxiv.org

[25] European Securities and Markets Authority, “Maximal Extractable Value: Implications for Crypto Markets,” ESMA TRV Risk Analysis, ESMA50–481369926–29744, July 1, 2025.

[31] Centre for Economic Policy Research, “The Crypto Carry: Market Segmentation and Price Distortions in Digital Asset Markets,” VoxEU Column, 2025。

Cryptography and security research

[72] Verichains Research Team, “TSSHOCK: New Key Extraction Attacks on Threshold Signature Scheme (TSS),” Black Hat USA 2023, August 10, 2023. verichains.io

[73] Fireblocks Cryptography Research Team, “GG18 and GG20 Paillier Key Vulnerability,” CVE-2023–33241, August 2023.

[74] Trail of Bits, “Breaking the Shared Key in Threshold Signature Schemes,” CVE-2024–21492 through CVE-2024–21500, February 20, 2024. blog.trailofbits.com

[75] L. Wilke, F. Sieck, T. Eisenbarth, “TDXDown: Single-Stepping and Instruction Counting Attacks against Intel TDX,” ACM CCS 2024, CVE-2024–27457. dl.acm.org

[76] A. Seto, O. K. Duran, S. Amer, J. Chuang, S. van Schaik, D. Genkin, C. Garman, “WireTap: Breaking Server SGX via DRAM Bus Interposition,” ACM CCS 2025. wiretap.fail

[77] J. De Meulemeester, I. Verbauwhede, D. Oswald, J. Van Bulck, “Battering RAM: Low-Cost Interposer Attacks on Confidential Computing via Dynamic Memory Aliasing,” IEEE Symposium on Security and Privacy 2026. batteringram.eu

[78] R. Zhang, L. Gerlach, D. Weber, L. Hetterich, Y. Lü, A. Kogler, M. Schwarz, “CacheWarp: Software-Based Fault Injection Using Selective State Reset,” USENIX Security 2024, CVE-2023–20592.

[79] S. Gast, H. Weissteiner, R. L. Schröder, D. Gruss, “CounterSEVeillance: Performance-Counter Attacks on AMD SEV-SNP,” NDSS 2025.

[80] Confidential Computing Consortium, “Technical Analysis: Defense-in-Depth Recommendations,” 2023.

[88] G. G. Dagher, B. Bünz, J. Bonneau, J. Clark, D. Boneh, “Provisions: Privacy-Preserving Proofs of Solvency for Bitcoin Exchanges,” ACM CCS 2015. eprint.iacr.org

[89] T. Conley, N. Diaz, D. Espada, A. Kuruvilla, S. Mayne, X. Fu, “IZPR: Instant Zero Knowledge Proof of Reserve,” IACR ePrint 2023/1156, Financial Cryptography 2024 Workshops. eprint.iacr.org

[90] Y. Deng, J. Clark, “Xiezhi: Toward Succinct Proofs of Solvency,” IACR ePrint 2024/2001. eprint.iacr.org

[87] G. Maxwell, “Proving Your Bitcoin Reserves,” Bitcoin Forum Post, 2014; B. Kim, D. Lee, J. Lee, W. Lee, “Snapshot Cherry-Picking Attack in CEX Proof of Reserves and its Mitigation,” IEEE Access, Vol. 13, 2025.

[99] National Institute of Standards and Technology, “Post-Quantum Cryptography Standards: FIPS 203, FIPS 204, FIPS 205,” August 2024. csrc.nist.gov

法律与标准化框架

[83] UNCITRAL, “Model Law on Electronic Transferable Records (MLETR),” adopted July 13, 2017. uncitral.un.org

[84] Orrick, “New York Enacts 2022 UCC Amendments: A New Era for Digital Asset Transactions,” December 2025.

[85] UK Parliament, “Electronic Trade Documents Act 2023,” Royal Assent July 20, 2023. legislation.gov.uk

[86] European Securities and Markets Authority, “Report on the Functioning and Review of the DLT Pilot Regime — Art. 14,” June 25, 2025。

Market data and industry reports

[4] DefiLlama, Perpetual DEX Trading Volume Dashboard, 2025 Annual Data, https://defillama.com/perps; Cointelegraph, “Perpetuals DEX Volume 2025: Onchain Derivatives Growth,” January 2026.

[6] Newhedge, “Bitcoin ETF Tracker,” accessed April 8, 2026. https://newhedge.io/bitcoin-etf; Bloomberg, “U.S. Spot-Bitcoin ETFs Command Over $85 Billion,” April 8, 2026.

[17] SoSoValue, Spot Bitcoin ETF and Spot Ethereum ETF Net Inflow Tracker, April 6, 2026. sosovalue.com

[18] Fortune, “Current Price of Bitcoin for April 8, 2026,” April 8, 2026.

[14] RWA.xyz, Tokenized Treasury Dashboard, accessed April 2026. app.rwa.xyz

[26] DefiLlama, Layer 2 TVL Dashboard, accessed April 2026; The Block Research, “2026 Layer 2 Outlook,” January 2026.

[30] CME Group, “Portfolio Margining,” 2026. cmegroup.com

[32] Markets Media, “Bitnomial Is First CFTC-Regulated Exchange to Accept Digital Asset Margin,” September 2025. marketsmedia.com

[33] Pillsbury Winthrop Shaw Pittman, “CFTC Perpetual Futures: BTC, ETH Crypto Derivatives,” July 2025. pillsburylaw.com

[34] RWA.xyz, Tokenized Treasury Market Data, Q1 2026.

[35] 行业汇总:BlackRock BUIDL AUM,March 2026.

[36] CryptoSlate, “Hashnote USYC Overtakes BUIDL,” January 22, 2026.

[37] The Block, “Franklin Templeton FOBXX Exceeds $1 Billion,” April 2026.

[38] Ondo Finance, OUSG and USDY AUM Disclosures, 2025–2026.

[39] Industry aggregated data, tokenized treasury issuer concentration, 2025.

[42] CME Group, “CME Group Partners with BMO and Google Cloud for Tokenized Cash Capabilities,” March 24, 2026.

[43] Hyperliquid, “Portfolio Margin Documentation,” 2026. hyperliquid.gitbook.io

[44] Aster Protocol Documentation, 2025–2026.

[45] 21Shares, “The Perpetual DEX Wars: Hyperliquid, Aster, and Lighter in Focus,” 2025. 21shares.com

[46] Lighter, “Protocol Whitepaper,” 2025. assets.lighter.xyz

[70] CCData (UK FCA Authorised Benchmark Administrator), “Crypto Custody: An Institutional Primer,” commissioned by Zodia Custody, 2024.

[71] Taurus-State Street Institutional Custody and Tokenization Services Partnership Announcement, August 2024.

[91] DefiLlama Perp DEX dashboard, Q4 2025 monthly volume data; Coinfomania, “Perp DEX Volume Record $1.14 Trillion September 2025,” September 2025.

[92] CoinDesk, “Hyperliquid’s Perpetual Share Shifts as Aster and Lighter Gain Ground,” September 23, 2025.

[93] CME Group, “CME Group Crypto Derivatives 2025 Annual Review,” December 2025.

[94] CoinDesk, “CME Crypto Futures Volume Hits Record 795K Contracts Amid Volatility,” November 24, 2025.

[95] Coinbase, “Coinbase Futures: Spring 2025 Release — More Hours, More Contracts, and More Perpetual,” 2025.

[96] Cointelegraph, “Cboe Plans 10-Year Dated Bitcoin and Ethereum Futures,” 2025.

[97] ETF.com, “$34 Billion Entered Crypto ETFs in 2025,” December 2025.

[98] CoinDesk, “Circle (CRCL) overtakes BlackRock (BLK) as tokenized treasury market hits $11 billion,” March 13, 2026; Circle / Hashnote acquisition disclosures (2025); Binance institutional collateral integration via Banking Triparty and Ceffu, disclosed Q3 2025. coindesk.com

[102] Kraken, “Announcing the world’s first regulated, tokenized-equity perpetual futures, using xStocks,” Kraken Blog, February 24, 2026; CoinDesk, “Kraken brings crypto-style, 24/7 perpetuals trading for tokenized U.S. stocks,” February 24, 2026; Business Wire, “Kraken Lists the World’s First Regulated Tokenized Equity Perpetual Futures Using xStocks,” February 24, 2026. blog.kraken.com